Research and development (R&D) tax credits are a government incentive designed to reward UK companies for investing in innovation. Also referred to as Enhanced Expenditure they are a valuable source to reduce CT liability or to receive cash from HMRC if a loss was made. The idea behind R&D is to incentivise companies to invest in accelerating their R&D efforts, hiring new staff and ultimately growth.

To qualify for R&D Tax credits a company must:

- Be a UK limited company that is subject to Corporation Tax.

- Have carried out qualifying research and development activities.

- Have spent money on these projects using either internal PAYE resources or a Third party.

What is classed as Research and Development

Not all projects are eligible as R&D is aimed at projects that are seeking to advance science or technology. The key requirements are:

- Be seeking an advance in the field of technology or science

- Be considered commercially innovative

- Incorporate science or technology that is not readily available in your industry

- Relate to your company’s trade – you must be intending to use the findings for your business

- Additionally, your company must not currently be receiving state aid or subsidised expenditure.

What types of R&D claims can you make?

There are different types of R&D claims you can make, depending on the size of your company and also the financial year that your accounting period falls across.

SME R&D Claims:

If your company is classed as either a micro, small, or medium sized entity then you can make an SME R&D claim. This type of claim offers a higher return rate as it is designed specifically for smaller businesses. For this type of claim, you can consider all qualifying R&D expenses that were incurred during the period, and you will either get a reduction in tax due or a tax credit pay-out depending on if your company is profit-making or loss-making once the claim has been calculated. It is important to note that this scheme is only available for companies whose accounting periods started before 1st April 2024.

RDEC Scheme:

The RDEC scheme is another R&D tax credit scheme which is available to be claimed by the following types of entities:

- Large companies

- Small and medium sized entities that are claiming for work that has been subcontracted to them

- Small and medium sized entities that have received a notified State Aid for the project

- Small and medium sized enterprises that are claiming for costs that have been subsidised in some way (such as a grant)

It is important to check the requirements before making any claims.

With the RDEC scheme, you can only claim for 'above the line' costs, meaning you can claim on costs that are incurred by the business in order to make or sell its products/services, and that impact the company's profits (before tax). The current RDEC rate is 20%, which applies to all expenditure incurred from the 1st April 2023 onwards.

Merged RDEC Scheme:

For accounting periods starting on or after the 1st April 2024, a new merged RDEC scheme will be replacing both the SME R&D Scheme and the old RDEC scheme. With this, they are merging the two schemes so that all qualifying companies can claim under this tax relief scheme instead. It is very similar to the current RDEC scheme in that again only 'above the line' costs are considered when making the claim, and the rate will stay at 20%.

However, there are some differences between the current RDEC scheme and this new merged scheme. To start, within the calculation, it uses the 19% small profits tax rate rather than the 25% main corporation tax rate within this new scheme (for loss-making companies only). It also takes into account the PAYE/NIC contributions at the same rate that is does in the SME R&D scheme when determining the tax credit claim - which is (PAYE/NIC contributions x 3) + £20,000. The introduction of this new scheme should allow for a more cohesive approach for all companies looking to make R&D claims.

ERIS Scheme:

Alongside the new merged RDEC scheme, they are also releasing the ERIS (or Enhanced R&D Intensive Support) scheme. This is also introduced for companies whose accounting period starts on or after 1st April 2024. It is very similar to the already in place R&D Intensive company scheme which is available for SME's making R&D claims. It has the same enhanced expenditure rate of 86% on top of your qualifying expenses, and it offers a tax credit claim rate of 14.5%.

It is important to note that only companies whose relevant R&D expenditure is at least 30% of its total expenditure (including that of any connected companies) can make this type of R&D claim.

At the moment, we only support the making of SME R&D claims (both intensive and non intensive) through our software, however, we will be updating this to include the integrated RDEC scheme as well, in the near future.

What can be claimed and how much Tax credit can you claim?

Currently any cost that is eligible for SME R&D Tax credit must be related to a 'R&D phase' of the projects life cycle - this could be PAYE costs of resources working on the R&D, equipment directly related to the research and any related third party costs.

The current rate of enhanced expenditure available is 86% of the R&D expenditure (this was reduced from 130% pre April 2023). Since you will also include the original cost in the total operating expenses, the overall impact will be a 186 % increase in costs (or 230% pre April 2023) - hence causing a reduction in the corporation tax liability.

