When you have an accounting year of more than 12 months, which often happens in your first year of trading, this can lead to a dilemma as CT600 forms can only report a maximum of 12 months.

When a company is incorporated, its incorporation date will be on the day the company applied to the Companies House Register. If you want to extend your first year, you can do so for up to 18 months. However, even if you don’t choose to extend your first year unless your incorporation date was on the first day of the month, Companies House will set the end date to 12 months plus the extra days to the end of the anniversary month. This means you will have an extended year, so your first-year accounts will be slightly longer than 12 months.

For example if you incorporated on the 11th July 2022 , Companies House will move your end date to

the 31st July 2023. This will then become your Accounting Reference Date (ARD).

This raises a reporting anomaly. HMRC require a Corporation Tax return (CT600) after

the end of the accounting period. But as a CT600 can only report up to a maximum of 12 months, so you will need to file online two CT600's.

Companies House however only require a single set of abbreviated Accounts that cover the whole (extended) period / extended year.

In the above example year you will would need to create a (HMRC) IXBRL Company Accounts filing for 7th July 2022 to

the 31st July 2023 and a CT600 for the 7th July 2022 to the 6th July 2023 and a second CT600

for the 7th July 2023 to the 31st July 2023.

You will need to attach the accounts that cover the extended period with either or both CT600 Filings.

Confused? The Steps below hopefully guide you through this situation.

Note: HMRC require full Accounts which includes a Profit and Loss Statement

where Companies House only require the statutory declaration and the Balance Sheet.

Confused? Our CT600 Filing Guide Will Help you Through this Situation.

Step 1 - Create two Corporation Tax CT600 Filings and a single IXBRL Company Accounts

You can either create the first CT600 and accounts using the QuickStart dialog which after selecting your company, Accounting period start date and company size (Micro or Small) - or alternatively create 2 CT600 filings and IXBRL accounts separately.

In both cases you should end up with 3 Filings in your blotter which will hopefully look like the below:

In this example the accounting year has been extended to cover the period 7th July 2022 to 31st July 2023 - a period of 1 year and 25 days.

Note that the first CT600 accounting period starts on the 7th July 2022 and ends on the 6th July 2023 (12 months). The second CT600 starts on the 7th July 2023 and ends on the 31st July 2023 (25 days).

The IXBRL accounts can cover the entire extended accounting period (in our example 7th July 2022 to the 31st July 2023.) - which makes the filing slightly easier.

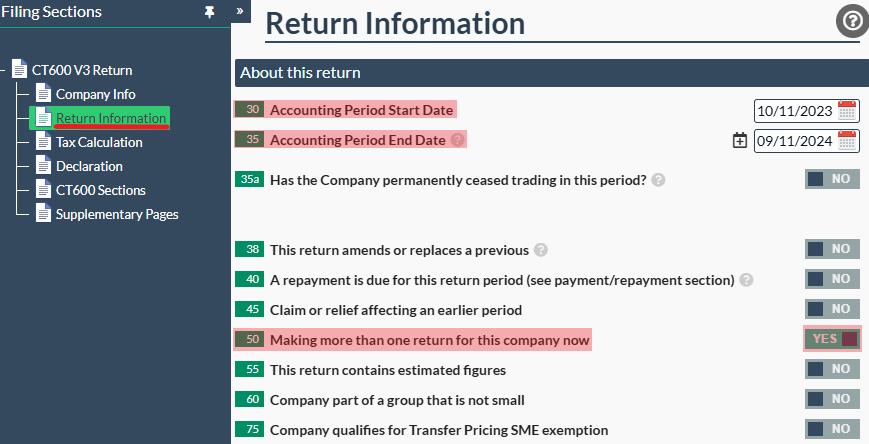

You can check the accounting period are correct, and change the dates if required, in the Return Information section of the CT600 return itself. Please click on the CT600 return template to open it, then click on the 'Return Information' tab. Here you can see the dates in boxes 30 and 35.

Also, please ensure that you switch box 50 to 'Yes' (which can be found on the Return Information page as well) in both of the CT600 returns when filing for your first accounting period.

Step 2 - The first CT600 return (the first 12 months)

The primary question here is normally "what to enter for turnover in CT600 when

accounting year is more than 12 months"?

Generally your records / accounting system should

be able to provide what income and expenditure you had for each period, if your records do not divide your income and expenditure over the extended period, you should apportion according to the number of days in each part of the extended period.

