What is income?

In simple terms, income is any money that a company receives, which could be anything from sales from customers, money from the company director, interest from your bank, and many more - however, how you reflect it in your company accounts will differ depending on where it came from, or what type of company you are. Let’s take a quick look at each one.

- Sales from customers - this is money that you receive from products or services sold by the company. This is either done through actual payments made online or in store, or through invoiced payments.

- Money from directors - when a director gives the company money, it is typically either a loan that they made to the company, or an investment into it. If the money was a loan, then it would be reflected in the balance sheet, rather than the income statement, and is usually shown under the creditors section, as this is money that the company owes back to the director. If this was money that was invested into the company, then it usually would be reflected under the capital and reserves section of the balance sheet, however, it can sometimes be shown in the income statement, depending on the company.

- Interest from banks or loans - companies can also receive interest income, either from a bank or from any loans that they have given out and are charging interest on. This interest is taxable, and must be included in your company’s income statement under ‘interest income or similar’.

Now that we have covered a few of the basic income types, let’s dive into the difference between sales income and other income.

Sales Vs Other Income:

When you are completing the income statement in your company accounts, you will notice that there are two separate headings within ‘Income’ - one is ‘Sales’ income and the other is ‘Other Income’. You will need to use either one of these when recording the income received from the main period.

Sales Income:

What counts as sales income?

Sales income is any money that you received which was from your main source of trading income. For example, if your company is a standard trading company which offers products to customers, then you would typically enter the income you receive from customers under ‘Sales’. Any income received that doesn’t relate to the sales of the products or services should be entered as ‘Other Income’ instead. There is a catch though, because if you are a property company, any rental income received is still considered as ‘other income’ since this is a different type of exchange - but don’t worry, we’ll get into that more later!

So where do I reflect sales income?

Whether you are filing as a small or micro entity, there is a box within both of the company accounts where you can enter your income. To get started, simply add either the small or micro company accounts template and then head to the ‘Income Statement’ tab on the left-hand side of the template. Here you will be able to see the headings for each different type of income.

In the micro accounts, you see this:

In the small accounts, you will see this:

Even though the reporting standards are different, you simply need to enter your sales income in the ‘Sales’ box if it relates to your company’s main trade.

If you are also filing for company’s corporation tax return (CT600), then you will need to enter this sales income figure within the ‘Tax Calculation’ page of the return.

Please enter the total sales income for the period in the ‘Turnover from trade’ box (145). Please note that this should only include the sales income figure, as there is another section where you need enter any other income that was received. Now let’s move on to what this other income is and how to reflect it as well.

Other Income:

What counts as other income?

The other income section covers a much broader range of income types, which can be very useful if you are unsure where to reflect certain types of money the company received.

The main type of income that this section covers is income from property companies. Even though rental income is their main type of trade, there are different ways of treating this within both the accounts and the CT600 corporation tax return. So, if the company received any property income, this needs to be reflected under the ‘Other Income’ heading. Then, in the CT600 return, this income also needs to be reflected under ‘Other income’ within the ‘Property Income’ page. You can find out more on how to file for a property company in our article ‘Filing For a Company With Property Income’.

Other types of income that would be reflected under ‘Other income’ is any money that was received from sources outside the main source of income from trade. This covers any VAT refunds that were received, any dividends received from group companies, cashback, other expense refunds, commissions received, and more. If you are ever unsure where to input your income into your accounts, then it most likely will simply fall under other income.

Where do I reflect other income?

If you have received other income within the period, then you need to reflect it in the relevant boxes in both the company accounts and the CT600 return. Similarly to sales income, the entry boxes for both small and micro accounts are the same, even though each set of accounts are prepared under different financial reporting standards.

For micro accounts, you can find other income here:

For small accounts, you can find other income here:

As the small accounts are a little more complex, it is worth double check that your income doesn’t fall under any other of the other headings before entering it within the ‘other income’ box.

But the CT600 return is where sales income and other income really differ. In the corporation tax return, you need to enter your income into the ‘Other Income’ section instead - within here there are also multiple different headings to cater to the varying types of other income you can receive.

To access the Other Income page, please open the CT600 return template, head to the ‘CT600 Sections’ tab and switch box 95 to yes. This will then create the other income page where you can input your figures.

If your income doesn’t fall into any of the categories shown, then you can enter it within the ‘Income not falling under any other heading’ box - this page will allow you to add entries for other income along with a description of what the income relates to. This is usually where you would enter any VAT or sales refunds.

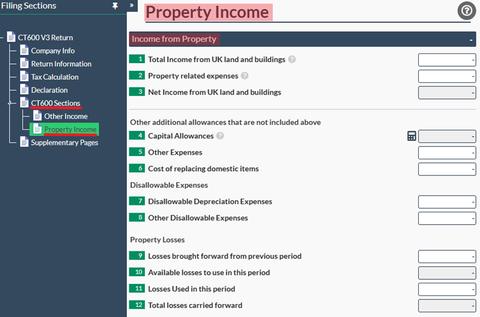

Furthermore, if you are filing for a property company instead, then you will need to enter this on the Property Income page - you can find this either by clicking on the calculator icon next to box 190 on the ‘Other Income’ page, or by heading to the ‘CT600 Sections’ tab and switching box 96 to Yes.

Any income, expenses, capital allowances, etc., that are relating to your property company should be entered on this page, instead of the Tax Calculation page. The rental income would be entered in box 1, expenses would be entered in box 2, and so on. Please read our article ‘How To File a CT600 for a Property Company’ for more guidance on how to complete this section.

It is important to remember that if your company is loss making but you have other income, that you need to also complete the ‘Deductions and Reliefs’ page to offset your trading losses against your income. It is worth reading our article ‘What are Deductions and Reliefs in a CT600’ if you are unsure how to reflect this.

Hopefully now you will have a better understanding between the different types of income a company can receive, and how to reflect both ‘sales income’ and ‘other income’ in your accounts and CT600 return!