As we know, HMRC has recently made some major updates to the research and development claim schemes for corporation tax, which applies to accounting periods starting on the 1st April 2024 onwards. Previously, there were two separate research and development schemes – one for SME’s, which offered a higher return rate due to the nature of their business, and one for larger companies, which was a bit more complex and offered a lower return rate. Now, HMRC has abolished these two schemes and created something called the ‘Merged RDEC Scheme’ and the ‘ERIS Scheme’. Before we discuss how to file under these schemes, let’s dive a little into what they are and who can claim each one.

What is the merged RDEC scheme?

The merged RDEC scheme is a research and development claim which has replaced the previous RDEC scheme, which was just for larger companies. While this new scheme is very similar to the previous one, there are some key differences, one of which is the corporation tax rate used. Previously, just the 25% main corporation tax rate was used, however, now, with the introduction of the small profits rate, this is also taken into account when making the claim.

Another thing to note with this RDEC scheme is that the tax credit itself is considered as trading income, thus it is liable to be charged corporation tax on. This is different to the SME R&D scheme and the ERIS scheme, as these tax credits are considered as below the line (not chargeable).

Who can claim under this scheme?

Essentially, anyone can make a claim under the merged RDEC scheme, as long as they are a company that is trading, are chargeable to corporation tax, and have a project that meets the definition of R&D. There are certain companies that must file under this scheme, rather than the ERIS scheme, which are:

- Profit making SME companies

- SME's who are claiming for work subcontracted to them

- SME's who received State Aid for the project

- SME's who are claiming for subsidised costs

- Large companies

If this does not apply to your company, then you can claim under the ERIS scheme instead. To find out more about merged RDEC, please feel free to read our article ‘What is the Merged RDEC Scheme and how does it work?’ on our EDF Knowledge Base.

What is the ERIS Scheme?

The Enhanced Research and Development Intensive Support Scheme, more commonly known as ERIS, is a tax relief scheme where companies who are heavily involved in investments toward research and development can benefit from an increased trading loss and even qualify for a tax pay-out.

Under this scheme, you can claim enhanced expenditure and a tax credit pay out. The enhanced expenditure rate for this scheme is 86% - so you receive an additional 86% of your total expenses on top of the 100% already being claimed as an expense. Furthermore, you also will receive a tax credit pay out, which will be at the R&D intensive rate of 14.5%. This means that you claim back 14.5% of either your company’s trading loss or surrenderable loss (depending on which is lesser), as a credit owed to the company. Depending on which losses are lesser, you sometimes can even carry forward some of your losses on top of the claim itself.

Who can claim this now?

Only pre-R&D loss making companies can claim under the ERIS scheme – meaning that the company must have been loss making before any enhancements from R&D were added. If the company was profit making then it must claim under the Merged RDEC scheme instead.

Not only this, but you must also be considered as an R&D intensive company, according to the conditions set out by HMRC. A company claiming under the ERIS scheme must have incurred relevant/qualifying R&D expenditure which was at least 30% of the company’s total expenditure for that accounting period. It is important to note that if the company has any connected or associated companies, then the relevant R&D expenditure must be at least 30% of the total expenditure of all these companies.

It is also worth mentioning that previously, in the old SME R&D Scheme, there was the option to file as an R&D intensive company, however, in order to qualify for this your total relevant/qualifying R&D expenditure needed to be at least 40% of the company’s total expenditure instead. So, it is important to double check the accounting period that you are filing for, before making your claim, as even if your period started on the 1st March 2024, then the company’s expenditure would still need to be 40%, not 30%.

For more on this scheme, please feel free to read our article 'The Enhanced R&D Intensive Scheme (ERIS) Explained'.

How to submit a claim under the merged RDEC scheme:

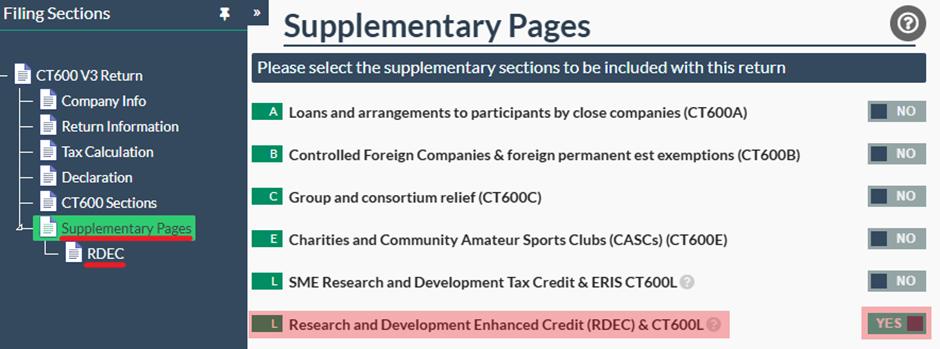

To make an R&D claim under the merged RDEC scheme, you first need to add the CT600L form. To find this, please open the CT600 Return template, go to the ‘Supplementary Pages’ tab, and switch box L (the last box) to Yes.