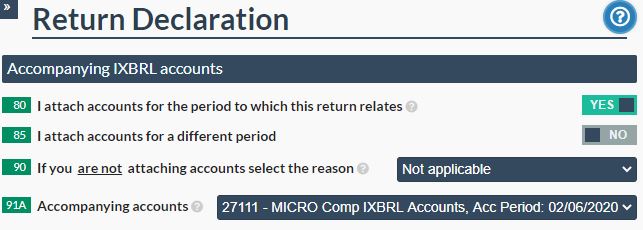

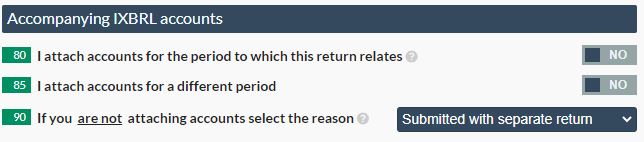

When you are completing the CT600, in the declaration section you will need to allocate the IXBRL accounts that you have created. Note that Box 80 is set to YES; Box 85 is set to NO, and; Box 90 is set to Not applicable. With box 91A being set to the IXBRL Company Accounts. Note: if you have supplied your own IXBRL accounts you can select to upload them in the drop-down menu in box 91A.

Step 3 - Your second CT600 return / the extended period

You can attach your accounts to both CT600 returns as it makes no difference, but they must be attached to one of them. Note: Although in this example, we had the longer period first (the 12-month period), it actually makes no difference, and therefore you could have the shorter period for the first CT600.

