What are fixed assets?

Fixed assets are noncurrent assets, meaning that they are expected to be used in the business for periods greater than one year. These typically include cars, buildings, fixtures and fittings, machines or equipment, etc. The cost of purchasing these assets is not included on the income statement as an expense, and instead, is only accounted for on the company's balance sheet as an asset.

However, for certain fixed asset items, you can claim capital allowances on them, which means that you can claim a portion of the cost of the item as an expense on your company's tax return, thus reducing the amount of corporation tax due.

If you are selling an item that you have claimed a capital allowance on, then you may get a balancing charge, which is subject to corporation tax.

Balancing Charges

Balancing charges are added to your company's profits if you have disposed of an asset in the period. A balancing charge is only added if you did not claim any other capital allowances in the period, or, if you sold the item for a larger amount than what you are claiming.

For example, if you are claiming a new capital allowance on a fixed asset item, however, you are also disposing of an item for more than the capital allowance is worth, then there is a balancing charge added to your taxable profits figure.

Example 1: Addition and Disposal (Profit)

In this example, we assume that there is a trading company with fixed assets of £5,650, however, they can only claim capital allowances on one of the machines (costing £2,530) that they purchased for their business, as the other fixed assets do not qualify for capital allowances. We will also assume that they have sold their vehicle which had a balancing charge of £12,500. A balancing charge is calculated by taking the difference between what you paid for an item and what you sold the item and any capital allowances claimed.

In their CT600 (corporation tax) return, they will need to input both the capital allowance that they are claiming, and the item that they are disposing of in the 'Capital Allowances' page:

Step 1: Once you have opened the CT600 return template, you will need to head to the 'CT600 Sections' page. Then, you will need to switch box 105, called 'Capital Allowances' to 'Yes'.

Step 2: Once in the 'Capital Allowances' page, you will need to first add the new item that you are claiming the capital allowance on in box Q15. To do this, you need to click on the green plus button next to the heading in box Q15. You can then select the type of capital allowance that you are claiming on the item, the description of the item, the AIA percentage if necessary, and the amount that the item cost.

In the example below, I have assumed that the company is claiming an Annual Investment Allowance (on plant and machinery - main pool) at 100%:

Since they are claiming an Annual Investment Allowance, I have kept the 100 in the AIA% box, meaning that they are claiming 100% of the cost of the item. The total AIA that they are claiming in the period is also showing in box 690 - this figure is automatically populated by our software depending on the entries made.

Step 3: After adding the new addition in the period, you can also add the disposal. To do this, you can click on the green plus button next to box Q20, called 'Disposals made in the period'. This will then add a line where you can enter the same information as in box Q15, except relating to balancing charge of the item that you are disposing of.

In this example, a special rate pool (plant and machinery) capital allowance was originally claimed on the item that is being disposed of in the period, so from the drop-down box, you need to select that same capital allowance type. The description box is just a brief overview of the type of item the fixed asset was - in this case, a vehicle - and then, in the final box, you just enter the amount that the vehicle was sold for.

In this case, there is a balancing charge which is added to the company's profits, since they made more from selling the capital item than they claimed as an expense for the other capital allowance type. See below:

£12,500 (the amount that the fixed asset was sold for) - £0 (any other capital allowances claimed in that same pool) = £12,500.

In this case, the company was not claiming any other capital allowances in the same pool, which was the special rate pool (plant and machinery), so the balancing charge of £12,500 was added to the company’s total profits for this period.

The capital allowance that was claimed in this period, equalling £2,530, is still added as an expense, so the profits are offset against this, leaving a taxable profit for the period of £9,970 (assuming no other trade had occurred in the period).

This means that the total tax to pay for this accounting period is £1,894.30:

£12,500 (the balancing charge) - £2,530 (the capital allowance claimed) = £9,970 x 19% = £1,894.30.

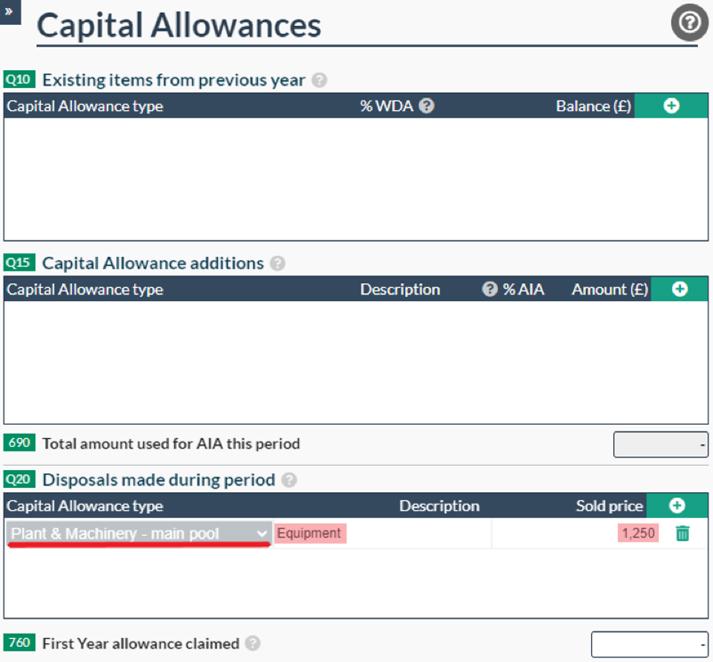

Example 2: Addition and Disposal (Loss)

In this example, we will assume that the company is claiming two new capital allowance items, and just disposing of one item.

