All companies that employ people through PAYE must also make employer contributions to their employees' national insurance and pension scheme. There are some restrictions based on age and wages, however, typically you need to make an employers contribution of at least 3% of your employees' qualifying earnings into their pension scheme, although you can make larger a employers contribution if your wish. It is best to double check which scheme the company is registered with, as the payable amount can vary. Let's take a deeper look into how the pension schemes work and how/when they are paid.

What are pensions and who pays them?

A pension is a type of payment plan and it's purpose is to provide income for when you retire. There are many different payment plans, such as workplace pensions, private pensions, or the state pension, and vary depending on where you work or whether you set one up.

Typically, as an employer must enrol your employees in a pension scheme if they are aged between 22 years old and the state pension age (which you can figure out using the gov.uk calculator), they must earn at least £10,000 a year, and normally work in the UK (meaning that they are based in the UK, even if you travel for work). An employer can choose to defer enrolling an employee into the pension scheme for up to 3 months after joining. However, an employees' qualifying earnings amount may differ depending on which scheme the company has, so it is best to check this first. Once confirmed, the employee must be enrolled into the pension scheme within 6 weeks after becoming eligible. As the employer it is your responsibility to ensure you enrol your employees on time

Within the scheme, as already mentioned, an an employer must pay at least 3% of their employees’ qualifying earnings. Under most schemes, the total qualifying earnings include their wages, bonuses and any commission paid, overtime pay, statutory sick pay, and statutory maternity/paternity/adoption pay. The employees contributions are taken from your employees pay each month and putting into their pension scheme along with the employers contribution. Between the employees and employers contribution a minimum of 8% of the qualifying earnings must be made each month. You must pay this amount by the date that has been agreed with your pension scheme provider, otherwise you may be fined if you do not pay the minimum contribution for each staff member on time.

How to manage your pension scheme:

As an employer, there is a little bit more to the pension scheme than just making the payments each month, so let’s go into a bit more detail on how to manage your employees’ pensions.

Re-enrolment:

Once you have your pension scheme set up and your employees enrolled, you might think you’re done – however, that’s not the case. Every three years after your first member of staff starts working for you, you must re-enrol them into the pension scheme. This is only the case if they had left the pension scheme more than 12 months before there re-enrolment date, and they are still in the pension scheme but pay less than the minimum contributions. If any employees had left the pension scheme 12 months or less before their next re-enrolment date, then you can choose to re-enrol them on the pre-existing date, or just wait until their next enrolment date in three years.

It is also important to note that you must inform the eligible employees that you have re-enrolled them into the pension scheme, and it must be done within 6 weeks after re-enrolment.

Re-declaration:

This goes hand in hand with re-enrolment, as every three years, after re-enrolling your staff members, you need to also re-complete a declaration of compliance to inform the pensions regulator that you have met your duties. You must complete this form every three years, no matter whether you re-enrolled any employees or not, as this is obligatory. If the form is not completed on time, then you may be fined.

Requests to join or leave:

Any employees can request to join the pension scheme if they desire, as long is meets the mandatory pension scheme requirements. For example, if there are any employees who are under 22 years of age, then they can voluntarily opt in to the pension scheme, even though it is not mandatory. In this case, you must check if they are eligible to be enrolled into your specific pension and they must be enrolled within 1 month after requesting, if applicable.

Additionally, your employees can also request to leave the pension scheme as well. In this case, you must also remove them from the pension scheme within one month of their request. Employees can also choose to leave the pension scheme within something called an ‘opt out window’. Essentially, you are allowed to opt out of the pension scheme within 1 month, and if this is the case, any contributions made must be refunded by the employer. If they choose to leave the pension scheme after the opt out window has passed, then their contributions are not refunded, and they must stay in their pension until you reach the state pension age.

Record keeping:

There are also certain rules about the records you keep, and for how long. You are legally required to keep records on how you have met your duties, which includes the name and addresses of the staff who are enrolled, when each of the contributions were paid, any of the request to leave or join the pension scheme, and your pension scheme reference/registry number. Almost all of these records must be kept for 6 years, except for the requests to leave, which only need to be kept for 4 years. Also, you need to keep track of the ages and earnings of your employees so that you can enrol them when necessary.

How does it affect your corporation tax?