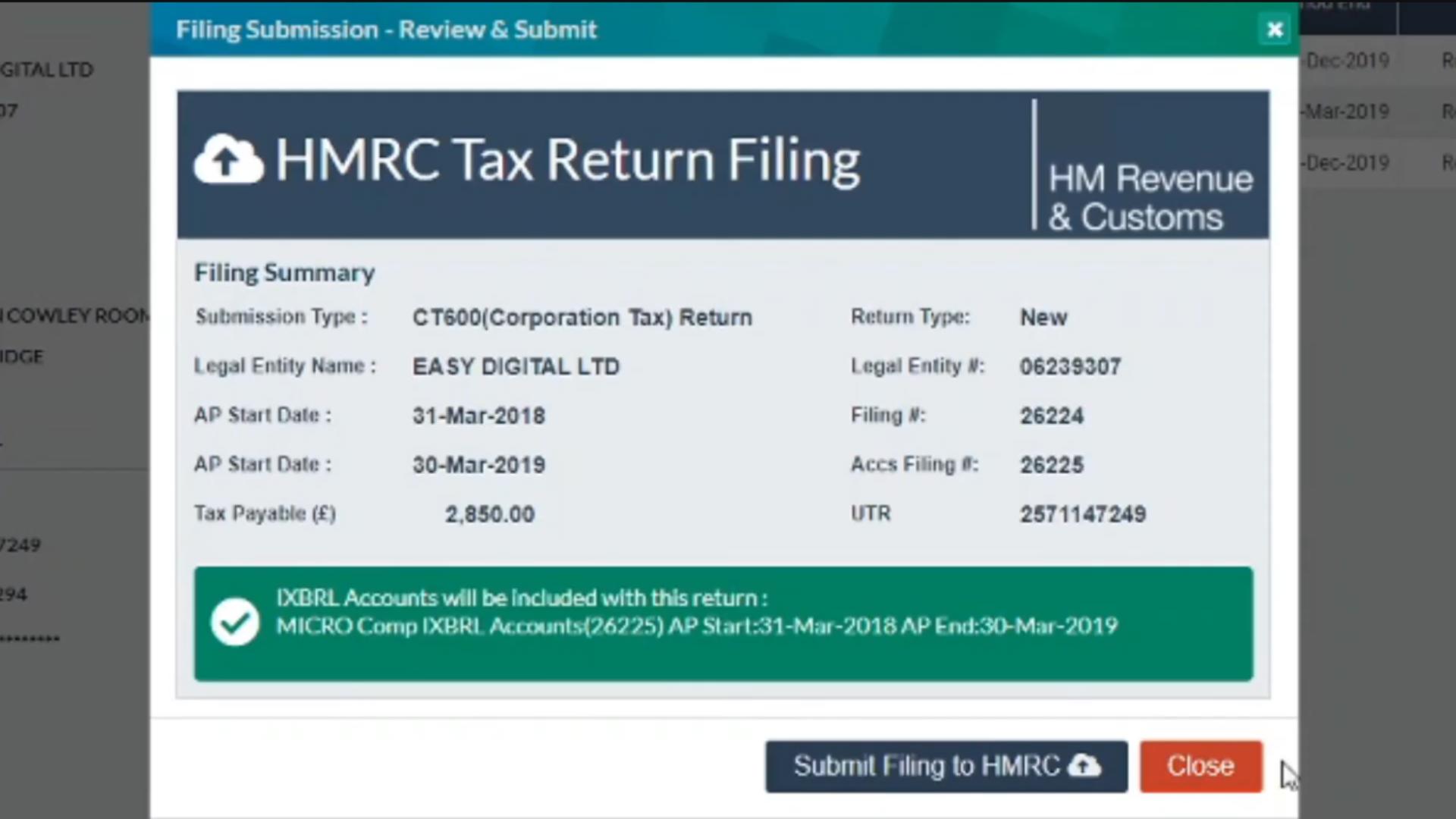

Step 4 - Make your submission to HMRC

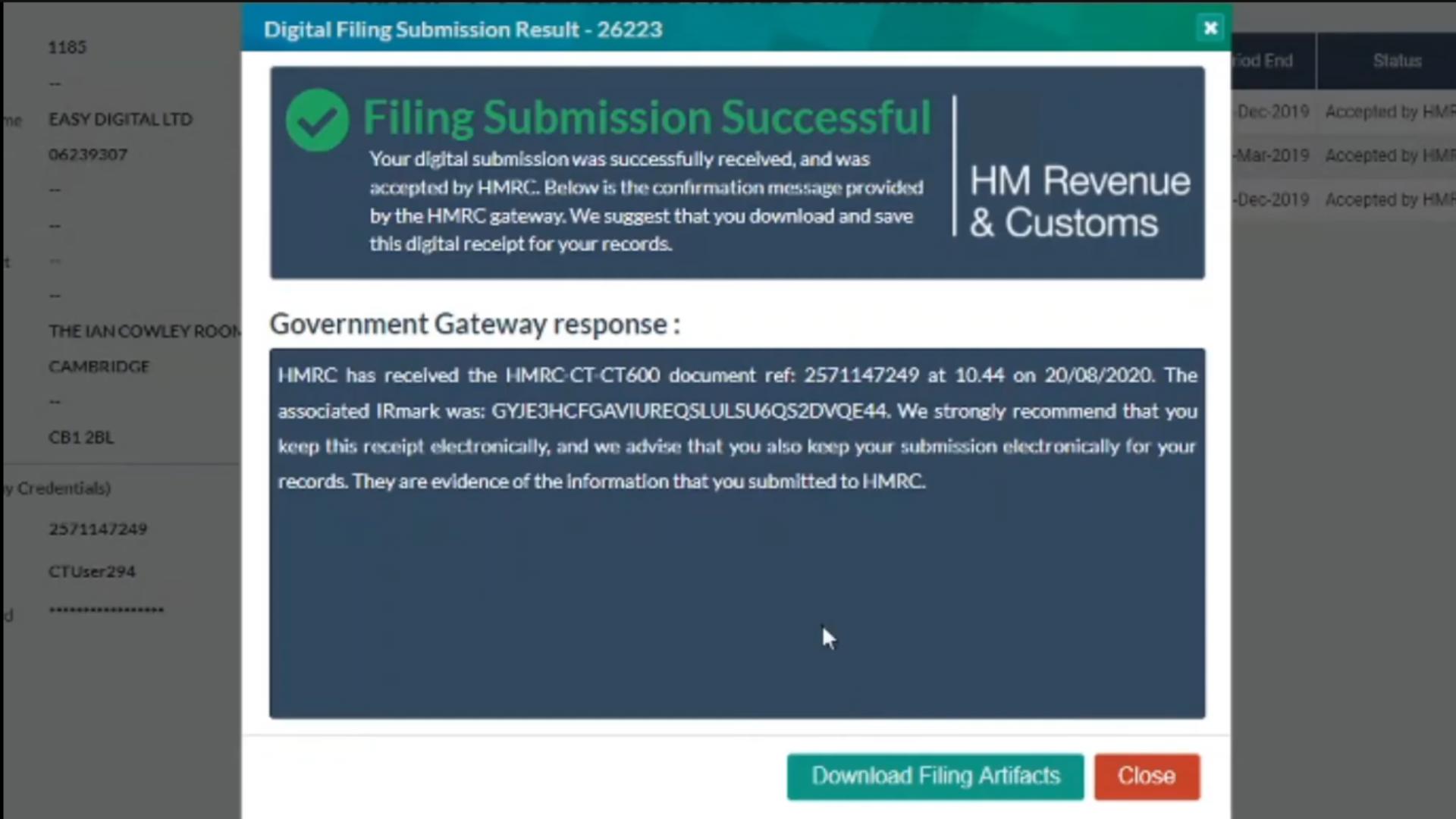

Once you have completed your returns and completed the above, you will now be able to submit and file online. You can submit your filings in any order, normally though the CT600 return with the accounts attached if sent first. If you get a rejection error, it’s better to deal with this first. Once you have submitted both (and accepted), you will receive emails from the Easy Digital Filing team with your IRMark (digital hash) and later (possibly 4-12 hours) an email from HMRC, if they have your email address.

Step 5 - Make your submission to Companies House

When I first wrote this article, we did not submit to Companies House, but due to popular demand we built out to the Companies House interface and you can now also create a Companies House Submission which will fillet (remove the Profit and Loss statement) from your HMRC IXBRL accounts, and add the iXBRL tagging for Companies House.

You can then file with a click direct and file online to Companies House. For Micro Limited Companies you can do this through the Companies House web site for free, however, as you will have already made the accounts up on the platform for HMRC, we hope that being able to do this automatically will save you time, ensure accuracy and consistency with what is filed with HMRC, and have all your Accounts filings in one place. If you have already paid, please ask us for an upgrade code for this additional filing.

Step 6 - Sit back and relax

All done - at this stage you will feel like a master. The pressure is off, well for another year anyway!