In this article we look at how each section of a balance sheet works to help you balance and file micro company accounts. However, if you need more detailed guidance on filling in your profit and loss, please see our related article on How to Create Micro Entity iXBRL Company Accounts

Balance Sheet Demystified

The balance sheet is the area of accounts that seems to cause the most confusion. It is made of 2 halves, and as the name suggest these must balance. The top part is the net assets and the bottom part the capital and reserves, and the two halves need to be equal and balanced. Well that is the theory and in practice that seems to be the difficult bit.

Your net assets are everything the company owns, including cash held in the bank, fixed assets and other assets minus your liabilities, these include bank loans, overdrafts, taxes dues to HMRC and any other debts.

Your capital and reserves are the share capital issues when you incorporated plus your net retained profit for the year. This is the figure that is taken from your profit and loss account after tax. Add your retained earning from previous year to this figure, minus any dividends you have paid in the year.

Download The Basics:

Get your copy of our super useful PDF guide to understanding the balance sheet for free:

https://easydigitalfiling.com/downloads/Balance-Sheet-Guidelines.pdf Alternatively, read on to find out how to fill in the balance sheet using our filing software, or scroll down to view the video guide.

Day 1

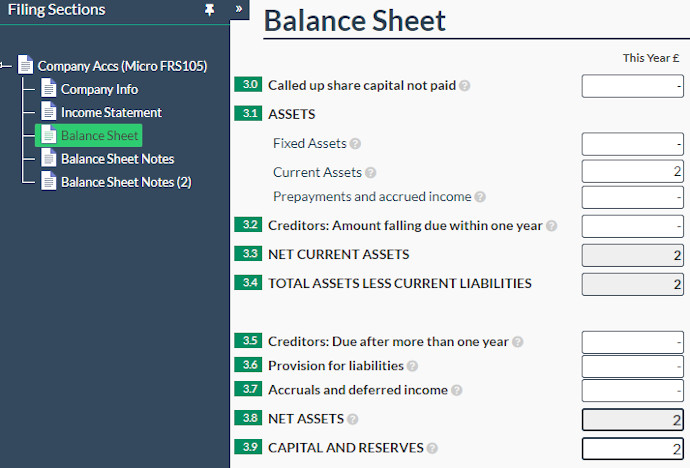

On the first day you incorporate your company and issue shares as part of the incorporation process.

Often for micro companies this is 1 or 2 shares. Lets assume you issue 2 and give them a nominal value of £1 each. You therefore have a capital and reserve value of £2.

You can choose whether you pay for these shares or leave them as 'called-up share capital unpaid'. If you pay for them, you would put £2 in to your bank account.

This would give you a balance £2 of current assets (the £2 in your bank account) and £2 share capital. The balance sheet balances.

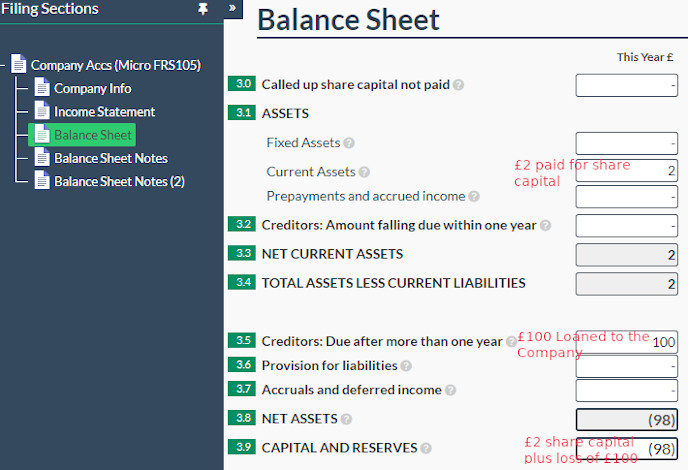

Day 2

You need an office or business premises, with an upfront fee of £100. This is a cost that you will enter into your profit and loss account. The profit (or loss) account will now have a loss of £100. if you need further information about creating a profit and loss account please refer to our Micro accounts article.