You might be wondering - what does this have to do with corporation tax? Well, essentially, you can claim any pension (the employers contribution) that was paid by the company as an expense, which helps to reduce the company's corporation tax. This is reflected separately to the wages paid in the income statement of the accounts, which is the same way national insurance contributions are reflected as well. When completing the tax return itself, this is just included in the company’s operating expenses, thus reducing the company’s taxable profits and the tax due, in turn.

Another way that pensions costs can affect your tax is if you are completing a research and development claim. When completing your R&D claim, you must enter the total PAYE/NIC liabilities that were made in the period, otherwise your tax credit pay out will be capped. You can include the pension costs in this figure, which will increase your tax credit cap and allow you to receive the full claim. Read our article ‘How to File a R&D Tax Credit Claim’ to find out more about how to file this.

How to report pension payments when filing:

Now that we know what pensions, qualifying earnings and employers contributions are and how they work, let's take a look at how to reflect them in your filings when it comes to submission time!

Income Statement:

In both the micro company accounts and small company accounts, the pension costs are reflected in the same way within the income statement.

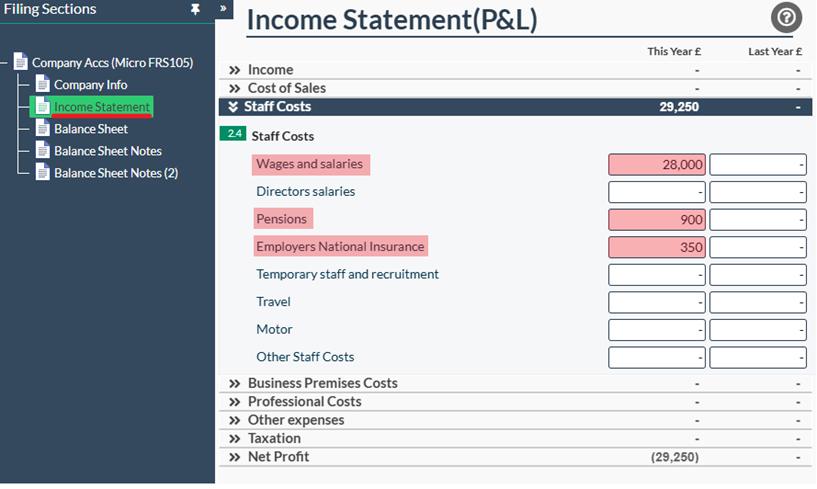

This is an example of the micro company accounts, but as you can see, they are reflected under 'Staff Costs' in their own category. There are also separate categories for the wages (full gross amount before deductions) and national insurance (employers contribution) costs as well. To access this page, you need to open the 'Micro Company IXBRL Accounts' template, and click on the 'Income Statement' tab to the left, where you will be able to view all the different income and expenses categories.

Corporation Tax Return (CT600):

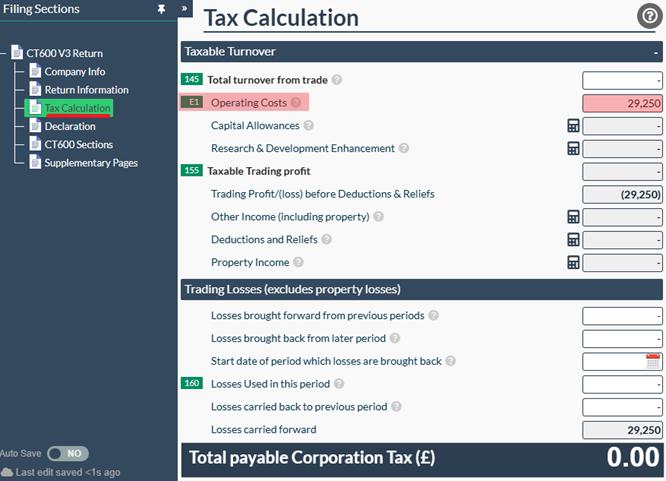

There is just one tax return to complete, irrespective of whether the company is micro or small, however, where the pension costs are reflected can be dependent on the type of company, such as a standard trading company, or a property company, etc.

Once you open the CT600 return templates, head to the Tax Calculation page and then enter the total expenses, including the pension costs, etc., in box E1, which is the operating costs box. For property companies, they would need to complete the Property Income page instead. You can find out more about this in our article 'How to File a CT600 for a Property Company'.

Hopefully you now have a better understanding on what pensions are, how the schemes work, and how they can affect your company when it comes time to file!