If your company carries out research & development, you may have heard the term ‘ERIS’ a lot over the last few months, but what exactly is it? The Enhanced Research and Development Intensive Support scheme, more commonly known as ERIS, is a tax relief scheme where companies who are heavily involved in investments toward research and development can benefit from an increased trading loss and even qualify for a tax pay-out. This scheme was released alongside the new merged RDEC scheme, which you can read more about in ‘What is the Merged RDEC Scheme and how does it work?’.

ERIS was introduced for companies whose accounting period starts on or after the 1st April 2024, much like the merged RDEC scheme. It is very similar to the current SME R&D intensive scheme, as it has the same enhanced expenditure rate and tax credit claim rate, however, there are some key differences.

Who can claim ERIS?

A key difference in the ERIS scheme compared to the previous SME R&D intensive scheme, is that you can only claim this type of tax relief if you are a loss-making SME, whereas previously anyone that met the 'intensity conditions' could claim, no matter if they were profit or loss making pre R&D.

An SME is only considered as loss-making if the company had made a trading loss before any of the research and development enhancements are added from this scheme. So, if you are not loss-making before you make this claim, then you are not eligible, however, you can however, claim under the merged RDEC scheme instead.

Furthermore, just as with the last scheme, you must meet the conditions of being an intensive company to be able to make this claim. A company must be claiming for an accounting period that starts on or after 1st April 2024, and its relevant/qualifying R&D expenditure must be at least 30% of the company’s total expenditure for the period. If you have any connected or associated companies, then the relevant R&D expenditure must be 30% of the total expenditure of all those companies combined.

What are the enhanced expenditure and tax credits rates in this scheme?

Similarly to the previous SME R&D Intensive claim, you will be eligible to receive an enhanced expenditure and a tax credit pay out. The enhanced expenditure rate for this scheme is 86%, meaning that you will receive an additional 86% of the company’s qualifying R&D costs added to the company’s expenses. So instead of just claiming 100% of the qualifying costs, you get an extra 86% of this added to your total expenses, thus increasing the company’s trading loss.

Not only this, but you also get a tax credit pay-out, at the intensive rate of 14.5%. This means that you claim 14.5% of the company’s surrenderable losses as a credit which is paid back to you. Depending on which of your trading losses or surrenderable losses are greater, you may be able to claim a tax pay-out and still have losses to carry forward to the next accounting period.

Like the old SME R&D scheme, the surrenderable loss is the lesser of either 186% of your R&D spend or your actual trading loss.

This scheme is different to the merged RDEC scheme as the tax credit is not taxable for the company under ERIS, however, under the RDEC scheme, the credit is taxable.

It is important to note that you may not necessarily receive 14.5% of your losses as a claim since there is an additional restriction to the credit amount which is dependent on your company’s PAYE/NIC liabilities for the period. This is known as the PAYE cap and it means that you cannot claim a tax credit that is greater than 3 times the company’s PAYE/NIC spending for the period, plus £20,000. So, for example, if you spend £15,000 on PAYE/NIC’s in the period, then your tax credit cap is as follows: (3 x £15,000) + £20,000, which equals £65,000. This means that your credit claim cannot exceed this amount, even if 14.5% of your losses are greater than this amount. Also, if the company did not have any PAYE/NIC liabilities in the period, then their tax credit claim is automatically capped at £20,000.

If my company's accounting period falls across 1st April 2024, what happens then?

Unlike the previous SME R&D scheme, there are no apportionments to be made based on accounting periods when it comes to the ERIS scheme. This means that you can only claim under the ERIS scheme for accounting periods that start on or after the 1st April 2024. So, if your period started on the 1st March 2024, you can still claim under the previous SME R&D tax credit scheme instead. This applies to both intensive and non-intensive R&D companies as you would need to claim under the previous SME R&D tax relief scheme, (rather than the previous RDEC scheme). Then for any subsequent periods you would need to switch to either ERIS or the merged RDEC, depending on your company’s status.

