Every year, whether you are a person or own a company, you are typically required to complete a tax return and then pay the amount of tax you owe to HMRC. Sometimes, a company may overpay their corporation tax and require a repayment, which is likely when carrying back losses or when forgetting to include any deductions, allowances, or tax relief schemes in your corporation tax return for the period.

So, what is a Tax Rebate?

To put it simply, a tax rebate is a refund of tax which is owed to the taxpayer or company by HMRC when they have paid more tax than they owe. You can also receive payments from HMRC if you have claimed tax credits from one of the tax relief schemes and it has created a loss for your company.

1. Trading Losses

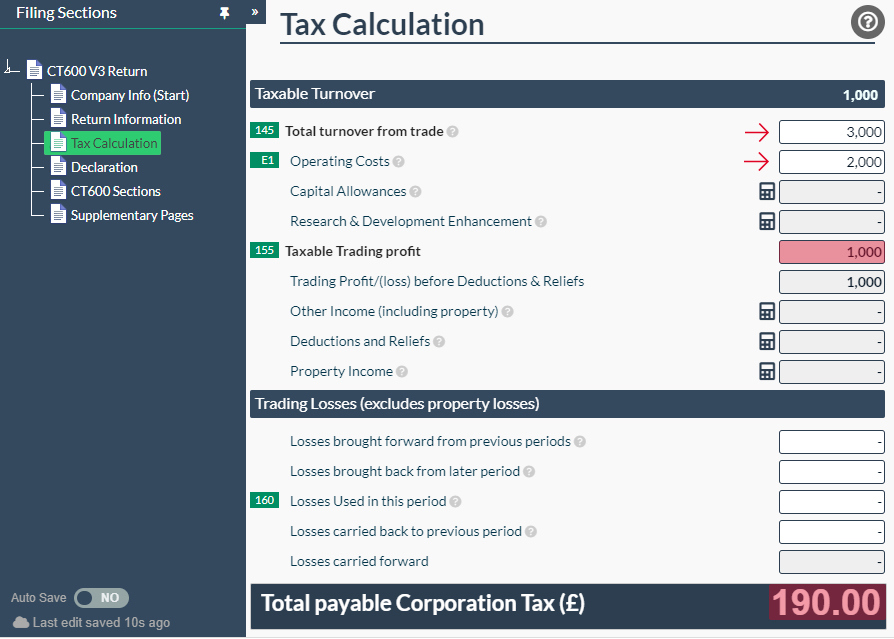

In your CT600 (corporation tax) return, you can carry back any losses that your company made in the previous period to offset the amount of corporation tax which was due.For example, if you had £3,000 of turnover and £2,000 of operating costs for the accounting period covering 2021/2022, then you would have made a profit of £1,000. As the tax rate for micro companies during that period was 19%, the corporation tax you would have been required to pay was £190.

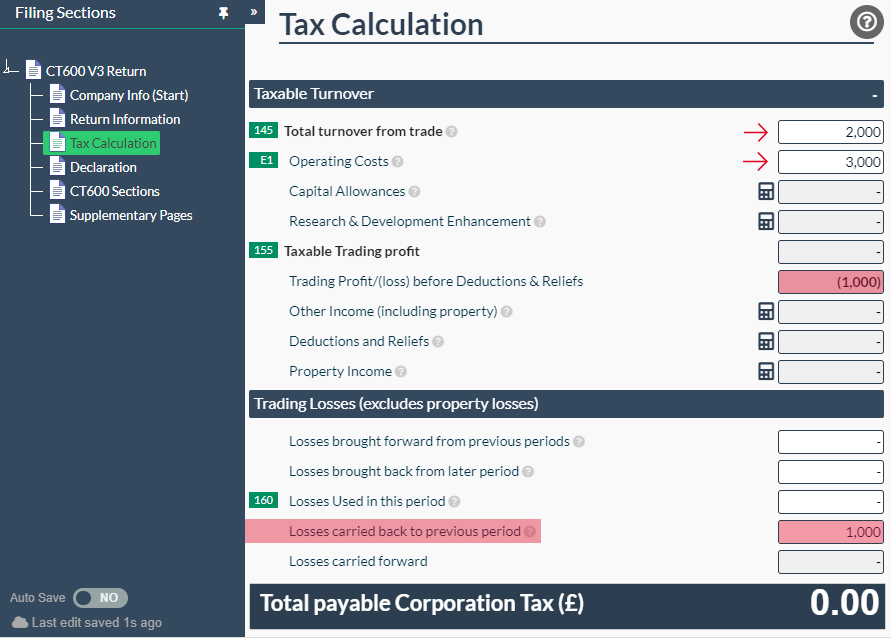

However, if you then have £2,000 of turnover from trade, and £3,000 of operating costs in the accounting period covering 2022/2023, then you would have had a loss of £1,000, meaning there would be no corporation tax to pay.

