Charitable Donations and Corporation Tax

Can Limited Companies receive Donations?

If you have already or are going to incorporate a limited company in the UK, you might want to know whether your company can receive charitable donations.

In short, yes, limited Companies are able to receive charitable donations, although they are more widely received by organisations like company’s limited by guarantee or community interest companies (CICs). While limited companies are allowed to receive donations, the legal and tax treatment depends on the type of company and donation.

Tax Consequences of Donations Received

Donations received by limited companies are typically not exempt from tax, this is usually recorded as taxable income with the CT600. However, if you are receiving charitable donations as a registered charity then you will typically be able to receive this income exempt from tax.

Alternative Company Structures

There are different types of company structures that you may want to consider as an alternative to a limited company, if your company’s principal activities are charitable and the company’s main source of income are donations:

• Charitable Incorporated Organisations (CIOs) – Primarily, CIOs have a good company structure for receiving donations due to its tax relief, typically all donations income would be tax exempt. Additionally, CIOs still offer benefits of an incorporated structure.

• Community Interest Companies (CICs) – CICs are typically formed to invest in and purchase assets for their communities, so would a be an ideal structure for receiving charitable donations for these activities. CICs would be considered limited companies, limited by guarantee.

Claiming Tax relief on Charitable Donations

Limited companies can reduce their corporation tax liabilities by donating money to registered charities or Community Amateur Sports Clubs (CASCs). Other charitable donations include equipment and trading stock, as well as land and property. Typically, tax relief can be claimed by deducting the amount of charitable donations from the company’s profits.

As per HMRC guidelines, the following payments to charities of CASCs that aren’t tax deductible include the following:

• Loans made to charities that are expected to be repaid.

• Distributions of the company’s profit, such as dividends.

• Payments made on the condition that the charity will buy property for your company (or anyone connected to the company).

Company Received Benefits

Companies that donate to charity can sometimes receive certain benefits themselves directly from that charity, benefits could include tickets to events for example. These benefits however, must be below a certain threshold, illustrated in the table below:

| Donation Amount | Max Value of the Benefit |

| Up to £100 | 25% |

| £101 - £1,000 | £25 |

| £1,001 and over | 5% (up to max of £2,500) |

Any company or person related to the company donating to charity is able to receive benefits that meet these requirements.

Equipment

Limited companies can also donate equipment or sell ‘trading stock’ to charities in order to reduce their tax liabilities. Companies will be able to claim full capital allowances on the fixed asset equipment purchases as a way of tax relief.

It’s important to note that in order for equipment to qualify as a donation, the items will have to be purchased by the company and used first before donating.

Types of equipment that your company can donate include:

• Computers and printers

• Office furniture

• Vehicles

• Tools and Machinery

Trading stock can also be donated; these are items that a company makes to be sold. When this is donated the full purchase price of the items can be deducted from the company taxable profits.

Land and Property

Another way companies can pay less Corporation Tax is by selling land, property or shares from another company to charities. It’s important to note that a company is only able to donate shares from another company and not its own.

The sale of land or property to charities or CASC’s is typically exempt from capital gains, this is whether it’s donated for free or sold at a reduced price, hence lessening the amount of tax to pay.

How to claim tax relief on donations

There are multiple ways that your company can claim tax relief when donating to charity in the CT600 (Corporation Tax) Return. This will depend on the type of donation that you are looking to make.

Deductions and Reliefs

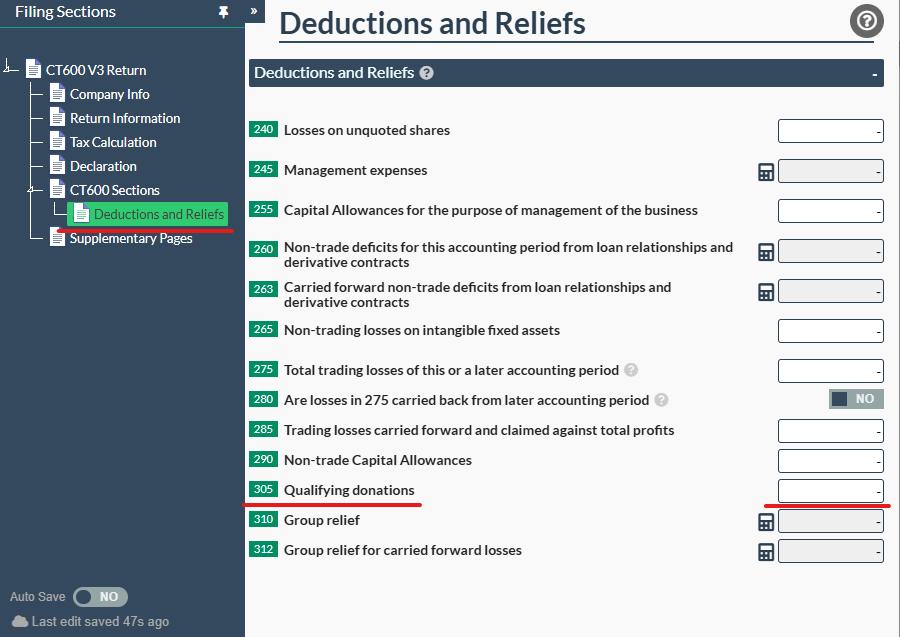

If the company has donated money or given/sold land, property or shares, you will be able to claim tax reliefs on this in the ‘Deductions and Reliefs’ section of the CT600.

