What is a qualifying donation?

There are requirements that must be fulfilled in order for a charitable donation to be considered ‘qualifying’ under UK tax law. A qualifying donation is a donation that is given to a charity that has been approved as a registered charity by HMRC. Money donated to these charities (and under some circumstance, gifts of assets) might count as a qualifying donations for tax purposes. However, there are requirements that must first be fulfilled in order for a donation to be considered ‘qualifying’ under tax regulations.

The following points must be met in order for a donation to be eligible for tax relief:

1. A registered charity or another HMRC-approved qualified organisation must receive the donation.

2. The gift must be given freely, without anticipating any reward or personal gain in return.

3. The charitable donation must be made with cash, a cheque or a bank transfer.

The donor may be able to claim tax relief on the qualifying donation, which lowers their overall tax expense once these requirements are met. As mentioned previously, donations of goods or services are not eligible for tax breaks under programs like Gift Aid, however there may be some exceptions.

The Gift Aid Scheme:

Gift Aid is a scheme which allows charities to claim 25p for every £1 provided from a taxpayer at no additional expense to the donator. This scheme is the most well-known tax benefit as the charities revenue is increased at no additional charge meaning the donation becomes more valuable.

The following requirements must be fulfilled by the donor in order for their donation to be eligible for Gift Aid:

• In order for the charity to claim their donation, the donor must be a taxpayer during the current tax year.

The main advantage of Gift Aid is that donors can increase the impact of their contributions at no extra costs for themselves, meanwhile giving organisations a big financial boost. For instance, if a person gives £100 to a charity, the charity may be able to claim an extra £25 from HMRC, bringing the total donation to £125.

Corporation Tax Relief and Corporate Donations:

In addition to individual taxpayer, businesses are also encouraged to donate to charities. This is because, contributions usually lower a company’s total corporation tax liability and therefore are tax deductible. The donation must be voluntary and made to a recognised charity, just like individual gifts.

The following types of donations are eligible for tax reduction for corporations:

• The most common type of donation is cash, which is also completely tax deductible for businesses.

• Businesses can occasionally give stock or equipment to charitable organisations. However, HMRC must agree on the valuation of the donated assets and these donations may also qualify for tax relief.

Qualifying Donations and Inheritance Tax:

Donations may also impact the amount of inheritance tax (IHT) a person must pay. If a person leaves a certain amount of money to a charity, then this figure will be deducted from their estate. This then lowers the amount of inheritance tax that is owed as the overall estate value decreases.

Additionally, the rate of inheritance tax on the remaining estate can be lowered from 40% to 36% if a donor donates at least 10% of their net estate to charity. This is because it promotes charitable giving which is a compelling choice for people looking to lower their IHT while also contributing to causes that are important to them.

Other Tax Reliefs for Charitable Donations:

Payroll Giving is another scheme that enables workers to make donations straight from their pay cheque. This is when the donation is taken out of the pre-tax income, (meaning the donation is subtracted from their gross income), and consequently the donor receives instant tax savings. There is also more tax relief available for taxpayers with higher tax rates. The difference between the basic rate and the higher rate tax on a charitable donation might be refunded to the higher-rate taxpayer.

Which Donations Are Ineligible?

Although the UK tax system does provide significant tax relief for donations, not all gifts are considered qualified. Important exclusions include of:

• Donations of products or services: Generally speaking, the Gift Aid program only offers tax breaks for money/cash donations.

• Donations with personal benefits: A donation may no longer be eligible for Gift Aid if the donor receives something of personal value in exchange (e.g. raffle tickets). This is because the donation must be made without the intent of any kind of compensation.

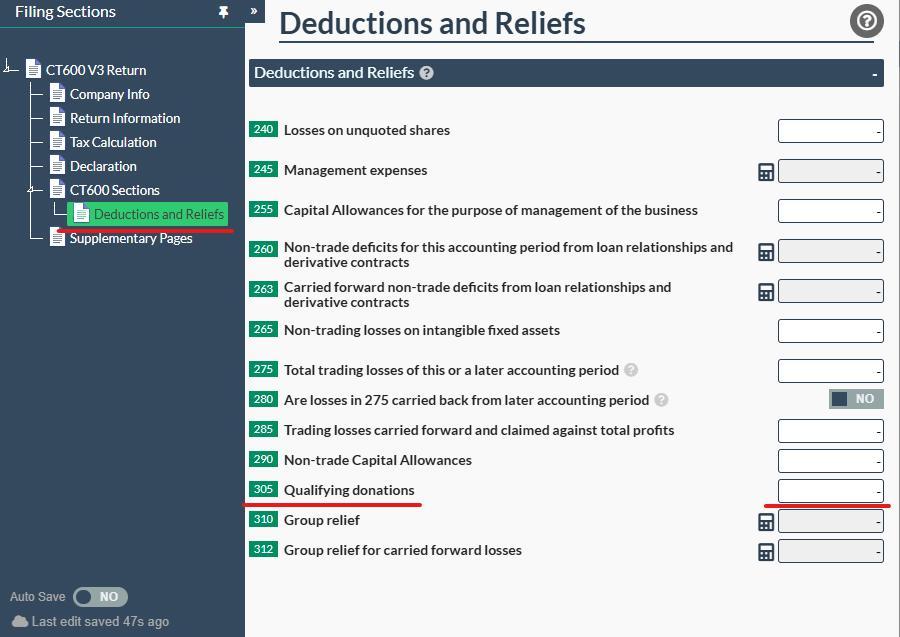

How to declare a company donation on a CT600:

When making charitable donations, your company can claim tax relief on the CT600 (Corporation Tax) Return - this is subject to the company making a profit. In the CT600's "Deductions and Reliefs" tab, you can claim tax reliefs for any company donations made by the firm as well as any land, property, or shares that have been given or sold.

You will be able to claim these qualifying donations using our corporation tax software. The first step is to change box 115 on the "CT600 sections" page of your CT600 template to "YES." You can then input the donations in box 305, "Qualifying Donations".

This will then reduce your taxable income, which will in turn reduce your corporation tax liability.

Conclusion:

In conclusion, the UK tax system offers numerous tax reliefs to eligible donations made to registered charities. Contributions to charities can lower a donor's overall tax obligations while supporting worthy causes in a number of ways, including payroll giving, corporation tax relief, inheritance tax relief, and gift aid. This therefore, promotes a culture of generosity and social responsibility by providing these tax benefits.