If you are the director of a company, one of the many tasks that you must complete each year is submitting your corporation tax return and paying any tax that is due! But there is a question that always lingers on people’s minds when filing season comes around – and it’s ‘is there a way I can reduce my tax?’. While there is no simple “hack” that helps you remove your company’s corporation tax, there are many ways that you can reduce it – so let’s get into it!

What is corporation tax?

First of all, let’s discuss what corporation tax is and how it is calculated. Corporation tax is charged on a company’s taxable profits, and is expected to be paid every year, nine months and one day after the end of their accounting period. There are different rates that are charged, depending on the company’s accounting period that they are filing for, and their total taxable profits.

For most companies, they will be charged corporation tax at the main rate of 25% - this is for all company’s whose taxable profits are over £250,000. There is also a small profits rate, charged at 19%, which applies to small or micro companies, if their taxable profits are under £50,000. For companies whose taxable profits fall between £50,000 and £250,000, there is a tax relief scheme known as Marginal Rate Relief. Through this scheme, the company is taxed at 25%, but then they get a tax reduction, which can change depending on whether the taxable profits are closer to £50,000 or £250,000.

Let’s say that a company has income of £45,000 and allowable expenses of £23,560 – this leaves us with taxable profits of £21,440. As the taxable profits of this company is below £50,000, they will be charged tax at the small profits rate of 19%, so the total tax due for the period is £4,073.60.

Now that we’ve covered the basics of corporation tax, let’s take a look at how you can reduce it!

1. Capital Allowances

If you purchase larger items that you intend you use in the business for longer periods, then these would typically be considered as fixed assets, thus reflected in the balance sheet rather than the income statement. But in this case, the purchases wouldn’t be considered as expenses since they are not in the income statement - so how do you benefit from buying them? That’s where capital allowances come in.

A capital allowance is a type of claim you can make on the purchase of fixed asset items, such as laptops, equipment, vehicles and many more! There are different types of capital allowances that you can claim, with different rates, that depend on the item that you purchased. These allowances are essentially added as an expense to the company’s taxable profits, so that they are reduced, thus reducing the tax due as well. This means that although these items are not included in the income statement, they still offer a tax benefit as you can claim capital allowances on them – so it is always important to remember to make the claim!

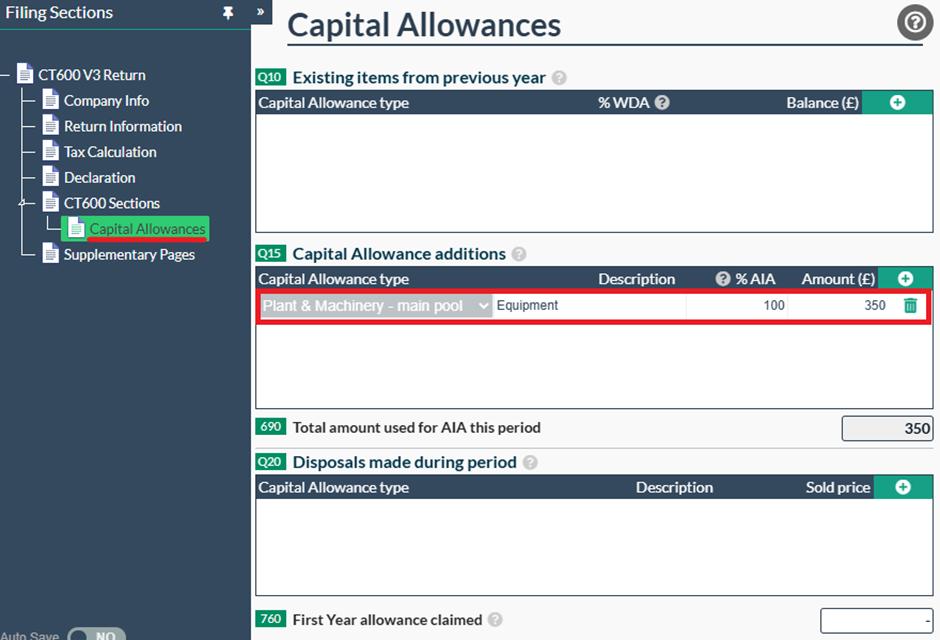

Within our software, there is a quick an easy way you can claim capital allowances – simply head to the CT600 Section tab within your CT600 return, switch box 105 to Yes, and then add your items in the necessary boxes within that page.