How to claim ERIS through our software:

We offer dual functionality for submitting claims under both the merged RDEC scheme and the ERIS scheme through our software. We will break down the steps on how to claim for the ERIS scheme below:

Step 1:

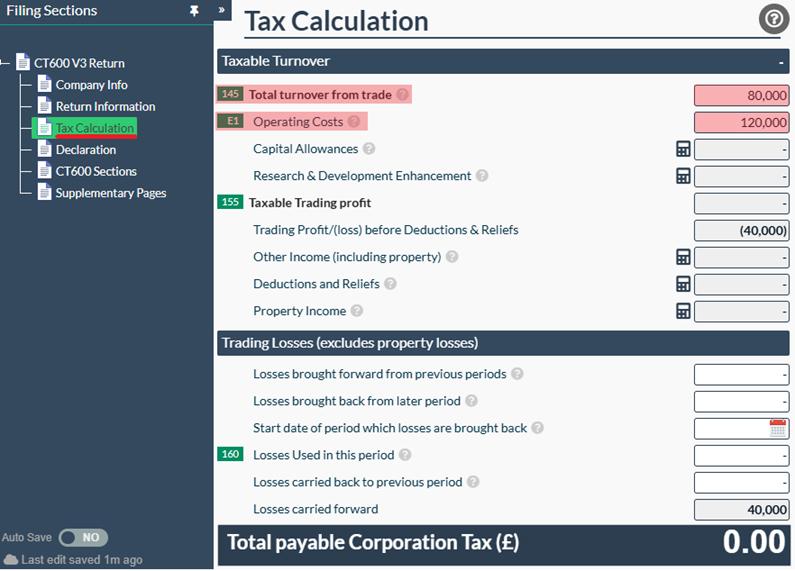

To start, you will need to open the CT600 return template and head to the Tax Calculation page. Please then enter the total income and total expenses into boxes 145 and E1, respectively.

Step 2:

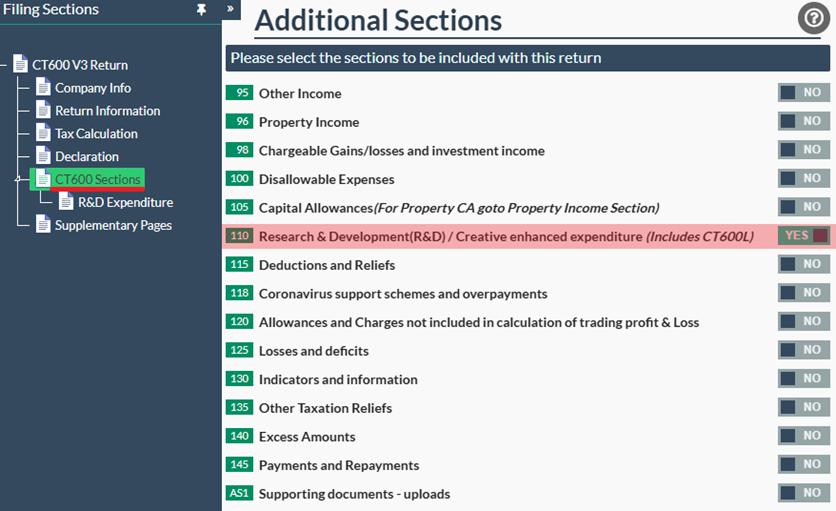

Once you have entered the company’s income and expenses, please head to the CT600 Sections tab and switch box 110 to Yes. This will create the Research and Development page.

Step 3:

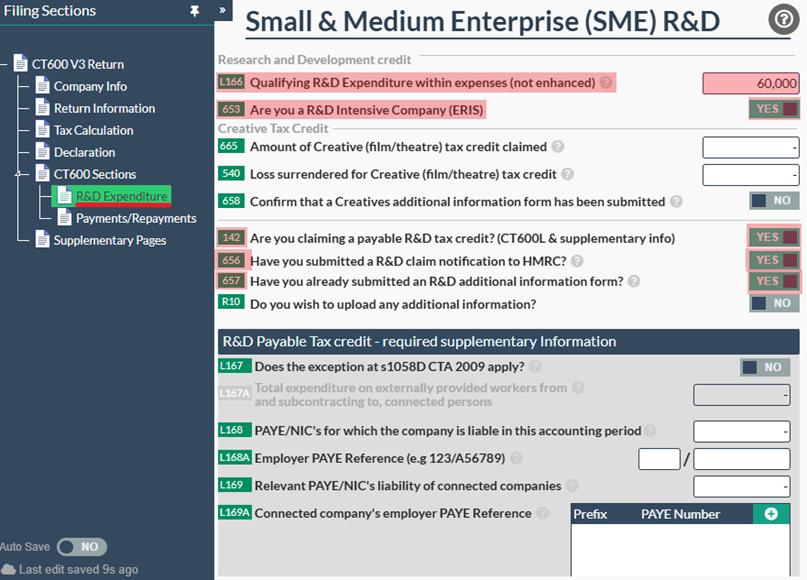

Once the page has been created, please click on the ‘R&D Expenditure’ tab. Here you will need to enter the total qualifying R&D expenses into box L166. As you are filing for an R&D intensive company, please also switch box 653 below to Yes.

