Introduction to Capital and Reserves

Capital and Reserves, also referred to as the 'Owner's Equity', or for a public company that trades its shares on stock markets - 'Shareholder's equity' shows the net worth (book value) of a business. It is the share of a company's Net Assets that the owner can claim as their own, meaning that it shows the amount outstanding from a company's Assets after all Liabilities are met. The Capital and Reserves section can be found at the bottom of a company's balance sheet, below its assets and liabilities.

Every business has four main ways of getting funding to support its operations:

- the business' own earnings

- investment by the owners

- raising capital from external investors

- external debt

The capital introduced by owners plus the business' own earnings are the items that make the Capital and Reserves.

Net Assets vs Capital and Reserves

On a Company's balance sheet , net assets should equal Capital and Reserves, so that a company's Balance sheet is balanced, but what are the Net Assets ?

Net Assets is the difference between a company's total Assets and total Liabilities.

Assets include:

- Tangible and intangible Fixed assets, for example - equipment, property and goodwill

- Current assets such as cash at bank and hand, stock and accrued income

Liabilities include:

- Funds that the business owes, for example - bank loans, unpaid invoices and taxes

The Capital and Reserves can either be positive (a positive equity), meaning that the company's Assets are greater than its Liabilities, hence the business is in a position to meet both its Current and Non-current Liabilities; or a negative equity, showing that a company's Liabilities exceed its Assets, therefore, there is no enough capital to support its business operations.

How are Capital and Reserves Calculated?

The calculation for Capital and Reserves is not as hard as it sounds, and here is the calculation as follows!

Capital and Reserves = (Net profit for the period + Retained earnings + Share capital) - Dividends paid out

This represents the funds invested by owners plus profits or losses of the business since incorporation minus funds taken out of the business minus funds owed to others.

Retained earnings are the brought forward figure from the previous year's capital and reserves minus share capital.

Let's take a look at the balance sheet of two companies in the following examples - a company with positive Capital and Reserves, and a company with negative Capital and Reserves.

- Positive Capital and Reserves in a micro company

Company A has the following details:

- Net profit of £24,494

- Current assets of £94,561

- Liabilities of £18,633 are comprised of the corporation tax due for the period of £5,746 + a director's loan of £12,887

- Retained earnings of £51,334

- Paid share capital of £100

Net Assets calculation: total Assets of £94,561 minus total Liabilities of £18,633 = £75,928

Capital and Reserves calculation: Retained earnings of £51,334 plus Net profit for the period of £24,494 plus paid share capital of £100 = £75,928

The Net Assets equal Capital and Reserves

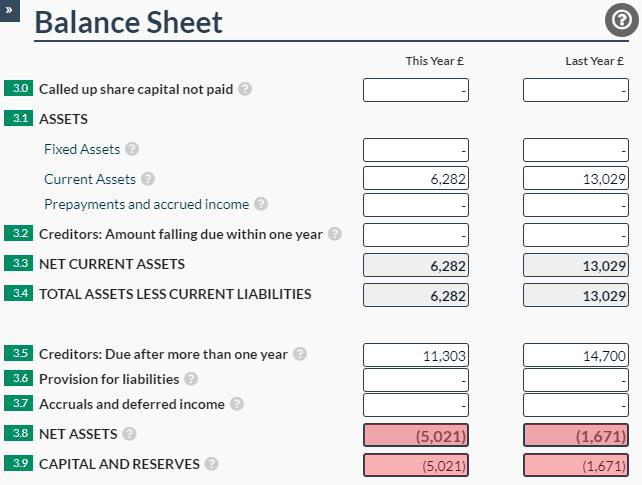

2. Negative Capital and Reserves in a micro company

Company B has the following details:

- Net loss of the period of -£3,350

- Current assets of £15,887

- Liabilities of £11,303 are comprised of a director's loan of £3,500 and a bank loan of £7,803

- Retained earnings of -£1,771

- Paid share capital of £100

Net assets calculation: total Assets of £6,282 minus total Liabilities of £11,303 = -£5,021

Capital and Reserves calculation of -£1,771 plus net loss of the period of -£3,350 plus paid share capital of £100 = -£5,021

The Net Assets equal Capital and Reserves

How can Capital and Reserves change?

There are several situations that can cause changes to a business' Capital and Reserves' figure, for instance:

- Profit or a loss in the accounting period

- Distribution of dividends

- Owners contributing personal funds to the business

To illustrate, if a business distributes dividends in its accounting period, this will affect the Capital and reserves by reducing the figure.

The Capital and Reserves ties together a business' Income statement and Balance sheet, by showing how the earnings for the period (from the Income statement) affect the value of the owner's equity (in the Balance sheet). The Capital and Reserves is a cumulative total of how the company has performed in all it's previous years. To find more about how to complete your balance sheet see our article.