In companies which are yet to be cash generative (potentially in start-up phase), or loss making, you may be entitled to a R&D tax credit payment from HMRC, instead. The exact amount of R&D relief that you can receive and the actual amount you can claim back as a Tax Credit is related to many factors, but don't worry - you can use our Research and Development Calculator to gain an understanding of what your company's R&D relief might look like.

For accounting periods starting after 1st April 2021, HMRC have introduced a cap on the amount of R&D tax credit that can be claimed. This is following on from the introduction of the CT600L from the start of April 2021 for all R&D tax credit claims. The cap is now the lesser of the existing calculation - the surrendable loss X 10% (or 14.5% PRE April 2023) or 3 times the total PAYE/NIC contributions paid by the company to HMRC in the period + £20,000. This means that if you have not been registered for PAYE or only spent R&D on contractors, then your tax credit will be limited to a maximum of £20,000.

If you have an accounting period that straddles April 2023 (part of the year falls before this date and part afterward) then the R&D claim is calculated by pro-rataing the spend over the period. This is all calculated for you, within our software.

How do you claim?

Although the process may seem complex to the inexperienced; it's actually relatively straight forward, with many people in Micro & Small business sizes put off by not knowing what can be claimed and how to file the Digital Filing return to HMRC. The Easy Digital Filing CT600 template has sections specifically for R&D. The following steps guide you through the process from start to finish.

Step 1 - Identify R&D work/Projects that you are undertaking

The type of company you are, and what your activities relate to, will dictate whether you are able to take advantage of R&D claims or not. Although the majority of companies who can make R&D claims are companies within the tech or scientific sector, many other industries can also carry out R&D. For example companies which rely on Information Technology may perform research to build a system which will be a game changer and advance their capabilities.

Once you have identified a project or package of work that qualifies as R&D, you will need to take a look at the 'problem' or challenge your project focuses on, and perform the following tests:

- Will the work perform a technical advance - will the solution provide new technological functionality for you

- Are there technical uncertainties in the work - are you going into the work with 'unknowns'

- Will you be able to describe how the uncertainties are overcome

- Can you explain why the uncertainties could not just be resolved by a competent professional

We would recommend that you use the headings above in your R&D report - this is the supporting document which you attach as part of your R&D submission when Filing. In our experience most companies create a report of around 4-6 pages detailing the project and the rationale against each of these tests. Note that this report needs to be converted into the pdf format.

Step 2 - Keep a note of all costs and time spent on R&D

You may be fortunate and have a ring fenced R&D team, however, it's likely that you will have fungible resources that work on other (non-R&D) activities. You may also have multiple R&D Projects which will require a separate R&D report for each.

If you have a time booking system you can use that so that people allot hours. Otherwise you may need to work out a proportion of time using your justifiable discretion.

Step 3 - Make a CT600 return include R&D amounts & attach the R&D report(s)

