Let’s explore what happens when you overpay your Corporation Tax and how you can sort it out without the hassle!

Corporation Tax- covering the basics

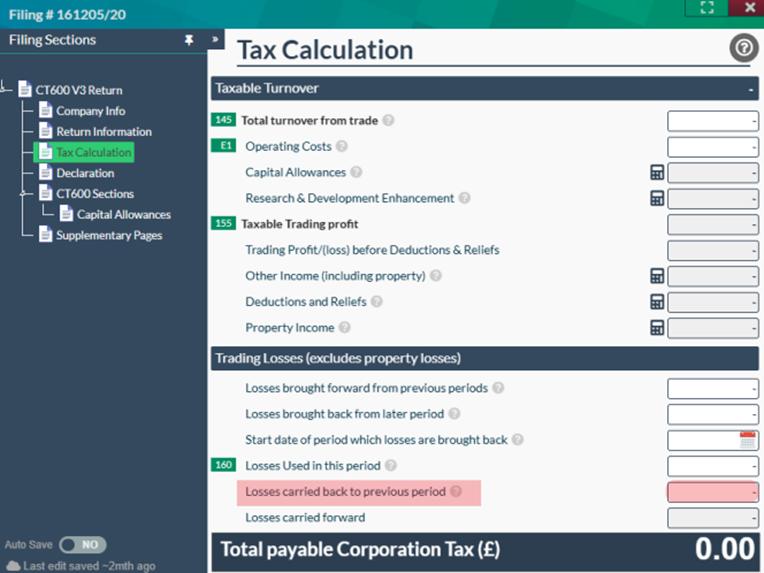

How is Corporation Tax calculated?

Working out the company’s taxable turnover means you start with the total income, which includes sales of goods or services, bank interest, property income, sale of assets or any other sources of income the company makes.

Calculate the allowable business expenses and overheads that can be deducted from the company’s total income. A few examples include travel, insurance, rent, purchases, salaries and wages, subscriptions, general administrative expenses. For limited companies, when claiming expenses, the expenses incurred must be "wholly, exclusively and necessary" for business purposes.

Any expenses that are not 100% business related are to be reflected as a disallowable expense in the CT600 Return. Such expenses cannot be deducted from your taxable income. For example, late filing penalties from HMRC and Companies House, client entertainment, depreciation expenses are typically not tax deductible.

Check for capital allowances. You may be eligible to claim capital allowances on fixed assets, which allow you the benefit of deducting up to the full cost of the asset from your profits before tax, ultimately reducing your taxable profits.

Apply the appropriate Corporation Tax rate—either 19%, 25%, or a rate in between based on Marginal Relief, which uses a sliding scale.

What are the filing and tax payment due dates?

Limited Companies are expected to file the Corporation Tax return 12 months after the end of the company’s accounting period.

For taxable profits of up to £1.5 million, HMRC expects corporation tax to be paid 9 months and 1 day after the end of the company’s accounting period. For example, if the company’s period is 1 June 2023 to 31 May 2024, HMRC will expect corporation tax to be paid by 1 March 2025.

Although it may seem unusual, HMRC expects the tax to be paid before the tax return is due to be filed. As a result, it's easy to see how companies might overpay Corporation Tax, especially if the final figures differ from initial estimates.

But, if your taxable profits are more than £1.5 million but less than £20 million, also defined as a large company, you should pay your Corporation Tax in instalments, which also requires you to estimate your company’s total liability for the full period and then work out the 4 quarterly instalments.

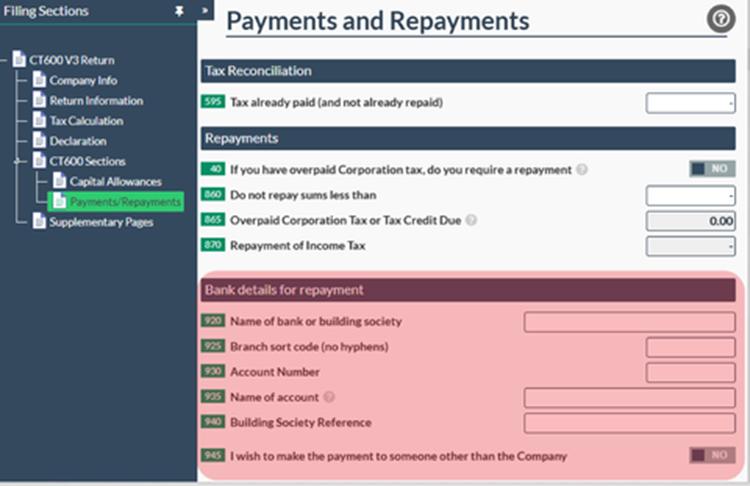

If you pay Corporation Tax early based on estimated figures, and the final liability submitted in the tax return is lower, you’ll be entitled to a refund of the overpaid amount. If you don’t want a refund (by not inputting your bank details in the tax return), HMRC will use the money owed back to you against other tax owed by your company, such as VAT or PAYE. Alternatively, the amount will be used to pay off your next Corporation Tax bill or any late filing penalties.

Additionally, if you’ve overpaid, HMRC will pay interest on the refund calculated from either the due date of the tax or the date you made the payment, whichever is later.

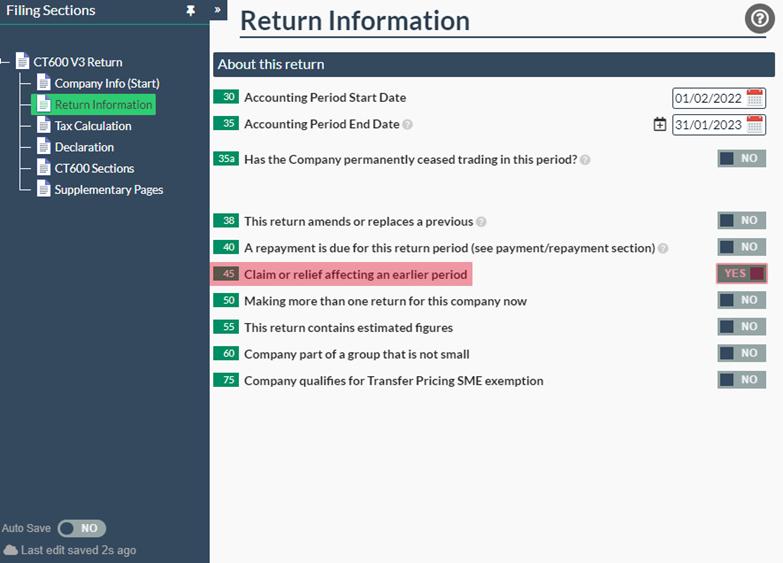

You may have overpaid due to errors in the company tax return, such as inaccurate reporting of income and expenses, or by failing to claim capital allowances or apply available losses against profits. If this happens, it’s best to file an amended tax return, but, it’s important to note that there is a deadline of 12 months from the statutory filing deadline date when filing amended returns.

What about refunds from carrying back losses?