Before we get into the details, what is a chargeable gain?

A chargeable gain is the profit a company makes when it disposes of an asset that has increased in value. For example, if a property, that is not your main residence, was bought for £120,000 and later sold for £300,000, the gain on the sale is £180,000. Depending on whether you are reporting as a limited company or an individual, you will need to pay either tax on the profit through your corporation tax return or through capital gains tax that may be due on that £180,000.

But, what does "disposing of an asset" actually mean? According to HMRC, disposal includes:

- Selling the asset

- Giving it away as a gift (except to a spouse or civil partner)

- Transferring it to someone else

- Swapping it for another asset

- Receiving compensation for it — for example, an insurance pay-out due to loss or damage

Who pays Capital Gains Tax?

CGT is payable by private individuals, trustees, sole traders (self-employed), partners in a business partnership on gains from the disposal of certain assets. Limited companies on the other hand do not pay CGT, they pay Corporation Tax on the chargeable gains.

Chargeable assets that you pay tax on the gain includes:

- Most personal possessions valued at £6,000 or more, excluding private vehicles (cars)

- Property that is not your main residence

- Your main home, if it has been rented out, used for business, or is exceptionally large

- Shares held outside of an ISA or PEP

- Business assets

There are some assets that are exempt from Capital Gains Tax (CGT). This means that if such an asset is sold, no CGT is payable, and any losses on disposal are not allowable either.

One key category of exempt assets includes certain chattels, but what exactly is a chattel?

It’s defined as anything that is a tangible moveable property. HMRC breaks this down further to state that all forms of property can be assets, and does not refer to being attached to land or buildings. For example: paintings, plant and machinery, furniture, jewellery. There are few questions that you should consider to help you determine if it is a chattel:

- Is the object physically tangible?

- Can the asset be moved with easy without damaging its surroundings?

- Can the asset be purchased or sold?

Chattels are further divided into wasting chattels and non-wasting chattels. A wasting chattel is one that has a useful life of 50 years or less, determined at the date of acquisition and generally exempt from CGT. Some examples of this include plant and machinery, clocks, watches, racehorses, and etc. Non-exhaustive list of other examples of assets typically exempt from CGT:

- Private motor vehicles, specifically cars

- Chattels acquired and disposed for £6,000 or less.

- Winnings such a betting, or from lottery

- Compensation or damages received – for personal injury or professional harm

- Shares in an Individual Savings Account

- Qualifying corporate bonds

- Gilt-edged securities

- Save As You Earn schemes

- Business expansion scheme shares

How is the gain calculated?

To calculate the gain, you consider the difference in value of the asset when acquired and the value at which it was disposed at but also deduct any incidental costs of sale and purchase and money spent improving the asset. You’ll then have the chargeable gain.

There is the tax-free allowance to consider, which is also known as the annual exempt amount. For the current tax year 2025/2026, it is £3,000. You can use this amount to reduce the amount of tax you owe. here are different rates applicable for CGT, which can be found directly on the government website, but just to explain an example, let’s look at individuals (not including carried interest gains). From 6 April 2025 onwards, for residential property gains, the rates are 18% and 24%. The 18% applies to gains that fall within the individual’s basic rate income tax band, and the 24% applies to gains that fall above that (for higher rate or additional rate income tax payers). For other assets, the rates are 10% and 20%, respectively. It’s also necessary to take into consideration total taxable income, the personal allowance, and any other reliefs including the AEA (£3,000).

What happens when companies sell business asset?

Your limited company will be liable to pay Corporation Tax on any gains arising from the sale or disposal of business assets. Examples of business assets include: plant and machinery, buildings, land, shares - essentially, anything owned by the company that has value.

Capital losses occur when an asset is sold for less than its original purchase price. These losses can be deducted from any chargeable gains in the same tax year to reduce the overall taxable amount. If the losses exceed gains in that year, the remaining capital losses can be carried forward and used to offset future chargeable gains. However, capital losses cannot be set against trading income or other types of profits.

Let’s go through a simple example on how you can do this through Easy Digital:

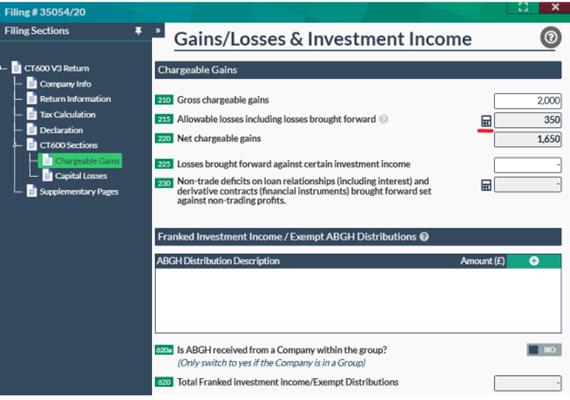

Suppose you disposed of a company business asset (e.g., machinery) and made a £2,000 gain. For simplicity, let’s assume the company has no other income or expenses and you’re filing for the 2023/24 period.

You’ll need to reflect this in the chargeable gains page of the CT600 Return. To find this, please switch box 98 to YES in the CT600 Sections page.

The £2000 would be entered as gross chargeable gain. At this point, the Corporation Tax payable is £380 (£2000 x 19%). Any existing capital losses from previous periods can be carried forward and entered by clicking the calculator icon for box 215, which opens up the capital losses page.

We’ll say that £350 of capital losses were brought forward and all £350 of allowable capital losses were deducted from the chargeable gain of £2000, giving a net chargeable gain of £1,650. Don’t forget to reflect this in box 1 and box 215 like below. The total Corporation Tax payable would then be £313.50 (£1,650 x 19%).

Box 2a is automatically calculated for you based on your entries from box 1 and 2. Any capital losses that are not offset against chargeable gains can be carried forward to future periods and utilised accordingly and this will be populated in box 3.

That's it! More details about selling fixed assets . Aside from that, keep an eye out for important updates and find guidance on filing through our software in our knowledge base space!