Please also ensure that you complete the R&D claim notification form (box 656) if it is your first time filing an R&D claim, or first time in three years, and that you also complete the R&D additional information form (box 657) for each accounting period. These forms will need to be submitted directly through HMRC’s website before you submit the CT600 return itself.

You will also need to switch box 142 to Yes in order to claim the tax credit.

Step 4:

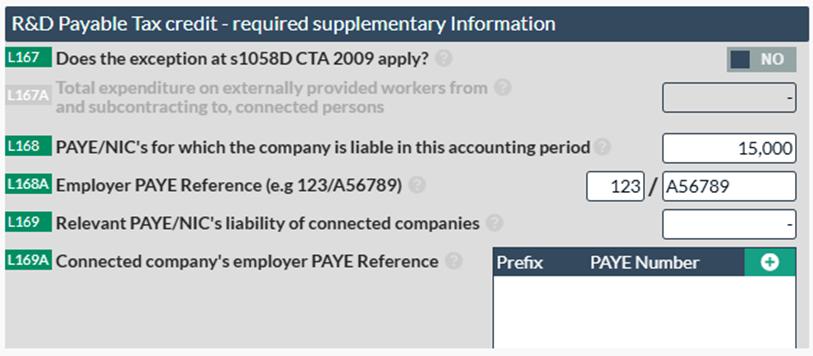

If the company has made any PAYE/NIC contributions in the period, then you will also need to enter this amount into box L168. Please ensure that you also complete box L168A by entering the employer's PAYE reference, as this is required if an entry is made in box L168.

Step 5:

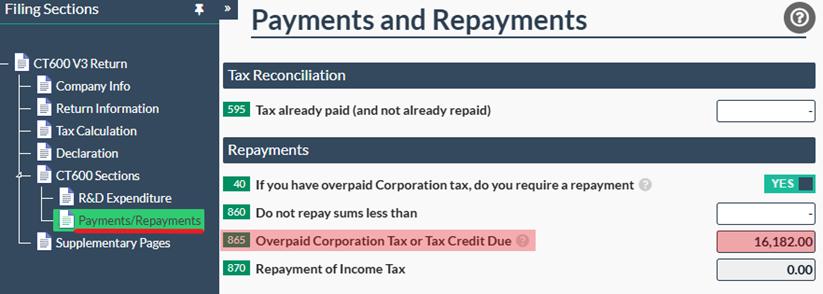

Once you have completed the R&D page, please click on the Payments and Repayments page to view your tax credit claim.

Our software will automatically calculate the tax credit claim for you, based on the entries made. You can view your tax credit in box 865 on this page.

And that’s it! After following these steps, you have now successfully completed an ERIS claim for your company.

Key points to remember:

Let’s recap some of the important points about the ERIS scheme:

1. Companies that meet the conditions to qualify as an R&D intensive company can claim under the ERIS scheme.

2. Only R&D intensive SME’s that were loss making prior to the enhanced expenditure being added, can claim under the ERIS scheme. If this does not apply, then you will need to claim under the new merged RDEC scheme instead.

3. The tax credit payment is not taxable under the ERIS scheme, which differs from the merged RDEC scheme, where it is taxed.

Hopefully after reading this article, you will have a better understanding of how the ERIS scheme works and how to file this claim through our software. For more on R&D claims in general, please feel free to read our article ‘

How to File a R&D (Research and Development) Tax Credit Claim’ in our Knowledge Base.

This article is information only and has been prepared for general guidance on matters of interest only, and does not constitute legal, accounting, tax, investment or other professional advice or services. You should not act upon the information contained in this article without obtaining specific professional or legal advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this article, and, to the extent permitted by law, Comdal Limited, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.