Once entered, our software will automatically take it into account the capital allowance and use it to reduce the taxable profits for you! You will be able to view the full deduction in the Tax Calculation page.

For more on capital allowances, please read our article ‘How to claim capital allowances on a corporation tax CT600 return’.

2. Research & Development

Another tax relief scheme that is available for companies which helps reduce their corporation tax is the Research and Development claim. There are two types of claims that you can make, depending on your company’s size and taxable profits/loss, and they either offer a reduction on the amount of corporation tax due, or they can offer a tax pay-out. If your company has invested in any R&D, then it is worth making a claim, no matter the amount of qualifying expenditure, as any small claim will help reduce your tax due.

From the 1st April 2024, HMRC updated their R&D scheme to include two different types of claims – one is under the merged RDEC scheme, and the other is under the ERIS scheme. The merged RDEC scheme is available for companies who are either profit making or loss making, and covers micro to large entities, as all can file under this claim. While this scheme is more accessible, it offers a slightly lower tax benefit as the rates under this scheme are slightly lower. You can find out more about this scheme and how it works in our article ‘What is the Merged RDEC Scheme and how does it work?’.

The other type of claim you can make is under the ERIS scheme, which can only be claimed by companies who were loss making pre-R&D. This scheme offers an enhanced expenditure, which increases the company’s losses, and also offers a tax credit payment. For more information on who can make a claim under this scheme instead, please feel free to check out our article ‘What is ERIS? Enhanced R&D Intensive Scheme Explained’.

3. Wages Vs Dividends

A common question that plays on directors’ minds is whether it is better to take wages or dividends when being paid by your company. Each one offers different benefits to either the company or director, but only one helps reduce the amount of corporation tax that is due.

While dividends offer a lower personal tax rate than when paid a salary, meaning that you may pay less income tax, they are not reflected in the company’s profit/loss statement. They are then not included as an expense within the company’s tax return either, thus do not affect the amount of corporation tax that is due.

Wages, however, are an allowable expense so they are reflected in both the company’s income statement and in the corporation tax return itself. This means that if you pay yourself or your staff wages, these are added as an expense, thus reducing the total taxable profits, which in turn, reduces the amount of tax due on them. Another point to note is that not only are the wages allowable, but any national insurance contributions and any pension contributions made by the company are also allowable, and can be added as an expense for the company. So, by paying wages and the contributions that go with them, you can significantly reduce the amount of corporation tax due.

For more on the tax benefits that dividends and wages offer, please feel free to read our article ‘How Do You Pay Yourself from a Limited Company?’, which is explains each in more detail and how to account for them.

4. Track All Business Expenses

While this goes without saying, it is extremely important to ensure that you are keeping track of all your business expenses, big or small, as they can all make an impact to your corporation tax. You need to ensure that you account for all expenses, whether it is a £2.50 postage fee or a £1,000 stock purchase, as all of them can make a difference to the amount of corporation tax you owe.

For example, if you buy a £10 train ticket for travelling just to a client's site and back to the office a few times a week, then you can claim these costs as an allowable expense for the company. While it may not seem like a lot, if you keep track of each ticket that you buy and add it up over the entire year, it can make a significant difference to the amount of corporation tax due.

Let’s say that you took the train three times a week for 20 weeks out of the year - that would equal total travel expenses of £600 for the period. If the company had taxable profits of £8,000, then their tax would have been £1,520. If they then add the travel expenses of £600, the taxable profits would be £7,400, and the corporation tax due is now £1,406 - that offers a tax reduction of £114. While this may not seem like a lot, it can make a big difference to a small company.

The only rule to remember when claiming for expenses is that everything must be 100% business related. For example, you can’t start claiming for your electricity bill if you work from home, but if you rent out an office space dedicated for your business only, then you would be able to claim for this expense.

5. Use Your Losses

Another way to reduce corporation tax due is by using any losses that you either made in the period or any losses that you have carried forward to offset against your company’s taxable profits.

