There can be a lot of confusion surrounding how to report bank loans on both the CT600 (corporation tax return) and on the accounts that accompany it, however, when you break it down into smaller sections, it can be easy to understand.

The first mistake that people tend to make is that they believe that all money going into the company, no matter where it comes from, should be considered as income on their income statement. However, this is not the case when it comes to loans and bank loans. A loan is not considered as income because the company is expected to pay that money back to the creditor overtime, meaning it is only reflected on the company’s balance sheet. However, any interest that is accrued or paid on the loan during the period, goes in the income statement as an expense. This can vary depending on the type of loan that it is.

How to record a bank loan with interest

If you have taken out a bounce back loan of £30,000 from the government, and you have arranged to pay it back at an interest rate of 2.5% over a period of 5 years, then this is how your accounts might look at the end of the first period in which you received the loan:

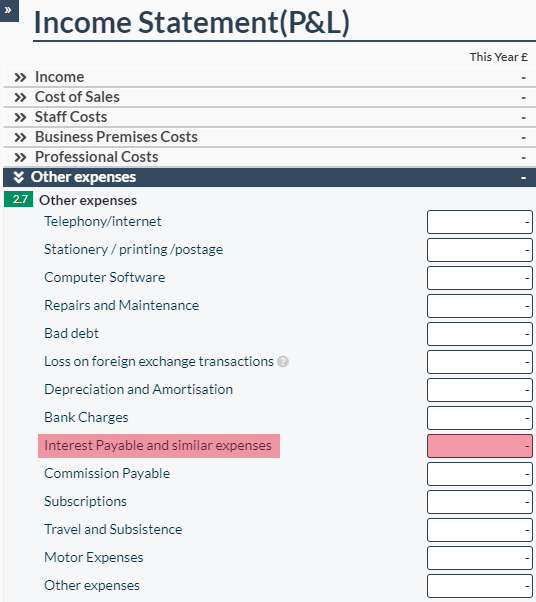

On your income statement:

Other expenses: Interest payable and similar expenses = 0

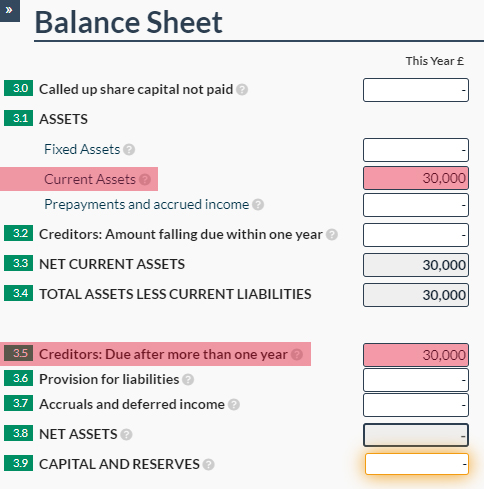

On your balance sheet:

Creditors: Due after more than one year = £30,000

This amount of £30,000 is reflected in the balance sheet as a current asset, because it shows the ending bank balance of the company. If the company had £0 in their bank account before the loan was added, and then they received the £30,000 of loan, their ending bank balance would be £30,000 at the end of the period.

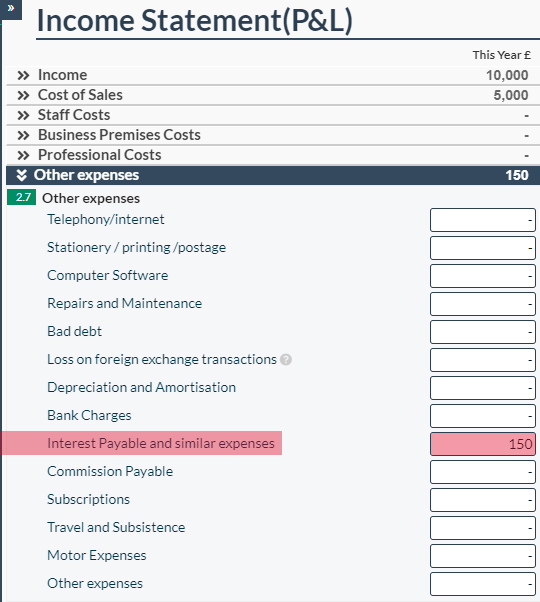

We then assume that the company has had £10,000 of sales income and £5,000 of expenses during the next accounting period. As the loan is expected to be paid back over a 5-year period, you are required to pay £500 of the loan off each month, and as you are charged at a rate of 2.5%, £12.5 of interest is added to your loan, per month, as well. Here is a breakdown:

On your income statement:

Sales = £10,000

Cost of sales = £5,000

Other expenses: Interest payable and similar expenses = £150

(As your accounting period is 12 months, you would have paid £12.5 x 12 months, which equals £150 of interest total).

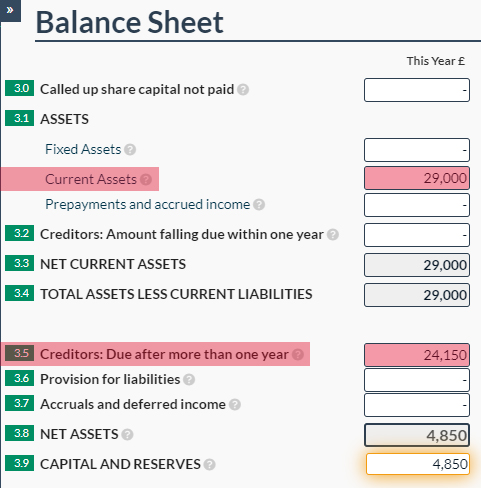

On your balance sheet:

Current assets = £29,000

This would be the ending bank balance for the company: £30,000 (at start of period) + £10,000 (sales) - £5,000 (expenses) - £6,000 (loan repayment) = £29,000

Creditors: Due after more than one year = £24,150 (This is the loan minus the amount actually paid off, after interest has been taken into account)

If you have a plan to pay off your loan in 5 years, that means that your monthly repayments are of £500, however, you then have to add back the interest charged each month to the amount of loan outstanding. So, if you have paid off £6,000 (£500 x 12 months), however, there was £150 interest charged (£12.50 x 12 months), then to figure out the remaining loan we calculate: £30,000 (initial loan) - £6,000 (loan repayment) + £150 (interest added) = £24,150 remaining left to pay.

But what if I have a loan with no interest?

Your company can also take out loans that don’t have interest, for example, a director’s loan (which is when the director loans the company a sum of money). Typically, directors don’t charge interest on the loans that they give to their company, however, if you decide that you want to, you can.

With a standard director’s loan, the only place it needs to be recorded is on the balance sheet. For example, if the director loans their company £30,000, then it would be reflected in both the current assets of the company and the creditors due. Here is an example:

If the company has had £2,000 of sales and £8,000 of expenses during the period, and the director has loaned the company £30,000, here is what your accounts will look like:

On your income statement:

Sales = £2,000

Cost of sales = £8,000

Loss = £6,000

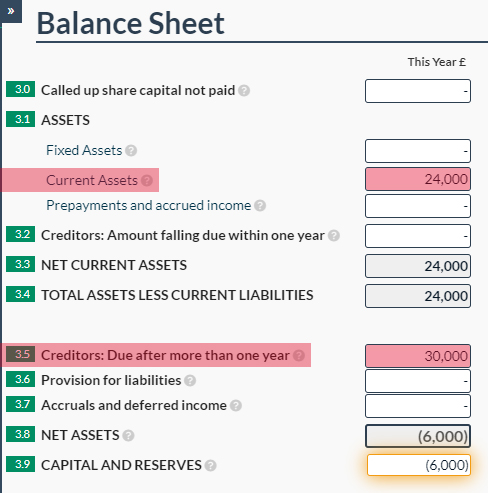

On your balance sheet:

Current assets = £24,000

This is the ending bank balance of the company on the last day of the accounting period: £0 + £30,000 (loan) + £2,000 sales - £8,000 (expenses) = £24,000

Creditors: Due after more than one year = £30,000

This just consists of the full director’s loan.