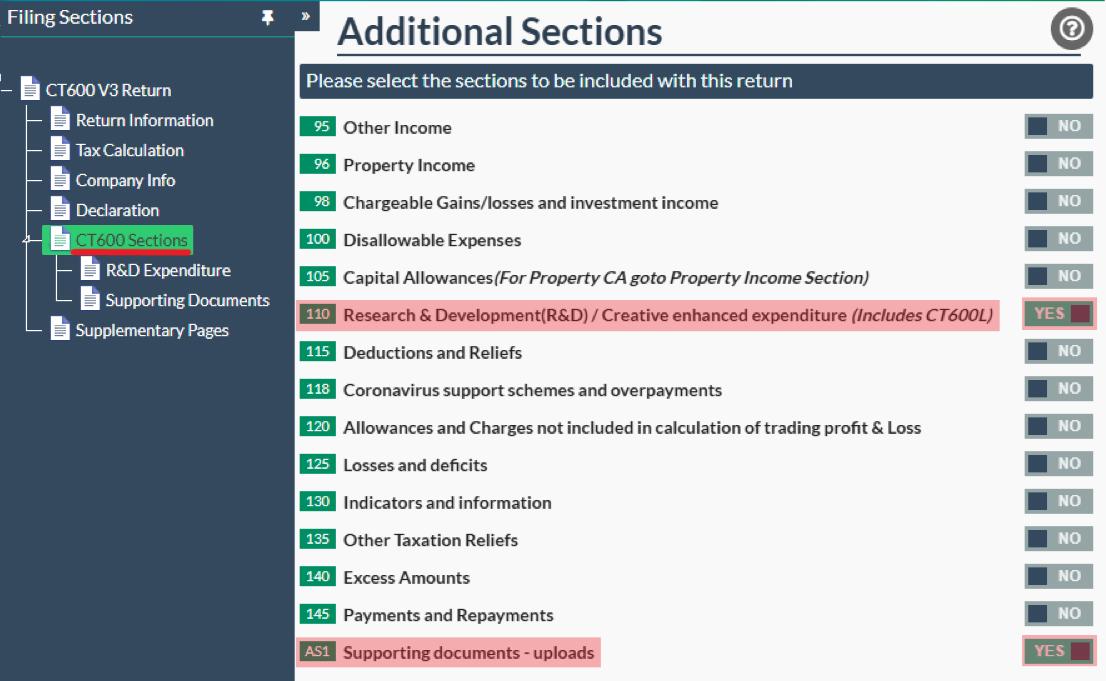

When your accounting period has ended and you are ready to file, you can create and open your CT600 Filing and select the section "Research & Development(R&D) / Creative Enhanced Expenditure", by switching box 110 to 'Yes' in the 'CT600 Sections' tab. When you select yes the supplementary section will be visible in the section navigator.

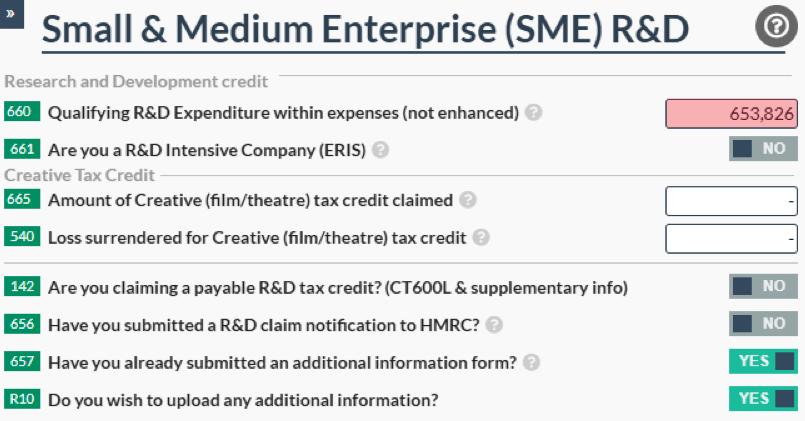

Once the 'Research and Development' page has been created, you will need to enter the total qualifying spend on R&D into box 660. Please also ensure that you have included this amount within the 'Operating costs' box (E1) in the 'Tax Calculation' page. Using these figures, our software will automatically calculate your enhancement and the tax credit due (if applicable).

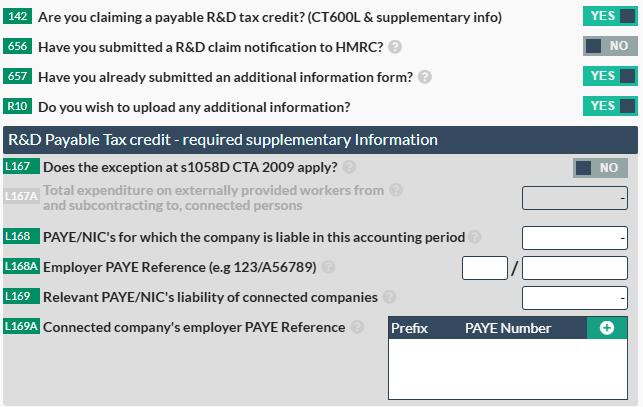

If you are claiming a tax credit, you will need to switch box 142 to yes - this will create the CT600L, where you can fill in the relevant additional fields. Please ensure that this is only switched to 'Yes' if your company was loss making and is claiming the payable tax credit - if you are profit making the software will still calculate the enhancement for you and the reduction in the corporation tax liability when this box is switched to 'No', as the CT600L is not required for in this scenario.

If the s1058D CTA 2009 exemption applies, please click box L167 to yes and complete L167A.

If you have made any PAYE payments or NIC contributions, please complete box L168 and L168A (also boxes L69 and 169A if applicable). We will then be able to accurately calculate the amount of tax credit payable.

To check how much tax credit you are claiming, please click on the 'Payments & Repayments' tab (this would have automatically been created when box 142 was switched to Yes) - the amount due back to the company will be shown in box 865.

Please ensure that you also complete the bank details section within this page of the account that you would like the tax credit paid into.