At the end of your period, the profit/loss figure will be added into your capital and reserve figure. Meaning your capital and reserves are -£98 (loss of £100 + your £2 share capital). Carrying on from the example above - that is great but your balance sheet, doesn't balance any more. Your net assets are still £2 but your capital and reserves are -£98.

Next consider how you paid for the rent. Have you got a bank loan, did you personally loan the company £100? – This loan, whether it is a bank loan or from yourself as a director should be shown as a 'creditor'. Usually payment to a creditor is due after a year, as realistically you probably will not be able to pay back before then. So your accounts are once more balanced.

Ok so that is day 2, but you are not going to be doing this every day, if you are using book keeping software, you will be able to look at the trial balance to check that everything is balancing. A trial balance is a breakdown of all your debits and expenditures through the period.

As the above is a very simplistic view, I will now go through the main parts of the balance sheet and explain what you need to do with each to ensure you keep a balance.

Fixed Assets

Fixed assets are items that last longer than a year, the accounting practice is to spread the cost over the items useful life. The costs of fixed assets do not therefore go in the profit and loss. The value is entered into the fixed asset area of the balance sheet. This actually does not have an effect on your balance – although your bank balance will have gone down by the cost of the item, your fixed assets will have increased by the same amount.

To ensure the balance sheet balances, you need to remember to include how you paid for your fixed assets. If you paid for them out of you bank balance that will reduce. However, if you used a bank loan to pay for the fixed assets, this will be shown as a creditor due.

Usually you depreciate or reduce the value of the fixed assets over its useful life. The reduction of value, is then entered in the profit and loss accounts as a cost. Please see our fixed assets article for further information about depreciation.

Current assets

In micro accounts there are several different components that make up current assets, I will go through them below:

Cash Held

Any cash you have in any of the company's bank account, is included as a current asset.

Stock

If your business holds stock, usually it would be counted as a current asset on your balance sheet, until the point it is sold. Once it has been sold, the cost of the item then becomes a cost of sale on the profit and loss and the sale price is classified as income, the difference is your profit! Please also see our article on Inventory

Trade debtors

These are people or companies you have issued invoices to, that have not yet paid. These net invoice amounts will be included in your total sales on the profit and loss.

Other debtors

This is any other money that is owed to the company.

Prepayments and accrued income

A prepayment is when you pay an invoice that covers more than one period. e.g if you pay office rent quarterly, depending on when

you paid your invoice you may have paid some rent that covers months outside the financial period you are reporting on. This part of the payment would count as prepayment.

Accrued income - this is income that has been earned but not yet received. An example could be bank interest that is already earned but will not be paid to the Company

until after the end of the accounting period.

Creditors Due

Now we have got all the companies assets identified, lets move on to the creditors - money the company owes.

These are items that have already been included in the expense part of your profit and loss (or else where in your accounts), however they have not as yet been paid for.

These are divided up into creditors that are due within a year. These reduce the value of your current assets and creditors due after a year. Creditors due after a year reduce the overall value of your assets. Creditors due include:

Trade creditors

These will be items you have purchased, they will have been included in the expense section of your profit and loss, however you will not have paid for them as yet. These are usually due within a year.

Corporation tax due

Include your corporation tax due for the period. This are usually due within a year.

Other tax and social security

If you are VAT registered and depending when your quarter falls, you may have VAT owing to HMRC. If you do please include the figure here.

The same applies if you have employees and have income tax or either employer or employee national insurance owing to HMRC. The cost of your wages and employer NI

will have been included in your profit and loss. These are usually due within a year.

Loans and overdrafts

If you have a loan, then this is a creditor, loans are usually creditors due after a year, it depends on when you think the company will be able to pay it back. Loans can be from a bank, a credit card debt or a loan that a director/friend/family member has lent to the Company.

Other creditors due

Include anyone else or body that that company owes money to. These can be either due within a year or longer.

Provision for liability

This is the amount the business puts aside to cover a probable future debt/liability.

Accruals and deferred income

Accruals and deferred income - These are the opposite of prepayment and accrued income, so when the Company has received income but not yet provided the goods or service.

View Our Guide to filling in the Balance Sheet: