What happens if you've made a mistake in your Company CT600 Tax Return? Perhaps you have realised that you need to update the figures in the full accounts (profit and loss and balance sheet) that are attached to the CT600 Return. Or maybe the figures within the CT600 Return need to be amended. Whatever it may be, submitting an amended CT600 return can be straightforward!

Let’s see how it's done.

How long do I have to make the amendments?

An amended CT600 Return can be filed digitally within 12 months of the filing deadline. This means that you have 2 years to file any necessary amendments from the end of the accounting period.

For example, let us say that Company ABC Ltd with an accounting period of 1-January-2021 to 31-December-2022, has until 31-December-2024 to file amended CT600 Returns. This is 2 years to file from the end of the accounting period. The filing deadline for the original submission is 12 months after the end of the accounting period, which is 31-December-2023.

If you have surpassed the 2 year filing deadline with HMRC, you will have to post the filing to HMRC's postal address, as online/digital submission will be instantly rejected. You can print and download all the relevant filings from our software and post it to the following address:

Corporation Tax Services

HM Revenue and Customs

BX9 1AX

United Kingdom

Please remember to print and post the micro or small IXBRL tagged accounts, the CT600 Computations and the CT600 Form. It is also important to note the company UTR (unique tax reference) number on any documents you post to HMRC.

How can I get started?

If you need to make any changes to the micro accounts or small accounts, please open up the filing and select the orange button 'unlock and amend'. A small box will pop up confirming if you wish to continue to unlock and amend the filing; please select YES. After you have made the relevant changes, set the accounts back to 'ready to file' (green button).

Please open the accompanying CT600 Return and select 'unlock and amend'. You can then proceed with making changes where applicable within the Company Tax Return.

You will also need to select 'Return Information' tab and switch box 38 to YES. This confirms that this return will amend or replace the previous CT600 Return.

You can then set the CT600 back to 'ready to file' and click on the flashing red arrow under the 'submit/result' column to submit your amended CT600 Return. That's it!

I do not wish to change accounts - just the CT600

If you do not need to make any changes to the account and you are only looking to make changes in the CT600 Return, that is fine too. Please keep the accounts as they are, you will not need to 'unlock and amend' the account filing. You can 'unlock and amend' the CT600 Return and make any necessary changes as mentioned above.

First year of filing

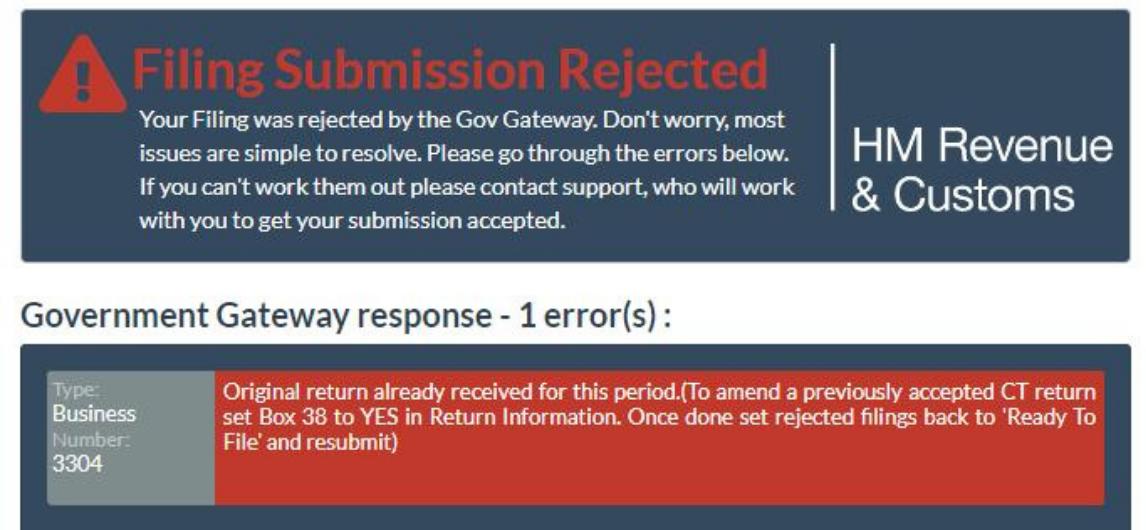

For companies that intend to file amended CT600 Returns for their first period, the procedure is a little different. You may face a rejection/error message upon submission of the amended Company Tax Return despite having switches on box 38 to YES. The error message will state, 'original return already received for the period'.

If this is the case, you will have to contact HMRC to unlog your first submissions from the system. HMRC will be able to unlog your previously submitted Tax Return easily by phone and HMRC's Corporation Tax enquires can be accessed here. After HMRC has removed your original submission/s from the system, you will be able to file your CT600 Return as a new return.

After you have unlocked and amended the necessary data relevant to HMRC, you will be able to file as a new CT600 return. Please ensure that box 38 is switched to No if you have previously tried to file as an amended CT600 return. As the original return has been unlogged this will no longer be an amendment and will be counted as a first submission. Occasionally, the unlogging process can take 24 hours before you can submit. If you have any difficulties filing, please do not hesitate to contact us; our support team will be happy to assist you through this.

Companies House Amendment

Companies House currently only expect the balance sheet (abridged accounts) to be submitted. Therefore, if you have made any changes to the balance sheet within your micro or small account, it would be best to file an amendment with Companies House too. This is to ensure that the company's financials at both HMRC and Companies House are up-to-date and accurate.

To see how you can submit amended Companies House accounts, please read the article here.

Do I have to pay extra for filing amendments?

Absolutely not! Amended filings are part of the package prices listed on our website. This mean that if you have already submitted to HMRC or Companies House through our software and you wish to file amendments, this can be done easily at no extra cost.

Please do not hesitate to contact a member of our support team if you have any questions or require any assistance in submitting amended filings.