To put it simply, the profit and loss statement indicates whether your company has made a profit or a loss over the period. It provides an overview of the company’s revenue and expenditure for the period and forms part of the company accounts, which need to be filed with HMRC and Companies House each year.

As well as delivering useful insights into the entity’s financial health, the profit and loss statement can help you make informed business decisions such as considering if the company has the funds to expand and grow the business.

You will be able to track the company’s growth in income by comparing it to previous period’s figures and analyse your different sources of revenue and identify the most and least profitable sources of income. Identifying trends and patterns in the company’s expenditure can also assist you in implementing solutions to reduce expenditure where necessary. It can help you come up with financial plan for the following period.

In the company accounts, gross profit is important to consider. This is calculated by subtracting the cost of goods sold/cost of sale from the company's income. As this expenditure are incurred directly from the production and the sale of the goods and service, it is important to monitor the expenditure for cost of goods sold and the income they bring in. The higher the gross profit, the more profitable and efficient the organisation is operating and utilising its direct resources. If your gross profit is low, you may have to consider the sale price of the goods and services being offered. Perhaps, you may need to consider cutting expenditure on the direct expenses, such as considering cheaper alternatives for direct materials purchased. There are a number of other ratios and indicators that you can calculate from your profit and loss statement to help you derive useful insights into the company.

How to complete the profit and loss through Easy Digital:

Before I explain how to successfully complete the profit and loss statement in the company accounts, it is good to know exactly which UK legal body requires the profit and loss statement. HMRC requires the IXBRL tagged full company accounts (profit and loss statement and balance sheet) to be submitted alongside the CT600 Return. Companies House, on the other hand, only require the balance sheet. However, you are able to submit full accounts to Companies House if you wish. It is definitely worth noting that the information that is submitted to Companies House will be publicly available and accessible on the register.

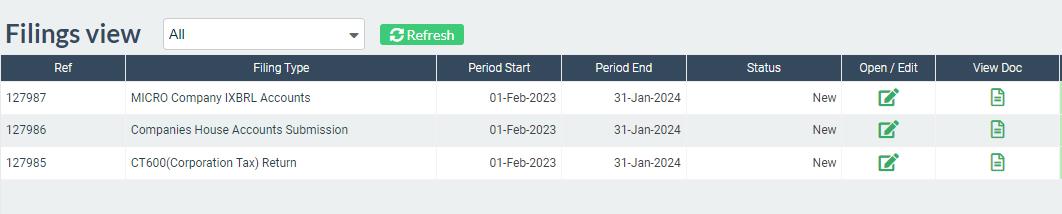

Let’s say Company XYZ LTD qualifies as a micro entity. With Easy Digital, I will be able to add the ‘Micro IXBRL Company Accounts’ template to my account as shown below. Whilst I am here, I will also add the CT600 Return + Companies House filing too. Under filings view, your company accounts will look like this:

If your company qualifies as a small company, you will be able to add the ‘Small IXBRL Company Accounts’ template instead! The income statement present in the small company accounts (FRS 102) is similar but offers much greater detail and breakdown than the categories mentioned below in the micro accounts (FRS 105). Find out more about the differences between micro-entity accounts and small company accounts.

QUICK TIPS!

It’s worth noting all your transactions that your company has incurred in the period for both income and expenditure , so that you can easily complete the profit and loss statement. Check your business bank account for the exact incomings and outcomings!

You may choose to track the company’s financial through a book-keeping software or if you prefer to record your income and expenses in a spreadsheet, that is also fine!