The item that was disposed of in the period was a piece of equipment used by the business and it was sold for £1,250. We will assume that originally, a main pool (plant and machinery) capital allowance was claimed on this item, so that is the category that we will select from the drop-down box.

See below:

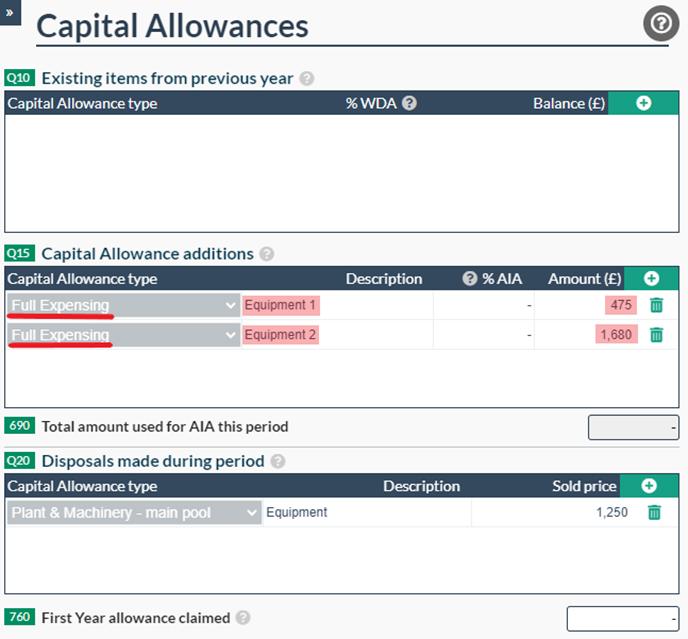

Then, we will assume that the other items that they are claiming capital allowances on are also equipment, so they are claiming a full expensing allowance (which is 100% of the cost of the item). One item cost £475, and the other item cost £1,680. Like below:

In this case, the disposal was less than the total amount of capital allowances claimed (equalling £2,155), so although a balancing charge will be added as the items are in different capital allowance pools, the balancing charge will be offset against the total capital allowances claimed in the corporation tax calculation.

£1,250 (the amount the disposal was sold for) - £475 (capital allowance for ‘Equipment 1’) - £1,680 (capital allowance for ‘Equipment 2’) = £-905.

This means that the company made a loss during this accounting period (assuming no other trade occurred), so there is no corporation tax due.

What about other types of fixed assets?

Sometimes, a company may have fixed assets that are not eligible for claiming capital allowances on. So, you may wonder what happens when you dispose of these?

Well, depending on whether you made a profit or a loss on the sale of the item, you either need to account for it as a chargeable gain or a capital loss.

Chargeable Gains:

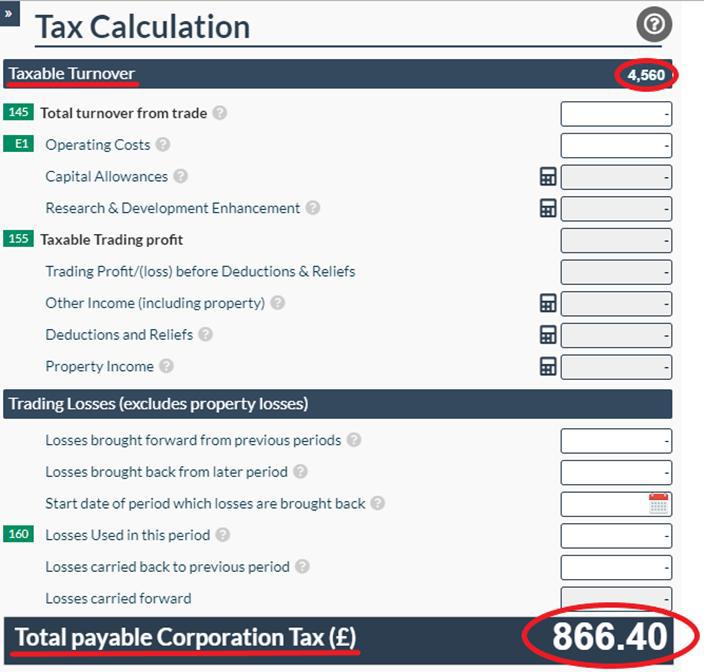

When you make a profit on the sale of a fixed asset item (usually when it’s value has appreciated since the time of purchase), it is liable for corporation tax – this is called a chargeable gain. You will need to account for this in the CT600 (corporation tax) return. The first step is to open the CT600 return, head to the CT600 sections tab, and switch box 98 to ‘Yes’.