You could actually carry back your losses from 2022/2023 to 2021/2022 and use them in that period to offset your taxable income and reduce the corporation tax due. To carry back losses, you will need to enter the amount of losses you wish to carry forward in section 160, in the box 'Losses carried back to previous period'.

After filing the 2021/2022 corporation tax return, your company would have been required to pay £190 of corporation tax, however, after carrying back the losses of £1,000, the tax due would be £0:

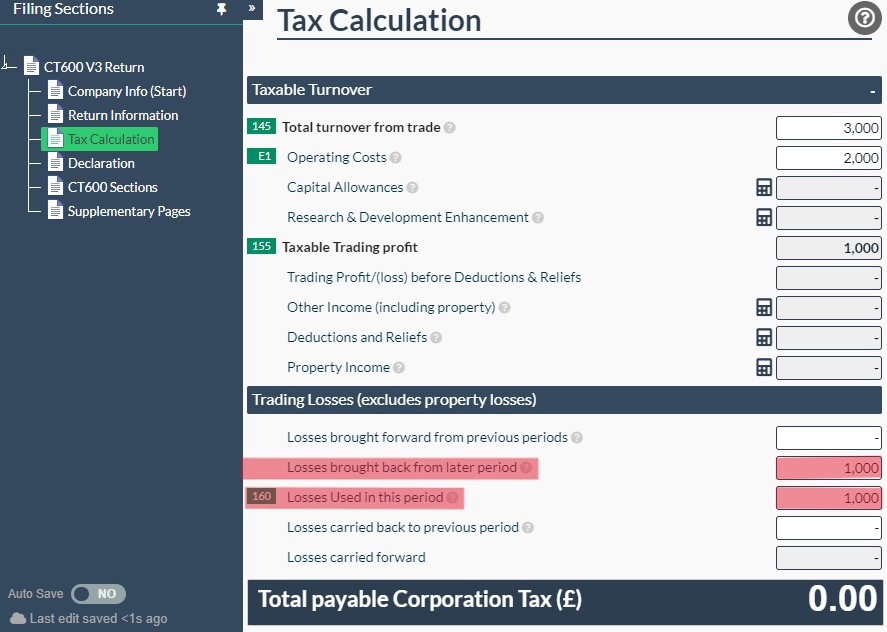

You would need to submit an amendment of your CT600 return for the accounting period covering 2021/2022 to reflect this change and reduce the corporation tax due to £0. In your amended filing, you would need to enter the amount of losses carried back to the accounting period (which in this case would be £1,000) into the box 'Losses brought back from later period', and then in order to use them in that period to offset the taxable income, you would need to enter that same amount in box 'Losses Used in this Period'.

