HMRC

If HMRC requires, you will need to submit your limited company accounts and tax return to HMRC, these will be due 12 months after the end of your accounting period. HMRC will typically request a Corporate Tax return by a 'Notice to File' letter posted to the company's registered address, sent approximately 2 weeks after the end of the Company's first accounting period. It's important to note when your accounting year ends so you can work out when this is due.

If you are filing for your first period after incorporation, you may have a period to report on that is more than 12 months. If this is the case you will need to complete 2 CT600s (the company tax return) plus 1 set of accounts to cover the whole period.

Please note that any tax due for the accounting period, will be due 9 months and 1 day after the end date of that period. If your limited company does not owe any corporation tax, it's important to let HRMC know this before the end of the due date.

You will also need to have created a government gateway account and activated your corporation tax service.

Companies House

Accounts to Companies House are due 9 months after the end of your accounting period, which can easily be checked on your Company page on the Companies House website under the Accounts Section in 'Overview'. Your Companies House page was set up at the date that your Limited Company was incorporated.

You will need your Companies House Authentication Code to be able file your accounts. This will have been issued to you when you incorporated your Company. If you have any trouble locating it, you can issue a reminder to be sent to the company's registered office.

However, it's noteworthy that if you are filing your first year's accounts, the deadline will be 21 months after the date that the company registered with Companies House.

Here is a summary of the key deadlines listed below:

| What is due? | Deadline |

| Company Tax Return due to HMRC | 12 months after the end date of the company's accounting period for corporation tax |

| Any Corporation Tax due to HMRC/ notify HMRC that the company does not owe any | 9 months and 1 day after the end of the company's accounting period |

| Filing first year accounts to Companies House | 21 months after company registration with Companies House |

| Filing annual accounts to Companies House | 9 months after the end date of the company's accounting period |

Preparing Financial Record

Having well prepared company financial records are important when coming to prepare your end of year filing of Company Accounts. Here are some potential statements or records that you should collate before filing.

- Company Bank Statements - that include the company's income and expenses

- Record of any Company Assets purchased within the period

- Gather all business expenses receipts and any invoices issued to customers

- Record of any loan contracts - Loans owed to or by the company, or to a third party

- Any payroll records - if your limited company has employees

Before proceeding to complete your company accounts, it's good to log your total income and expenses for the period. These can be recorded in either book-keeping software, a spreadsheet or by pen and paper if you'd prefer. Whatever form of account logging best suits you for when you come to file the end of year accounts!

Accounting Period

It's important to collate all of your limited company's financial records within the correct period. When referring back to the company's bank statements, check that all of the income and expenses you're recording fall within the correct dates. Gathering the end bank balance for the period will be important later on when filing the company accounts.Income Statement

Now that all of your company's financial records have been collated, you're ready to file your company accounts! Once all of the correct figures have been reported, you're able to fill out the Income Statement, also known as the Profit and Loss Statement, with the company income and expenses.Our software provides both micro and small company accounts templates, including both an Income Statement (P&L) and a Balance Sheet.

The company accounts can be filled out and submitted to HMRC (along with a CT600 return) and/or to Companies House (along with a Companies House Submission form) which we also provide templates for. These can be selected under the 'Add Filing' section in your account:

Company Income and Expenditure

When logging the company income and expenses, it's important to input them in the relevant categories. We have a useful article in our Knowledge Base on how to complete the Income statement, where it breaks down each section: What is a Profit and Loss Statement in Company Accounts?

Balance Sheet

The next stage of your accounts filing is completing the Balance Sheet, I have listed below some notable company incomings or outgoings that could be accounted for in the sheet.

Company Assets

A good way to start is to look for anything purchased that might be considered a "fixed asset" when looking through company bank statements, this should be recorded as such on the Balance Sheet. This is anything purchased within the accounting period that would have a useful life of over a year.

This could include purchases of:

- Property

- Heavy machinery or vehicles

- IT equipment

It's important to estimate what the useful life is for any of your fixed assets as you will have to account for the depreciation for certain assets. If you would like to know more about calculating and entering depreciation into your accounts you can check out our article on deprecation How to Account for Depreciation in The Accounts & CT600.

Additionally, you will need to log your end of accounting period company bank balance in the Balance Sheet. This is considered a "current asset" and should be recorded in this section. Current assets may also include any unpaid invoices, which if applicable will need to be added.

Outstanding Loans

Make sure to check for any loans due either to or from your Limited Company, which should be evident in the company financial records. These are not entered into the Income Statement, but are required for the Balance Sheet.

Loans Owed to the Director

Any loans owed to your company director, that are not paid off within the accounting period have to be recorded in the 'Creditors: Due after more than one year' section of the Balance Sheet, along with any unpaid loans from last year's section that need to be carried forward.

In addition, any loans due to any third parties can also be recorded in this section. The final Creditors due figure should be the remaining balance or amount due of any existing loans that are not fully paid off yet.

Loans Owed to the Company

Loans owed to the company, by the director can be considered a Current Asset and entered as such in the Balance Sheet. If an existing loan owed to the company is paid off by the director, it can be offset by deducting any amount paid off from the Current Assets.