This should now create the ‘Chargeable Gains’ page, where you can enter your figures. You will need to enter the gross chargeable gain in box 210 – this is the total of all chargeable gains if there were multiple in the period.

In this example, we will assume that there was a gross chargeable gain of £4,560 – so will enter this figure in box 210. See below:

As you can see, the net chargeable gain for this accounting period is just £4,560, as there were no capital losses to use against it. Assuming that the company had no other trade during the accounting period, this means that the total corporation tax due is £866.40 (which is £4,560 x 19% = £866.40.

Capital Losses:

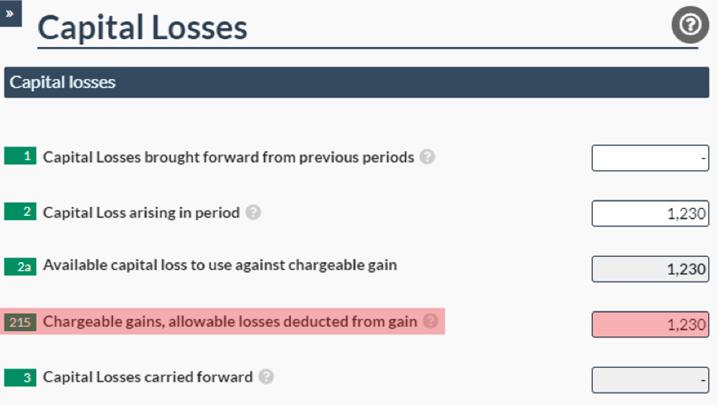

A capital loss is essentially the opposite of a chargeable gain. A capital loss is when you sell a fixed asset for less than you originally purchased it for (usually when the asset has depreciated in value over time). These losses can be used against any chargeable gains made in the period and will need to be accounted for in the CT600 return as well. To do this, you will need to head to the ‘Chargeable Gains’ page, then click on the calculator icon next to box 215, called ‘Allowable losses including losses brought forward’.

This will create the ‘Capital Losses’ page where you can enter any losses carried forward, any arising in the period, and if you want to use any of the losses against your chargeable gains.

In this example, we will still assume that there are £4,560 of chargeable gains in the period, but also £1,230 of capital losses, which we will then use against our chargeable gain. First, we need to enter the total capital losses from this accounting period in box 2 on the ‘Capital Losses’ page:

Then, if you want to use the losses against the chargeable gains, then you will need to enter the total amount you wish to use in box 215. In this case, the total chargeable gain is greater than the total capital losses, so we will use the full amount of losses in this period.

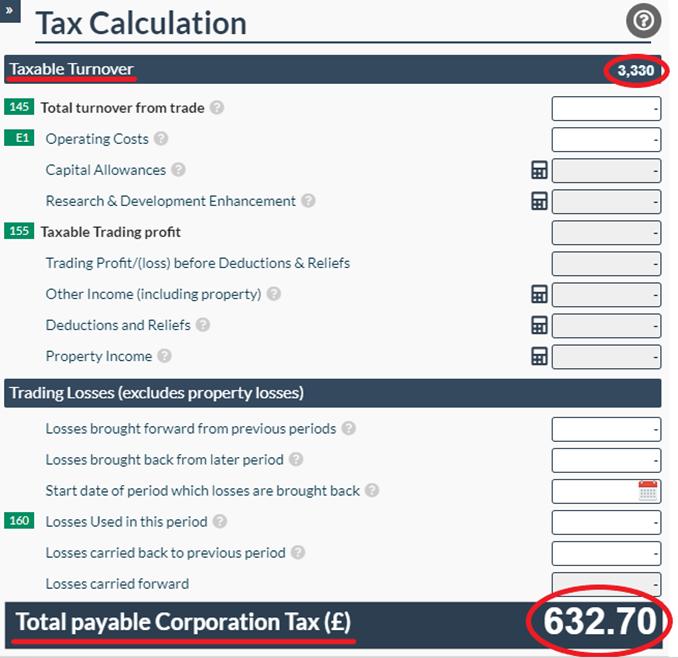

This will then use the losses to offset against your chargeable gains, meaning that the corporation tax due will be reduced. So, the total chargeable gains are now £3,330 (which is £4,560 (the total gross chargeable gains) - £1,230 (the total capital losses used) = £3,330).

Assuming that the company had no other trade during the period, its total profits are £3,330 (from the chargeable gain), meaning the total corporation tax due is £632.70 (£3,330 x 19% = £632.70).

To Conclude

The key points thing to remember is that there are different places within the corporation tax return to account for selling fixed asset items depending on whether it was eligible for capital allowances or not.

- If you originally claimed a capital allowance on the fixed asset item you have sold, then you need to account for it in the 'Capital Allowances' section of your return.

- If the fixed asset item you have sold was not eligible to claim a capital allowance on, then you need to account for it in the 'Chargeable Gains' page.

- If you made a profit, it is a chargeable gain, but if you made a loss, then it is a capital loss.

Hopefully, you should now have a better understanding of how to account for selling fixed assets when completing your company's returns!