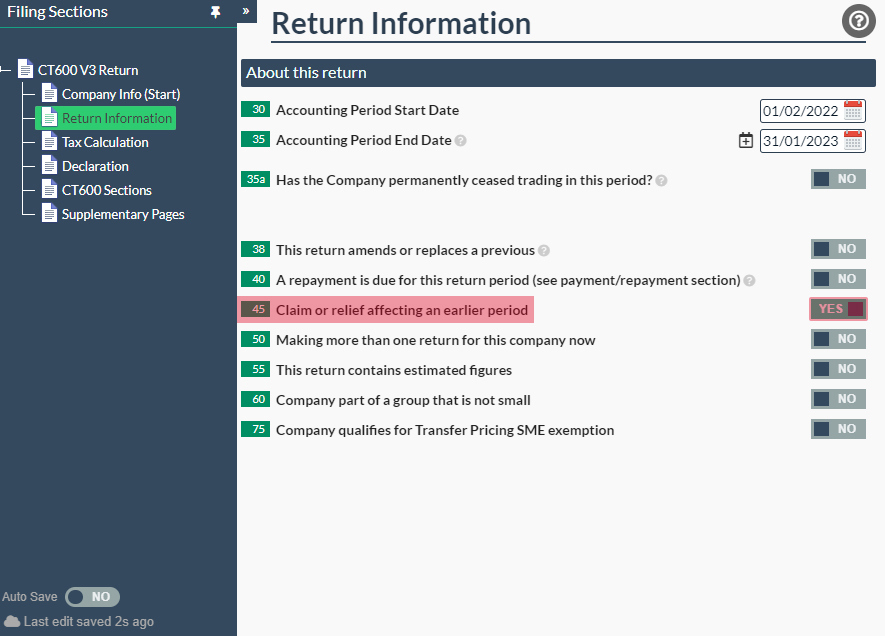

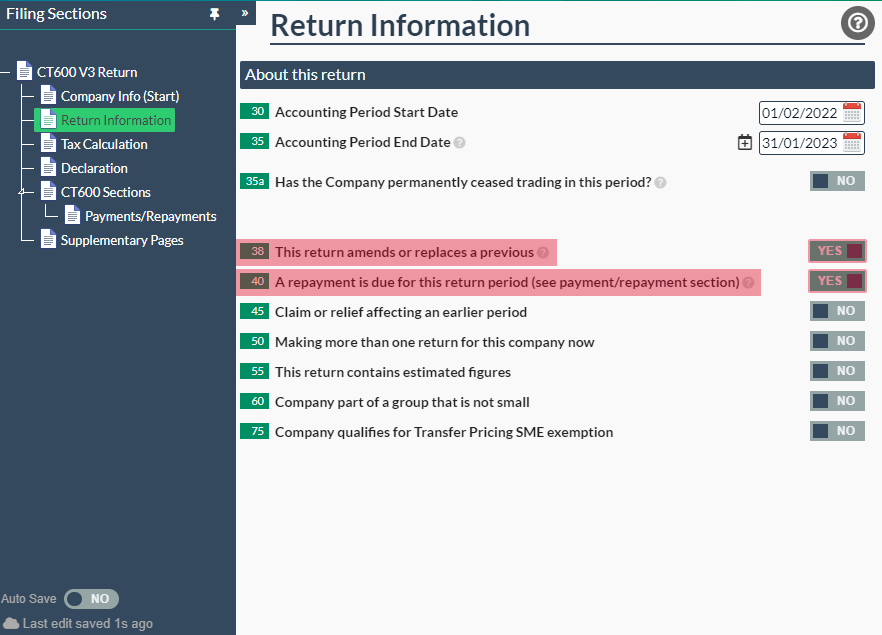

This would mean that you are owed a repayment of £190 by HMRC. Please remember that if you are submitting an amendment, you will need to switch box 38 to Yes on the Return Information page of your CT600 return.

When carrying back losses, it is important to note that you can only carry back losses 1 year. Additionally, you can only file electronic amendments of your returns to HMRC up to two years after the end of the accounting period.