Adjustments for Accruals and Prepayments

Another section of the Balance Sheet that is worth noting is the prepayments and accrued income section. This only needs filling if you have to account for items the company has paid for within the period, but not yet received or any income earned by the company that has not yet been paid.

There is also a section for accruals and deferred income, which only needs to filled if the company has received any payments but itself has not provided any goods or services yet.

Balance Sheet Review

Concluding the Company Accounts, it's essential that the Balance Sheet figures "balance", moreover that your Net Assets and your Capital Reserves should be equal in value.

Net Assets

The Net Assets are calculated automatically through our software, once you enter in all of the applicable sections, whereas the Capital and Reserves need to be calculated. In our Company Accounts template in our software, there is a help icon adjacent to the Capital and Reserves section telling you how this needs to be calculated, and making the figures balance should remove any error notifications on the Balance Sheet.

If you find that the figures are still not balancing, it's important to check you have accounted for all the incomings and outgoings of the company for the entire period. Please read our Balance Sheet Basics article, explaining how every section is filled in.

The final requirements of the limited company accounts files are that the Principal Activity is filled in and it's signed off on the Directors Report & Declaration page. Through our software, you can head to the Balance Sheet Notes, where this can all be inputted in section 4.4.

Calculating Corporation Tax

If you are required to submit to HMRC, you will have to fill out a CT600, this is usually when your company has income and expenses, but sometimes HMRC can request accounts even if the company is dormant. As mentioned earlier, it's a good idea to check whether HMRC have requested any accounts, as you will usually have received a notice to file by post.

If it's your first-year filing, this typically means that you will have an extended accounting period, as accounts are usually due at the end of the month. (For example: a company that incorporated on the 16th June 2023 will typically have a first-year accounting period of 16th June 2023 to 30th June 2024.) HMRC don't accept Corporation Tax accounting periods longer than 12 months, so you will require 2 CT600s to cover the whole period

Tax Calculation

The Tax Calculation page of the CT600 return is where you will need to input any company turnover or operating costs. We have another article in our knowledge base that explains how to file a CT600 online with our filing software. This covers where to input the company's income and expense figures to calculate the tax due to HMRC, and provides an easy step-by-step guide on how to prepare and submit the CT600 return.

Accounting for Corporation Tax

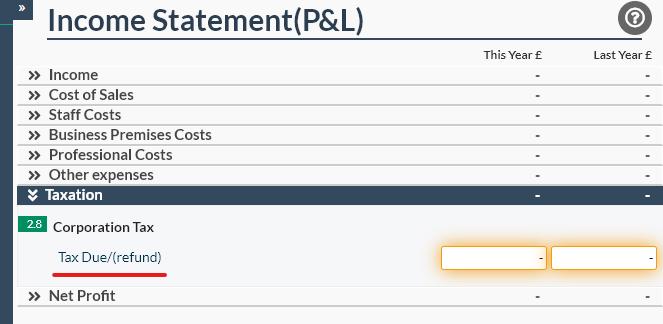

Once you've completed all of the applicable sections of the CT600, you're now ready to add corporation tax. Any corporation tax due to HMRC has to be accounted for in both the Income statement and the Balance Sheet. On the Income Statement, the tax is recorded under the "Tax Due" section.

This should reduce the overall net profit by the amount of tax, meaning the Capital and Reserves figure calculated earlier, inputted on the balance sheet will need to be reduced by this amount as well. In order to keep both sides of the Balance Sheet equal, any corporation tax due will also have to be added to the 'Creditor's: Amount falling due within one year'.

Preventing a Rejected Filing

As one of the final steps before filing your company returns, it's a good idea to review your Company Information. This is so you're more likely to avoid any filing rejections from HMRC or Companies House. The most common rejection is due to an authentication error, meaning that there could be errors with either the HMRC or Companies House Credentials.

HMRC Gateway Credentials

If you're filing with HMRC, it is required that you provide your limited company's Unique Tax Reference (UTR) number, which is a 10-digit number issued at the time of your company's incorporation. Your HMRC Gateway Account username and password are also required, these can be input under the Company Information section.

Sometimes it can be hard locating your UTR number when either looking online or sifting through documents. In which case, you can contact HMRC directly and request the UTR. The waiting time for this is usually about 10 working days, but can take longer.

Companies House Credentials

When filing to Companies House, they require an authentication code which you should have received shortly after incorporating your Limited Company. This is a 6-figure alphanumeric code that you can also enter in our software under the Company Information section before submitting your filings.

Ready to Submit Company Accounts

Once all your limited company filings have been completed and all your company info has been input and reviewed, you're now ready to submit to HMRC and/or Companies House!

Through our software, you can purchase one of our packages that best suit the accounts you wish to submit. The packages can be purchased either before or after you complete your necessary filings! You can view the different packages we offer through the 'Purchase Services' tab in your account, where each product is broken down into what is included.

Chat with us!

Completing company end of year accounts can sometimes be overwhelming. In the case that you require any technical help when completing your accounts. Send us a message or use the 'chat with us option' in your Easy Digital account. If you don't already have an account, our filing services are free to use and you only pay whe you're ready to file. Get Started or visit Easy Digital Filing to find out more about our user friendly tax filing platform.