What are associated companies?

Simply put, companies are considered as associated companies when one company controls the other, or when both companies are controlled by the same person or entity. In this case, control just means that the person or entity owns at least 50% of the shares, they control more than 50% of the voting power, or they are entitled to 50% or more of the distributable profits or assets.

An associated company does not necessarily have to be a group companies, where there is a parent-subsidiary structure; however, group companies are typically considered as associated to each other. Let’s take a look at some examples of associated companies below:

- A director owns 100% of Company A and 100% of Company B --> this means they are associated companies.

- A director owns 80% of Company X, which you are filing for, and they also control 60% of Company Y with another director who also controls Company Z --> this means that Company X and Company Y are associated companies. Company Y and Company Z are associated, however, as Company Z and Company X do not share the same director, these are not associated.

- Company M is a subsidiary of Company N --> this means that these two companies are associated.

You need to keep note of how many of your company’s are associated as this will have to be reflected in your company’s tax return. You may be wondering why, so let’s get into it!

Why do associated companies matter when completing your tax return?

Corporation Tax Rules:

For accounting periods that fall from the 1st April 2023 and onwards, there were new rules introduced which involved associated companies and their effect on the corporation tax rates, which were also changed. These updated regulations replaced the previous rule regarding 51% group companies, which was used partly to determine whether a company was considered as large or not.

To begin, we need to understand what the new tax rates were changed to. Before the 1st April 2023, there was just one corporation tax rate, which was set for all companies, at 19%. However, after the 1st April 2023, the tax rate was split into two rates - one for small companies, known as the Small Profits Rate, which was set at 19%, and another for larger companies, known as the Main Rate, which was set at 25%, alongside a new relief called marginal rate relief. The small profits rate is applicable for companies that have a taxable turnover of £50,000 or less. Whereas the Main Rate applies to companies whose profits are £250,000 or more. For those companies that have taxable profits between £50,000 and £250,000 (known as the lower and upper limit), they are charged corporation tax at the main rate of 25%, however, marginal rate relief is then applied on this tax, to reduce it.

Marginal rate relief is essentially a credit that is applied against the corporation tax due, and is based on your companies overall taxable profits, whether the company received any dividends or ABGH income, and how many associated companies there were in the period. The more associated companies that a company has, the lower their upper and lower limited for marginal rate relief are. For example, a company with no associated companies will be eligible for marginal rate relief if their taxable profits are between £50,000 and £250,000, however, a company with 1 associated company will be eligible for marginal rate relief if their taxable profits are between £25,000 and £125,000 instead. The more associated companies a company has, the less marginal rate relief they can claim. You can find out more about this by reading our article ‘Corporation tax increase and marginal rate relief explained’. It is also worth noting that not only will your marginal rate relief be reduced, but you may also not be able to claim the small profits rate either, if your taxable profits do not fall below the new lower limit.

Capital Allowances:

While the number of associated companies does not directly impact your corporation tax return, it does impact how much you can claim in terms of capital allowances. For corporation tax, there is something called an ‘Annual Investment Allowance’, which is a type of capital allowance that you can claim on plant and machinery. The AIA amount that you can claim for in each accounting period is up to £1 million, however, this allowance is spread across all of your associated group companies, meaning that if you are the subsidiary of a parent company, the £1 million claim is between both companies, not each company. For example, if Company A (parent company) has claimed £950,000 of AIA in the period, then Company B (a subsidiary), can only claim up to £50,000 in AIA. However, there are also other types of capital allowance claims you can make instead, which we discuss in our article ‘How to claim capital allowances on a CT600 return’.

Where do I reflect the number of associated companies in my CT600 return?

Now that I have a better understanding of what associated companies are and how they affect your corporation tax, let’s take a look at how you need to reflect them within the CT600 return itself.

To start, you will need to add the CT600 return filing template to your account and open it up. Then, please head to the ‘CT600 Sections’ tab and switch box 130, called ‘Indicators and Information’ to ‘Yes’. This will create a new tab below the CT600 Sections header - please click on this to open the necessary page.

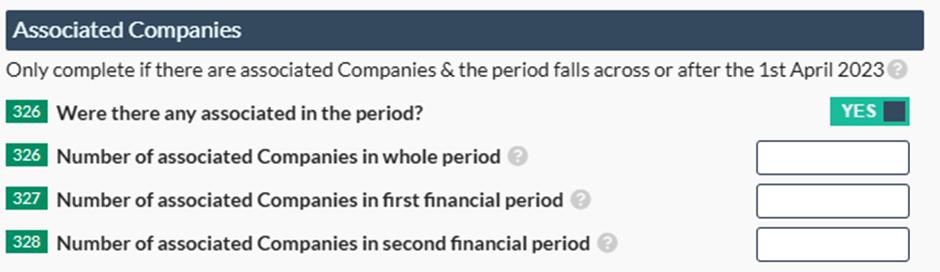

Near the bottom of the template, you should be able to see box 326 - please switch this to ‘Yes’. You will now find 3 boxes below - 326, 327 and 328.

Please complete box 326 if the company’s accounting period falls within one financial year (for corporation tax). Alternatively, if your company’s accounting period falls across two financial years, then you must complete boxes 327 and 328. Please note that you must complete either box 326 or 327/328 - you cannot complete them both. Once completed, your marginal rate relief/corporation tax will update automatically, accordingly.

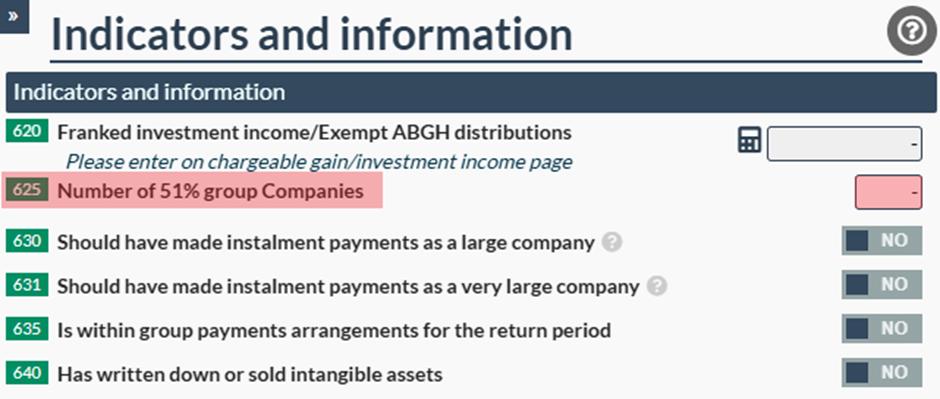

If you are filing for an accounting period that falls before the 1st April 2023, then this section will not be applicable. In this case, if there are any associated companies, you will need to complete box 625 instead, which is for the number of 51% group companies that your company had during the period.

You can find this section within the same ‘Indicators and Information’ page near the top.

If you are still struggling to find the associated companies section, we do also have an amber warning that appears at the bottom of the filing template to prompt you - please click on this and it will take you to the correct page. If it is not relevant, then you can ignore this warning.

Hopefully after reading this article, you will have a better understanding of what an associated company is, how having them will affect your company’s corporation tax rates, and also where to find this section on the CT600 return!