2. Allowances

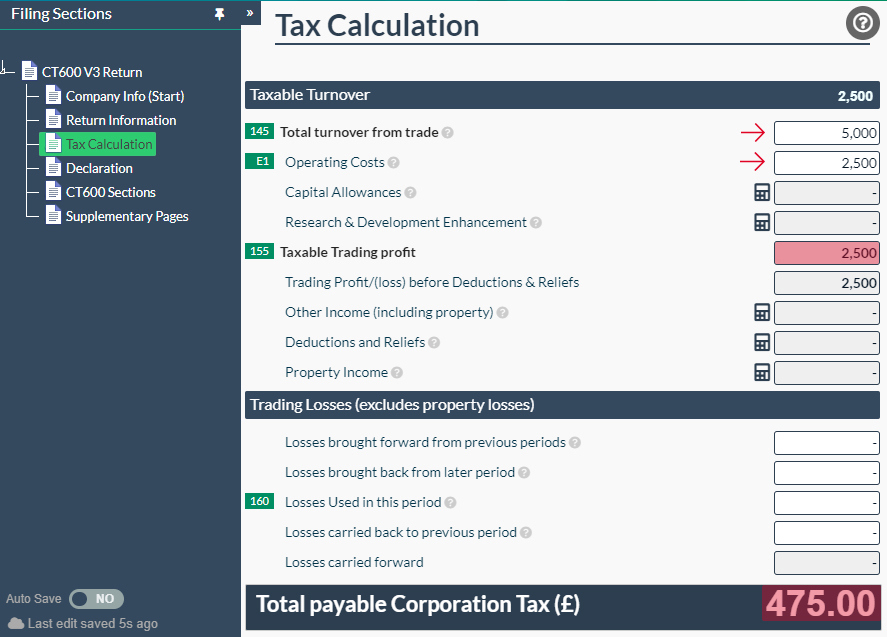

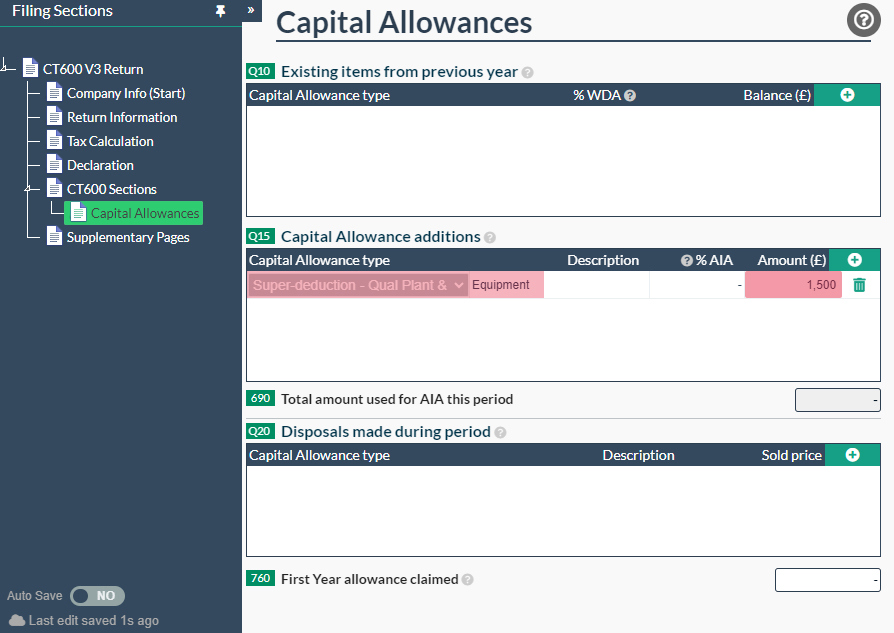

If you have forgotten to claim capital allowances, or deductions and reliefs, etc., which would reduce the amount of tax you were due to pay, then you can file an amendment of your CT600 return to HMRC and request a repayment. Here is an example of a tax reduction from claiming capital allowances.If your company had originally made a profit of £2,500, you would have had a tax payable amount of £475.

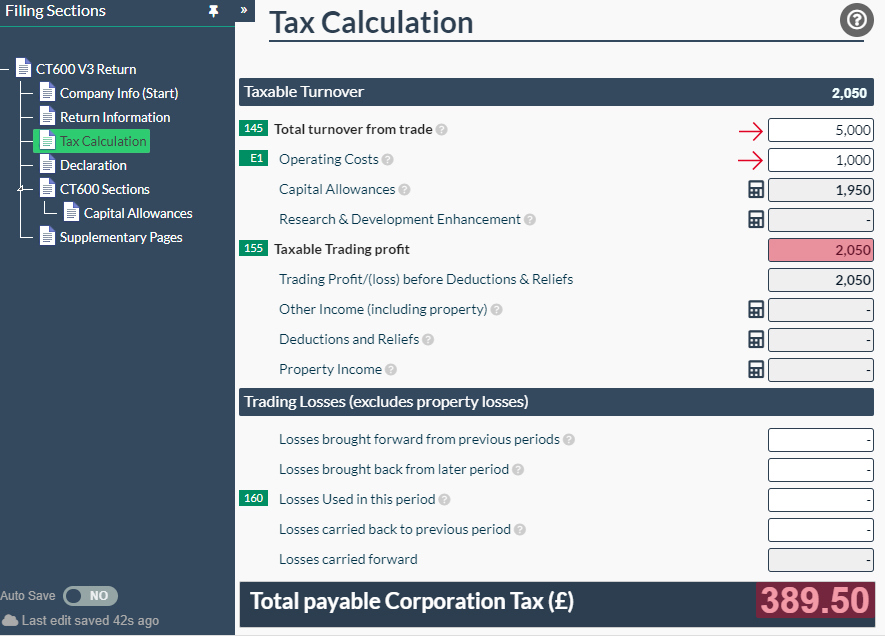

If your company had a total turnover from trade of £5,000 and total operating expenses of £2,500, then the taxable profit would have been £2,500, meaning that the corporation tax due to pay would be £475.

However, if you had spent £1,500 on equipment for your company which is to be used for periods longer than one year, it could be considered an asset and you could claim a capital allowance on it instead of claiming it as an expense. For this example, we will claim a super deduction, which is claimed on new and unused purchases and is at a rate of 130% (meaning that you can claim 130% of the total cost as an expense).

If the original cost of the asset was £1,500, and you claim a super deduction capital allowance on this item, this means that the new cost of the item is £1,950 (which is then deducted from the total taxable turnover).

This means that the taxable trading profit will be reduced by £1,950 and, in turn, reduces the amount of corporation tax due to pay from £475 to £389.50.

Unfortunately for small businesses, the super allowance ended as of April 2023, however depending on your tax year end you may still be able to benefit from this allowance.

