What is deferred tax?

This may sound like a daunting term, especially if you are trying to file the returns yourself, but put simply, deferred tax is tax that is payable in the future. A deferred tax liability is known as the amount of tax that is payable in the future accounting periods, with regards to ‘taxable temporary differences’. Taxable temporary differences is the difference between the carrying amount (or original cost of the item minus any depreciation) which is reflected in the balance sheet (or statement of financial position), and its tax base, which is the amount that the asset (or liability) is officially valued for tax purposes only. Again, this may sound a bit confusing, but in simpler terms, taxable temporary differences is the difference between what the asset (or liability) is currently valued at (as shown on the balance sheet), compared to what the asset (or liability) is worth, when properly valued.

To summarise, deferred tax is tax that is potentially payable in the future if the asset or liability is sold, etc., for more than it is currently listed as (meaning that it is worth more than it is currently valued at). If your company has any deferred tax, it needs to be accounted for on both the income statement and balance sheet when completing your company accounts. It is important to note that deferred tax should not be included in the calculation for corporation tax – only in the accounts.

How do I account for deferred tax on my returns?

Through Easy Digital Filing, there are two different financial reporting standards that you can file under – one is FRS105, which is primarily for micro entities, and the other is FRS102, which is primarily for small entities.

The Financial Reporting Standard 105 does not allow for accounting for deferred tax, so this would not be able to be included, if you choose to file as a micro company. However, the Financial Reporting Standard 102 allows for deferred tax to be accounted for, so if this is required, then you will need to file under this Financial Reporting Standard instead.

You can file under FRS102 if you are small entity, or as a micro entity as well. While small entities are not able to file under FRS105, and are instead only required to submit under FRS102, micro entities have the option to file under either financial reporting standard – so it is up to them which one they wish to file under. So, for example, if a micro entity wanted to account for deferred tax in their company accounts, they would be able to file as a small company instead.

Below, we will explain how to include deferred tax in your accounts when filing through Easy Digital Filing.

Add the filing to your account:

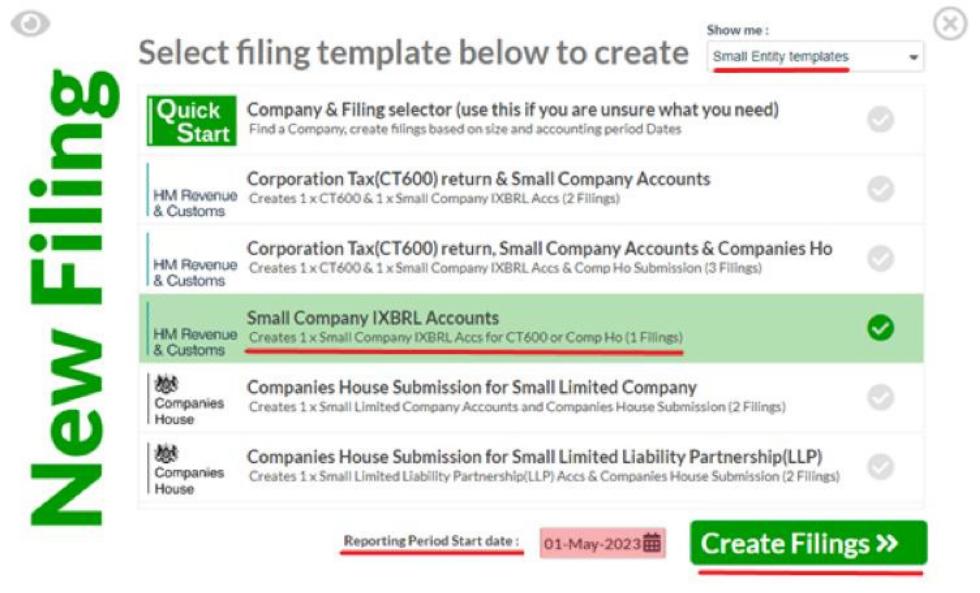

The first step is to add the correct templates to your account. You can do this by clicking on the blue ‘Add Filing’ button near the top left of your screen, once logged in to your account. Then, change the product filter near the top left of the ‘Add Filings’ box to show just the ‘Small Entity Templates’ (as this will make it easier to find the correct template). Your screen should look similar to the one in the picture below:

You can then select ‘Small Company IXBRL Accounts’ from the options shown, enter the start date of your company’s accounting period, and then click on the green ‘Create Filings’ button. You should now be able to see the Small Company IXBRL Accounts template under ‘Filings view’ within your account – click on the filing to open it.

Where to place deferred tax in the accounts:

As previously mentioned, deferred tax needs to be accounted for on both the income statement and balance sheet.

In this example, we will assume that a company has an asset that is worth more than it is valued. So, they have a piece of machinery which is listed as £33,350 on their balance sheet, but it has actually been valued at £45,500. If they are planning to sell this asset in the next accounting period, this will create a chargeable gain of £12,150, which they would be liable to pay corporation tax on. As the main rate for corporation tax is 25%, the total corporation tax that would be due is £3,037.5 (which is £12,150 x 25%) – this would then be considered as deferred tax.

In the income statement, this should be included in the ‘Taxation’ section in the ‘Tax Deferred’ box.

Within the taxation section of our templates, you just need to click on the box next to ‘Tax Deferred’, and you will be able to type in the figure – which, in this case, is £3,038.

Then, on the balance sheet, the deferred tax will need to be reflected in the creditors due section. The deferred tax can be placed either in the ‘Creditors Due within One Year’ or within the ‘Creditors Due after one year’ – it just depends on the type of company you are filing for, and whether the tax will be paid in the next year or longer than one year. In the creditors, you can place the figure either in the ‘Corporation Tax’ box, ‘Other Creditors’ box, or whichever you feel is most appropriate out of the options provided.

For this example, the company is expecting to sell the asset in the next accounting period, so I have included the deferred tax as ‘Other Creditors’ under the ‘Creditors Due within One Year’ section in the balance sheet. This figure could be included in the corporation tax section, however, in this case, we have just added it to ‘Other Creditors’ – it is up to you where you place the figure, as long as it is accounted for somewhere.

What about in the CT600 return?

The CT600 return, also known as the corporation tax return, should only include figures that relate to the accounting period that you are filing for – meaning that deferred tax should not be shown anywhere on the tax return.

For more information on how to complete the corporation tax return, please feel free to check out our article called ‘How To File a CT600 Online’ from our Knowledge Base.

Hopefully after reading this article, you can gain a better understanding of what deferred tax is and how to correctly account for it!