Common Myths:

1. I can’t register for VAT because my turnover isn’t high enough.

You can register for VAT at any time, even if your company’s turnover hasn’t met the threshold! In basic terms, a company is required to register for VAT when its annual taxable turnover reaches or goes beyond the thresholds set by HMRC.

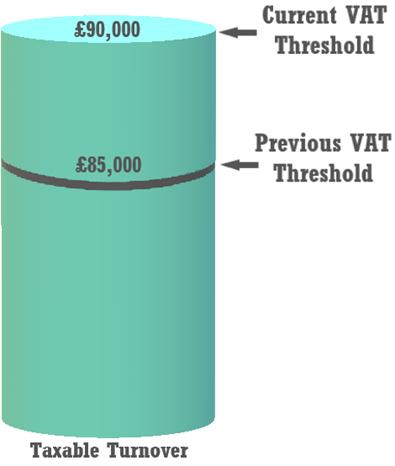

Previously, the VAT threshold for registration on the standard rate scheme was £85,000, however, from 1st April 2024, the threshold was increased to £90,000. It is important to note that this is the company’s annual taxable turnover, rather than just the annual turnover.

If your taxable turnover is below this threshold, then you can still register for VAT, which is known as ‘voluntary registration’. There are also many other VAT schemes which are available for smaller companies to register for. One popular VAT accounting scheme is the Flat Rate Scheme. Through this scheme, the VAT is only charged and paid on the income, or turnover, that the company makes. The rates are also different depending on what type of company you are registering. It is worth double checking before you register to see which scheme makes the most sense for your business.

But you might be wondering why someone would register for VAT when they don’t have to? Well, there can be many benefits to registering, depending on the type of company you are registering, its annual turnover, etc. One major benefit is that you might be able to claim a VAT credit from HMRC if the amount of VAT that you paid on your expenses was greater than the amount earned on your sales. For more on registering for VAT, please feel free to check out the article ‘How do changes to VAT threshold affect my small business?’ on our Knowledge Base.

2. I don’t have to file a corporation tax return because I made a loss.

Unfortunately, even if you made a loss, you will still need to file your company’s corporation tax return! All company’s that are active and trading are required to submit a corporation tax return with full accounts (income statement and balance sheet) to HMRC for each accounting period. HMRC will also send you a notice to file a corporation tax return letter before the filings are due, to confirm the period that they require the submission for, along with the date that it is due.

The only time that you may not need to file a tax return is if your company was dormant during the accounting period, meaning that your company was not trading and that there was no income or expenses incurred within the period. However, if HMRC have also sent your company a notice to file a corporation tax return, then you will still need to submit a nil corporation tax filing for the period. If you are unsure whether you need to submit a return, you can always double check with HMRC.

3. I should be eligible for the 19% tax rate because my turnover was under £50,000, but I am being charged at the 25% rate.

Many people believe that the small profits rate of 19% applies to all companies whose taxable turnover reported in their corporation tax filing is less than £50,000, however, this is not always the case. There are some restrictions on whether or not this can be applied, which can often confuse people. One of the most common misconceptions is that non UK companies that are filing corporation tax returns to HMRC are taxed based on their annual taxable turnover, however, the small profits rate and the marginal rate relief scheme are not available for non UK companies. Unfortunately, this means that no matter what your company’s profits were for the period, they will be charged tax on them at the 25% main rate for corporation tax.

Another misconception is that it doesn’t matter what period you are completing your corporation tax filing for as long as the taxable turnover is under the threshold, however, this is also not the case! The thresholds are based on a 12-month period, so if you are filing for a shortened accounting period, the thresholds are apportioned based on the number of days the period falls within 12 months. For example, if you are filing for a six-month period and your company’s taxable turnover was around £40,000, then you will be charged at the 25% main rate, with marginal rate relief applied, as the threshold for the small rate would have been reduced to £25,000 instead.

4. You can attach your additional information form to the CT600 return when submitting an R&D claim.

This is a common misconception about making R&D claims within your corporation tax filing, which causes a lot of people’s filings to be rejected by HMRC. But how do you fix it? Well, the additional information form is a separate form to the CT600 Return and CT600L, which must be submitted directly through HMRC’s website. You can attach it to your CT600 return as well, if you would like, however, this does not affect the submission.

Within this form, you will need to include the qualifying research and development expenditure that the company made within the period, and the details of each R&D project. HMRC introduced this for all R&D claim submissions which are made from 8th August 2023, and it must be submitted directly to HMRC before you submit the CT600 return. It is worth noting that even if the accounting period that you are filing for ended before 8th August 2023, you must still submit this as the date relates to when the submission was made rather than the accounting period.

Once the form is submitted, you will also need to ensure that you switch box 657 to ‘Yes’ in your CT600 corporation tax return. Also, if you have not done so already, you may need to submit a claim notification form directly to HMRC as well, before submitting the corporation tax return, if you are filing an R&D claim for the first time, or the first time in three years. For more information on how to file an R&D claim, you can head over to our article ‘How to File a R&D Tax Credit Claim’ on our Knowledge Base.

5. I need to reflect all directors loans in the CT600 return as well as in the accounts

There are two types of ‘directors loans’ – one is from the director to the company and the other is from the company to the director. Most loans that are made within small and micro companies are loans from the director to the company. These types of loans do not need to be reflected in the CT600 return, and are only considered as a creditor due for the company in the balance sheet of the accounts.

The other type of loan is from the company to the director – this may need to be reflected in the CT600 corporation tax return, depending on when it was paid or repaid, and the amount of the loan. You will need to reflect this in the CT600A supplementary form, however, this is only if the amount loaned is over £15,000 (for periods from 1st April 2022 onwards), but if it is under this amount, then it typically does not need to be reflected. You can find out more about directors loans and when to account for them in our article ‘How to Record a Directors Loan Account in your CT600’ from our Knowledge Base.

I hope that after reading this myth buster, you have been able to gain a better understanding of the CT600 corporation tax filing requirements and how to file correctly! If you want to learn more, we have plenty of articles available on our Knowledge Base, or you can send us a message about filing corporation tax , and we'll be happy to assist you.