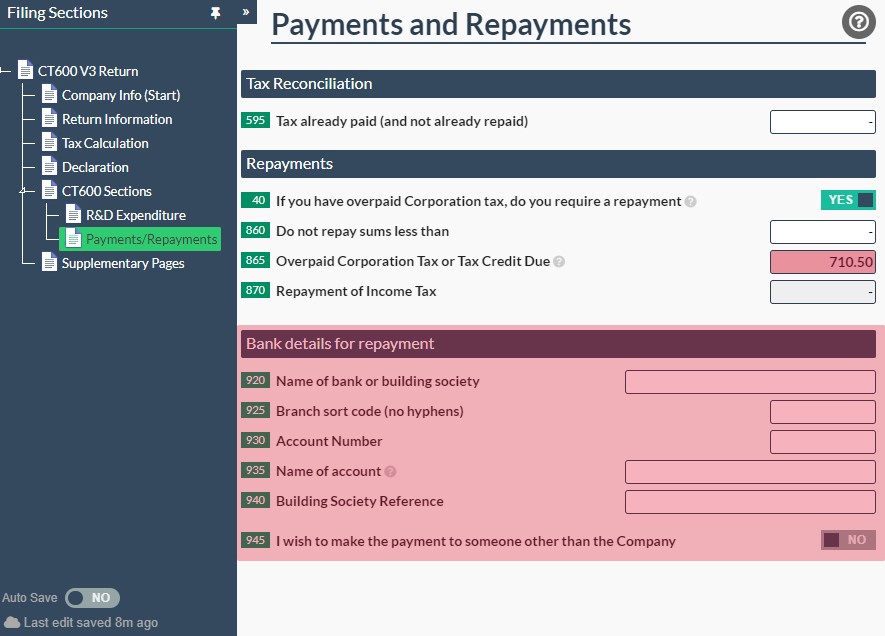

This would mean that you would be due a repayment of £85.50. This may not seem like a lot, but when you have capital allowances worth thousands of pounds, the difference adds up and it might worth filing an amendment and claiming a repayment.

3. R&D claims

You may also be due a repayment if you have had qualifying R&D expenditure during the period, meaning that a portion of your company’s expenditure was put towards research and development. Depending on whether your company is profit-making or loss-making, you may either be due a repayment, or your corporation tax due will simply be reduced.If your company was profit-making before and after adding the R&D enhanced expenditure, then the corporation tax that your company is due to pay will be reduced. However, if your company was profit-making before the R&D enhanced expenditure is added, but then it becomes loss-making once this is added, then the company's corporation tax liability will be reduced to £0 and they can claim the amount of tax credits due as a payment instead.

If your company was loss-making after adding the R&D enhanced expenditure, then you will be able to claim a payment of tax credits due. However, please note that the criteria for what qualifies as R&D expenditure is very specific and it requires a lot of supporting documents and evidence to be sent to HMRC before you can claim against it. Here is more information about who can claim SME R&D relief.

Additionally, you can find more information on how to claim an R&D tax credit in our article, How To File a R&D (Research and Development) Tax Credit claim.

So how do I get a repayment?

In order to get a repayment of corporation tax, you will need to notify HMRC that you are making a claim, which you can do directly through your tax return by switching box 40 (a repayment is due for this return period) to ‘Yes’ on the ‘Return Information’ page. You will then need to switch box 145 (Payments and Repayments) to ‘Yes’ on the CT600 sections page, and a new tab will appear. Click on this tab and it will open a page where you will need to enter your bank details (in boxes 920-945).You do not need to enter the amount of tax you are due to be repaid in box 595 as HMRC will automatically calculate this amount and will be aware that you are claiming a tax rebate. Alternatively, for R&D tax credit claims, our software will automatically calculate the figure which is due to be paid to you and it will appear in box 865.

Furthermore, it is important to note that if you are claiming a tax rebate on an earlier accounting period, you will need to switch box 45 to ‘Yes’ on the ‘Return Information’ page. For example, this would inform HMRC that you are claiming a tax repayment from the accounting period of 2021/2022, when submitting your tax return for the accounting period of 2022/2023.

Alternatively, if you are filing an amendment for the accounting period, you would need to switch box 38 to ‘Yes’, which notifies HMRC that it is an amendment to replace the previous filing. For example, if you were claiming a capital allowance that you had forgotten to add to your previous return, then you would need to file an amendment and claim a repayment at the same time. If this is the case, you would need to switch box 38 and box 40 to ‘Yes’.

Hopefully after reading this article, you have a better understanding of what tax rebates are and how to claim them when filing through Easy Digital Filing!