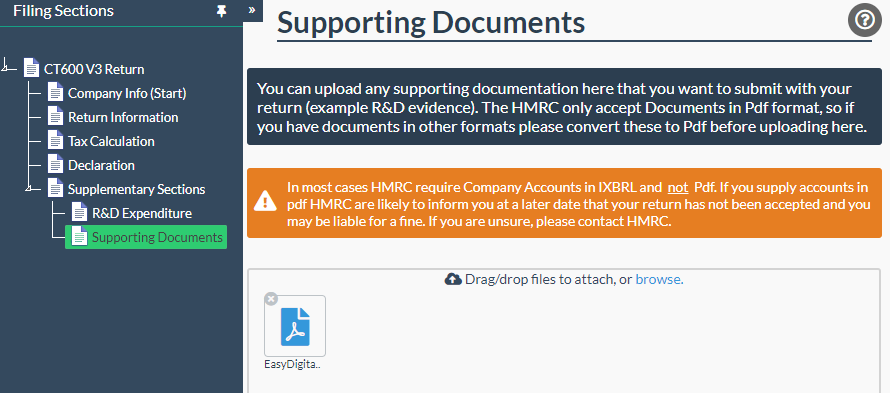

Attach your R&D supporting documentary evidence.

Since August 2023 there are additional documentary requirements HMRC require to be completed before submitting an R&D claim.

Additional Information Form:

All claims made from August 2023 must include the submission of the additional information form (AIF). This has to be completed and submitted to HMRC each time you are making an R&D claim, and it must be submitted before you can complete and submit your CT600 return. HMRC will not accept the claim in the CT600 return if the additional information form has not been submitted first.

Claim Notification Form:

For companies that are making an R&D claim for the first time, or the first time in three years, then they will need to complete a claim notification form and submit this to HMRC directly through their website. Once again, this must be completed and submitted to HMRC before you can submit the CT600 return with the R&D claim, as otherwise they will reject the claim.

If you have any other additional information that you would like to include, you can upload this within our software by attaching it in the 'Supporting Documents' tab. To get here, please switch box AS1 to 'Yes' on the 'CT600 Sections' tab.

Review your R&D costs against your other return inputs

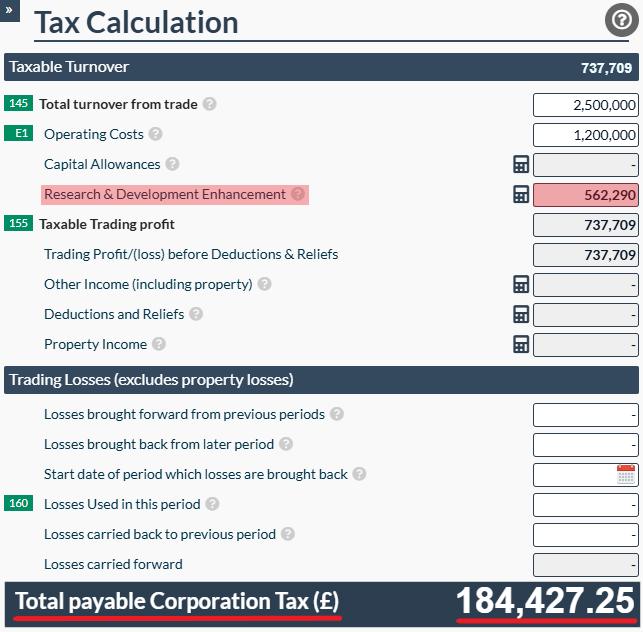

In our example below, the company had £2,500,000 of income, with £1,200,000 of expenses (which already include all costs including R&D ). The R&D enhancement has already been calculated for them by our software - resulting in an enhancement of £562,290 (post April 2023).

This has reduced the company's taxable trading profits, as 86% of the qualifying R&D costs (£653,826 * 86% = £562,290) have been added in as an expense - thus reducing the corporation tax due.

If we had not claimed R&D, then our taxable turnover would have been £1,300,000 (which is £2,500,000 - £1,200,000), and at 25%, the total corporation tax would have been £325,000. With the R&D claim, the total corporation tax due is £184,427.25, meaning that the company has saved £140,572.75 by claiming for R&D.

Payable Tax Credits

If you choose not to opt for a R&D tax credit, then you can carry the total loss, including the enhanced loss generated by R&D calculation forward to your next period to off-set against future profits. Find out more about moving losses from period to period. You can find out about losses through our article 'How to use losses in a Corporation Tax return' on our Knowledge Base.

You can use our R&D Online Calculator to find out how R&D Tax relief can reduce your CT liability, potentially pay you a tax Credit if you are Loss making and help your business's cash position.