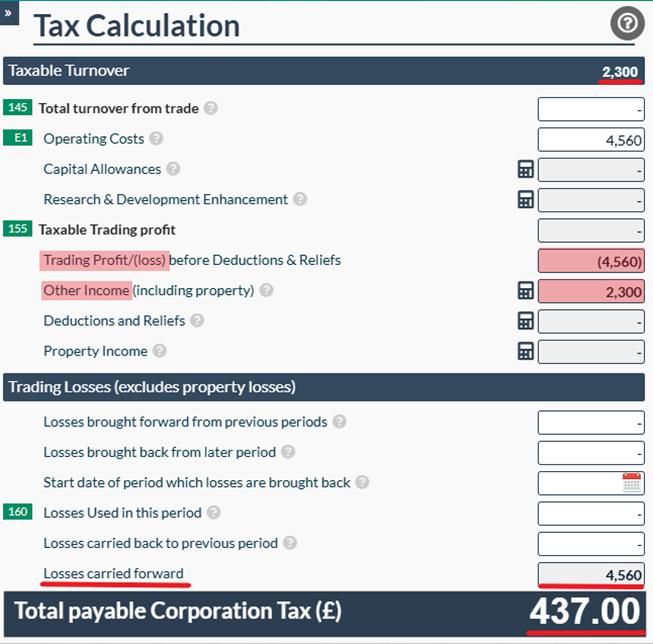

If your company made a loss in the period, but their main income was considered as ‘Other income’ not relating to their trade, then they can use their trading losses incurred in that period to offset against their non-trading profits. For this example, let’s say that a company had interest income of £2,300, and total expenses of £4,560. Without using their losses against the other income, there is tax charged on it of £437 (which is £2,300 x 19%).

As you can see, once you enter the losses used in the deductions and reliefs page, the total taxable profits are reduced, and there is no tax to pay.

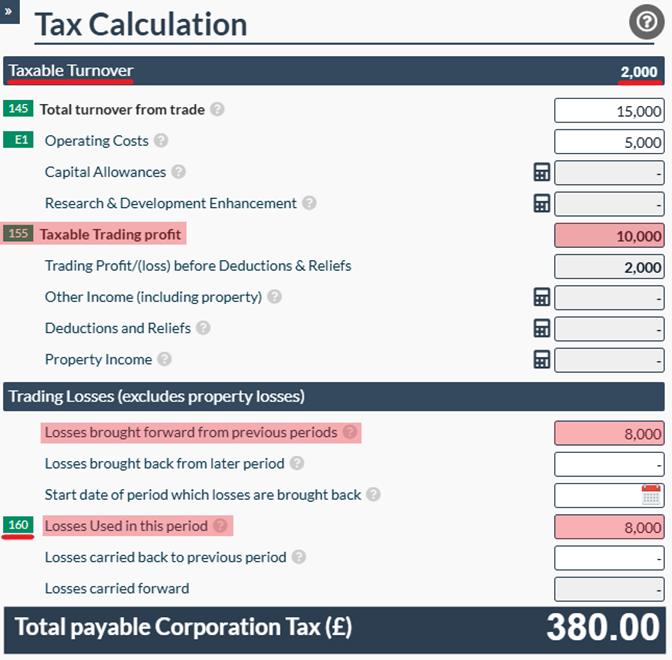

Another scenario would be if the company had made a taxable profit this period, but a loss last period, meaning that they had trading losses to carry forward. In this situation, you simply need to enter the total losses carried and total losses used in box 160 on the Tax Calculation page to reduce the corporation tax due.

In this example, the company's taxable profits for the period were £10,000, so there was corporation tax due of £1,900. However, they also had losses carried forward of £8,000, which they used to reduce their taxable profits down to £2,000, leaving them with corporation tax of £380. That’s a big change!

It is so important to keep track of any losses that your company incurs each year as these can be carried forward and used to reduce corporation tax that is due in the future.

For more on losses, please feel free to read our article ‘How to use losses in a Corporation Tax return’.

To Conclude

Now you should have a good idea on how to reduce your corporation tax for the period, whether through capital allowances, research and development claims, using your losses, and many more! You can get started on your tax returns today by creating an account and adding the filings! Please feel free to check out our article ‘Can I file my own Corporation Tax Return?’ if you are unsure where to begin. Furthermore, if you are still struggling to complete this on your own, we do offer a managed filing service where one of our account specialists will complete them for you. Find out more about this here.