Breakdown of the key terminologies:

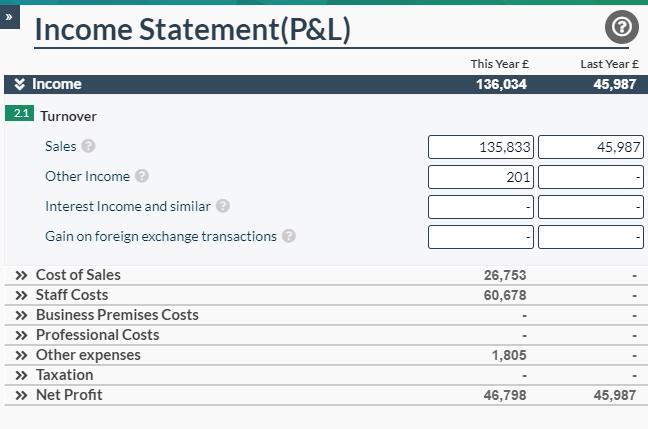

In the profit and loss statement in your company accounts, you will be able to enter your figures in the following categories: income, cost of sales, staff costs, business premises costs, professional costs, other expenses and taxation. Let’s discuss the key terminologies so that you can understand what they mean and if it is applicable to you.

BOX 2.1 Income is composed of money that you have received from sales, which is the company’s main trading activity. Income earned from other sources is reflected as ‘Other Income’. You will also be able to reflect interest income such as bank interest and any gains on foreign exchange transactions in the relevant boxes.

BOX 2.2 Cost of Sales is the cost directly involved in producing the goods and services sold during the period. It is also known as cost of goods sold (COGS). They include expenses such as raw materials, purchases of inventory, labour/wages, direct manufacturing overhead costs etc.

BOX 2.3 Distribution costs is the expenditure incurred for the delivery of the product from the production unit to the customer. Warehouse fees, transportation fees, and packing costs are some examples.

BOX 2.4 Staff costs include the wages and salaries of staff and directors, as well as other employee-related expenses such as pension contributions, employer’s national insurance contributions, etc.

BOX 2.5 Business Premises costs include expenses related to a rented office space used to conduct your business activities. Examples of relevant expenses are business rates, rent, utility bills, etc. The use of the home as an office space is also an allowable expense that can be reflected here.

BOX 2.6 Professional costs include costs paid towards a professional service such as advertising, insurance, accounting, legal costs, etc.

BOX 2.7 Other expenses offers a breakdown of other important expenses that a company may incur. Expenses such as postage and stationery, computer software, motor expenses, depreciation and amortisation, bank charges, travel, and subsistence can be reflected here. If there is no suitable category for any additional miscellaneous expenses, you can add them in the ‘other expenses’ field.

BOX 2.8 Taxation: Here, the amount of Corporation Tax due for the financial period is entered. This amount is derived from the tax calculation page of the CT600 return. If you are due a refund, please enter the amount as a negative figure by adding a minus sign before the amount.

This nicely takes you to the auto-populated profit/loss figure, based on your previous entries above, which will clearly indicate if your company has made a profit or a loss in the financial period.

How can I view the profit and loss statement?

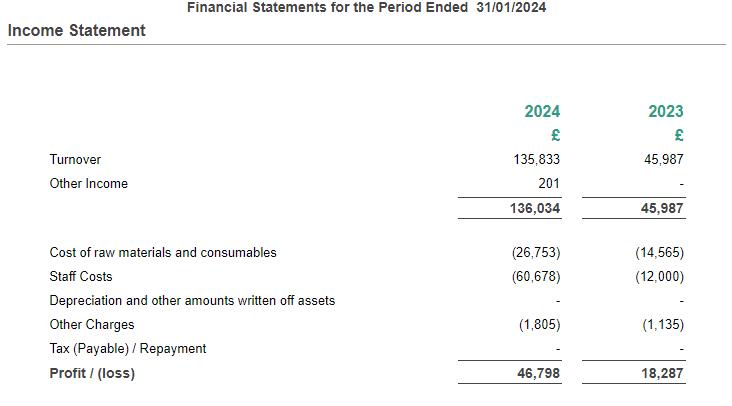

To view the profit and loss, please click the document icon under the ‘view doc’ column of the Micro Company IXRBL accounts.You will be able to see the income statement that is submitted to HMRC, but you will also be able to see the detailed profit and loss, which will not form part of the statutory accounts.

Alongside the profit and loss statement, the balance sheet, which also forms part of your company accounts, is also a highly important financial statement to understand. Simply stated, the balance sheet is a snapshot of the company’s assets and liabilities at a specific point in time. But, don’t worry, we have an article that covers how to create a balance sheet!