You should then be able to see the ‘RDEC’ tab on the left-hand side – click on this to open the form that you need to complete for this claim.

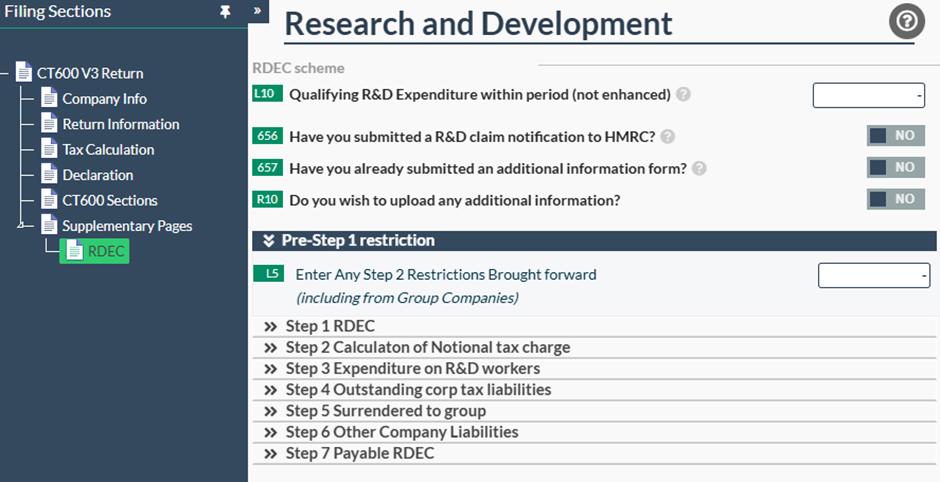

Please enter the total qualifying R&D expenditure into box L10 – please ensure that you also include this amount within the total expenses for the period in box E1 on the Tax Calculation page as well. Boxes 656 and 657 are forms that must be submitted directly through HMRC’s website first, before submitting the claim, but it is important to note that box 656 is only required if it is your first time submitting an R&D claim, or the first time in three years, whereas box 657 is required every year.

Once completed, you can then move on to the claim itself. First, you need to complete the relevant boxes in ‘Pre-Step 1’ (if applicable) and ‘Step 1’. If at this stage, there is still corporation tax due, please stop your claim here and do not complete any further steps. You can check whether there is corporation tax due by clicking on the ‘Tax Calculation’ page and checking the figure there. This is the same after Step 2 as well, as you will need to check if there is any RDEC remaining before continuing to step 3.

If there is RDEC remaining after this, then please continue to work through the remaining steps, only completing the applicable boxes. The claim will be offset against anything that is due, however, at the end, any of your remaining payable RDEC claim will be showing within step 7.

How to submit a claim under the ERIS scheme:

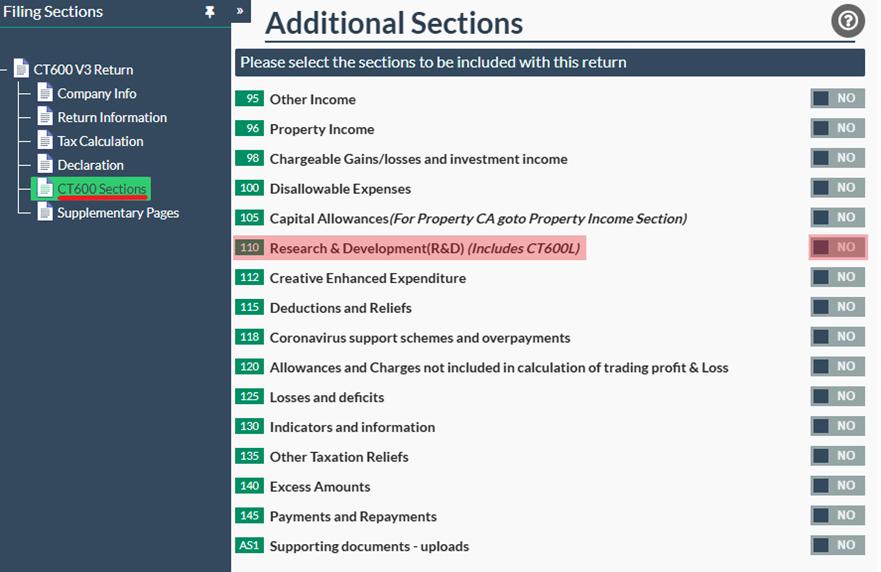

If you are looking to make an R&D claim under the ERIS scheme, then there is a slightly different procedure for this. To get started, you need to open the CT600 return template, go to the CT600 Sections tab and switch box 110 to Yes.