Through our software, you will be able claim these qualifying donations. Firstly, you will need to switch box 115 to ‘YES’ in the ‘CT600 sections’ page of your CT600 template. This will open up the ‘Deductions and Reliefs’ page and you will be able to enter the donations in box 305: ‘Qualifying Donations’.

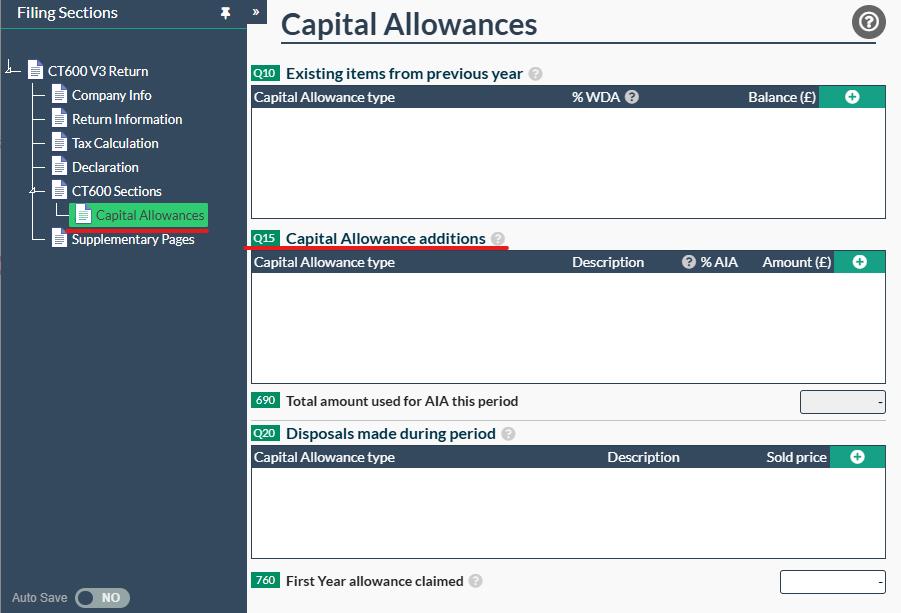

Capital Allowances

Additionally, companies will be able to claim Capital Allowances on any equipment that was purchased and then donated. In order to do this within our CT600 Return template, you will need to enter the amount of Capital Allowance additions claimed in section Q15 of the ‘Capital Allowances’ page. This page can be accessed by switching box 105 to ‘YES’ in the ‘CT600 sections’ page.

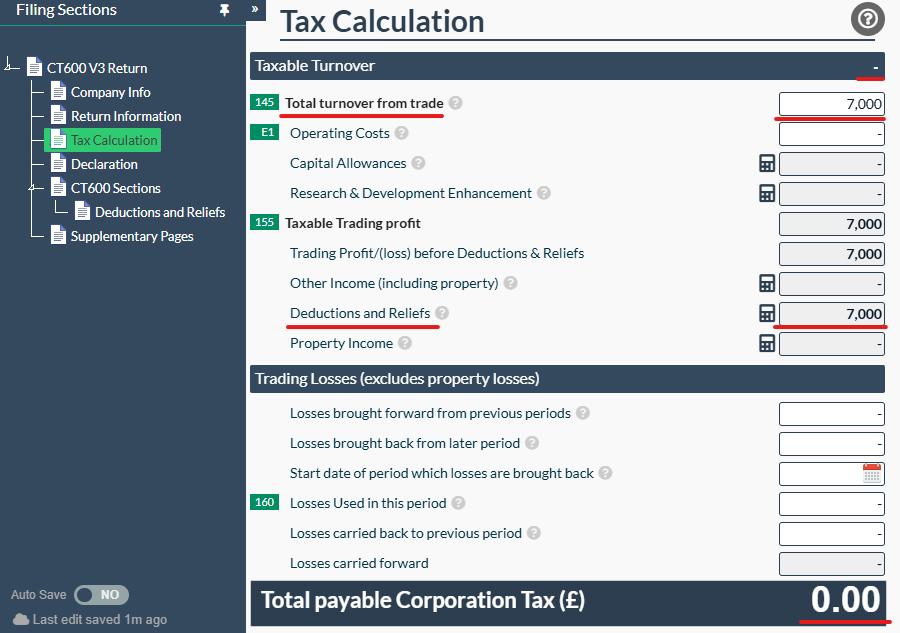

Donating more than your profit

Claiming tax relief on donations can not result in a trading loss. The maximum amount of donations you would be allowed to claim is the amount that reduces the taxable turnover to zero.

In addition, if the company donates more than the company’s profit, the excess donations cannot be carried forward or backwards to offset future taxable profits.

For example:

Let’s say your company has an overall business profit of £7,000 (before donations) and have made donations to charity of £10,000. The maximum amount of donations you can claim is £7,000 reducing the corporation tax liability to £0. However, the remaining £3,000 cannot be accounted for within the CT600 (as it would make the company loss making), it also cannot be carried forward to future periods or back to previous ones.

Main Takeaways

• Making donations as a limited company to charities of CASCs can help reduce your total corporation tax liabilities.

• There are many other items companies can donate to charities other than money, including equipment, stock and even land and property! Which can be used to offset taxable profits in different ways within the CT600

• It’s important to keep a detailed record of all of the donations made. This helps ensure the company can qualify for tax relief claims with HMRC.