Typically, a director’s loan is not paid back on a yearly basis as the company is only expected to start paying the director back when it is in a financial position to be able to. However, if in the next accounting period, the company has a boost in sales and their net profit is great enough to be able to pay some of the director’s loan back to the director, then here is an example of what the company’s accounts may look like:

In this example, we are expecting that the company has had £20,000 of sales, £8,000 of expenses, and have decided to pay off £5,000 on the director’s loan.

On your income statement:

Sales = £20,000

Cost of sales = £8,000

Profit = £12,000

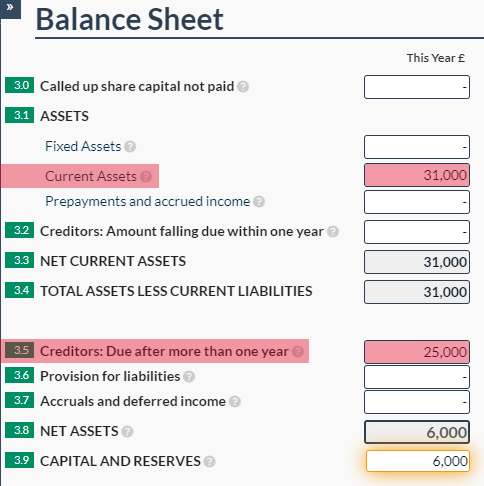

On your balance sheet:

Current assets = £31,000

This is the ending bank balance of the company: £24,000 (at start of period) + £20,000 (sales) - £8,000 (expenses) - £5,000 (director’s loan repayment) = £31,000

Creditors: Due after more than one year = £25,000

This is the remainder of the director’s loan after repaying £5,000 back to the director.

As you can see, as there was no interest charged on the loan, the only place where the repayments were reflected was in the balance sheet.

So, what are the most important things to remember then?

The key things to remember when reporting loans or bank loans for your company:

- When there is interest on the loan, it needs to be included in the income statement as a separate figure (under interest payable and similar in other expenses)

- When the loan is partially repaid, the amount of creditors due is reduced and the figure left is the remainder of the loan to pay off.

- It is important to remember that if you paid £6,000 of the loan off, it doesn’t necessarily mean that your creditors will be reduced by £6,000. This depends on if you are being charged interest on the loan, in which case the remainder of loan is: amount of loan at start of period – amount of loan repaid in period + amount of interest charged on loan in period.

- Loans do not count as income and are not reflected on the income statement, only on the balance sheet! Interest is the only amount that should be shown on the income statement!

What if my company has loaned someone money?

Now that you know the basics on how to report loans your company has taken out, it will be much easier for you to understand how to report a loan that your company has given out as well.

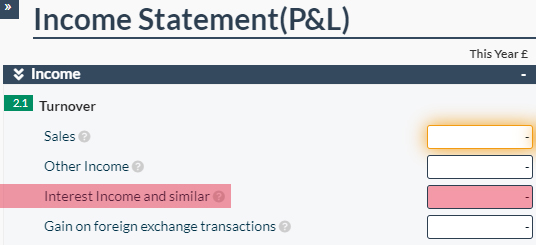

If your company has given a loan, to the director of the company, for example, you will need to record this as a current asset on your balance sheet as the director will be expected to pay back the money, at some point, to your company. Additionally, if your company is charging interest on the loan, this will also be reported in your income statement, however, this time it is recorded as income, not as an expense. The total interest charged for the accounting period will be reported as Interest Income and Similar under the income portion of your income statement.

If the loan is partially repaid to you, then your current assets will be reduced to the amount of loan left to pay back to the company, just like when we reduced creditors due when the company repaid the loan.

The only difference between receiving a loan and giving a loan, is that when giving a loan to a director or participant of the company, you also have to take note of this on your CT600 return for the accounting period in which you gave it - as you will be required to pay tax on the loan (however, you can claim this back at a later date once repaid). If you have more questions about this type of loan, please read the article 'How to Record a Directors Loan Account in your CT600', which will explain it greater detail.