You should then be able to see a tab to the left which says ‘R&D Expenditure’ - please click on this to open the page. Here is where you need to enter all of the relevant information for your R&D claim.

Let's break down the boxes for you below:

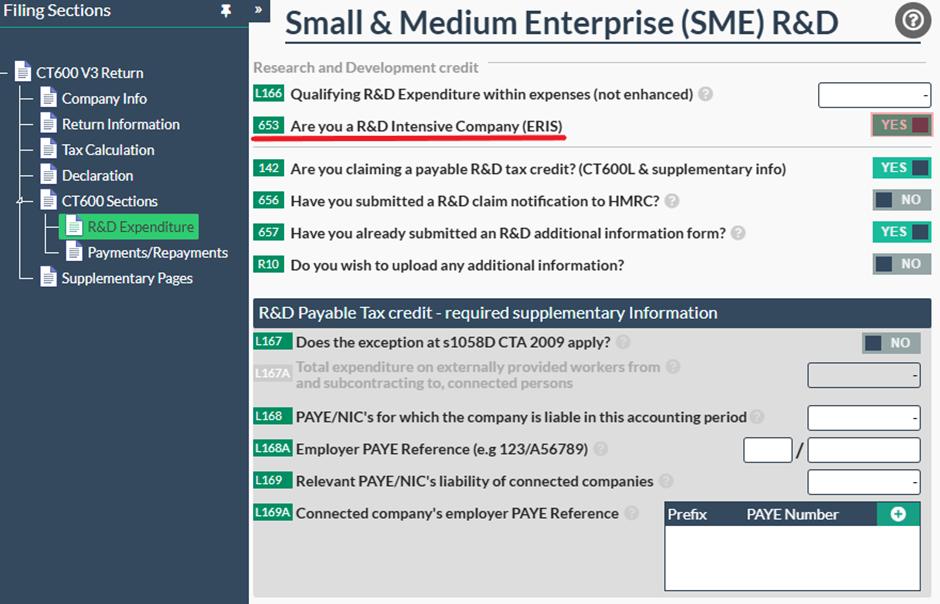

- L166 - Please enter all of the relevant qualifying R&D expenditure in this box. This is the same as box 659 and it will auto-populate this for you.

- Box 653 - Please switch this box to Yes in order for the correct rates to be used. This must always be switched to Yes in order to make an ERIS claim.

- Box 142 - Please always switch this box to Yes in order to claim the repayment from HMRC. This must be switched on for the tax credit claim to be correctly calculated and populated in the form.

- Box 656 - If this is your first time making an R&D claim, or the first time in 3 years, then this must be switched to Yes. You also need to ensure that you complete this form on HMRC’s website first, before submitting the claim.

- Box 657 - Before submitting an R&D claim, you must also always complete an additional information form, and this must be submitted directly through HMRC’s website first, as well.

- Box L168 - Please enter the total amount the company spent on PAYE/NICs in the period. If this is completed, please also complete box L168A.

It is important to remember that you must also enter the total income and expenses (including the qualifying R&D expenditure) into boxes 145 and E1 respectively, in order for the correct R&D claim to be calculated.

To summarise...

Now that we have gone into detail on what the merged RDEC and ERIS schemes are and who can file them, let’s recap some of the key things to remember when submitting the claims:

- You must claim under the merged RDEC scheme if you are profit making, even if you are an SME.

- Only loss making SME's whose qualifying expenditure was 30% of their total expenses, can claim under the ERIS scheme.

- You need to enter the total expenses, including the qualifying R&D expenditure, into box E1 on the Tax Calculation page, as well as in the CT600L form (box L166 for ERIS or box L10 for RDEC).

- You cannot claim under both the merged RDEC scheme and the ERIS scheme - you must pick one.

Now that you understand the basics of each scheme and how to claim them through our software, just head over to our website Easy Digital Filing to create your account and get started today!