Why many companies close down

There are numerous reasons as to why people close down a company: to go back to full-time employment, or to retire and kick your feet up or you want to work as a sole trader now. There are other reasons too, but what are your options and which one is best suited for you?

What you need to know.

When you want to close down, your limited company must have all its legal matters sorted. This is required by law before you can successfully close down your company.

As a limited company when you’re closing down, your first interests are the people you owe money to, who are called ‘creditors’. Legally, you are required to pay your creditors off before your directors or shareholders. This means any outstanding bills, money owed through any invoices, any running costs incurred, or any taxes needs to be paid.

If you are able to do this, you are a solvent company and you can apply to get the company struck off the Register of Companies.

Striking off the company is the cheapest way to close the company down.

You should seek professional advice from a solicitor or an insolvency practitioner if you’re not sure which option is suitable for you.

How much does it cost to close down a business?

This depends on the process best for the company. If you can dissolve your business, then all you need to do is submit a DS01 form to Companies House which will only cost you £33 via online or & £44 via paper application. Before applying to strike your limited company, you must close it down legally. This involves, announcing your plans to necessary parties and HM Revenue and Customs, dealing with your business assets and accounts and making sure employees are treated accordingly to the rules.

If you do not follow these rules, you could be fined and/or prosecuted.

There are other options if you cannot dissolve your company such as,

- Members’ Voluntary Liquidation (MVL)

- Creditors’ Voluntary Liquidation (CVL)

Members’ Voluntary Liquidation (MVL)

An MVL is a director-initiated process to shut down the company and distribute the assets as cash. In this case, the profits are distributed to shareholders as capital gain so it’s subject to Capital Gains Tax as opposed to Income Tax. Capital gains tax is at a lower rate than Income Tax so it means a much lower final tax bill for you. If you have a Business Asset Disposal Relief, the tax difference could be greater. Here are the steps to follow:

- Make a declaration that the company is solvent. Prepare the final financial statement to be sworn by a solicitor or a notary. Where there’s more than 1 director the statement must be sworn by at least the majority of the directors.

- Within 5 weeks of the declaration and the statement has been sworn by the directors, a company’s shareholders meeting must be held. At this meeting the shareholders/members will then be asked to pass a resolution to agree the company to be placed on liquidation.

- Appoint an authorised insolvency practitioner as a liquidator to take charge of liquidating the company. At this stage, the liquidator has full control of the company.

- This appointment should be published in The Gazette.

The liquidator will begin to settle creditor claims and make payments and look to distribute surplus funds to the shareholders/members. All creditors are entitled to receive an additional 8% interest on the amount already owed by the company. This is active once the liquidation process begins.

However, your MVL funds may be subject to income tax under specific conditions:

- Your company has five shareholders or fewer

- You get involved in a similar trade activity within two years

- The primary aim of your MVL appears to be tax avoidance.

Creditors’ Voluntary Liquidation (CVL)

A CVL is a director-initiated process that they decide to voluntarily shut down the company due to the business being insolvent. (Insolvent means to not have means of paying off debts). This needs to be agreed with at least 75% (by value of shares) of shareholders to pass what is called a ‘winding-up resolution’. Once this is made there are 3 steps you must follow.

- Appoint an authorised insolvency practitioner as liquidator to take charge of liquidating the company.

- Send the resolution to Companies House within 15 days.

- Advertise the resolution in The Gazette within 14 days.

After appointing the liquidator, the directors no longer have control of the company or anything it owns. They also cannot act for or on behalf of the company. The director must then give all information to the liquidator, hand over any company assets, records and documents and allow them to interview you if they ask.

Both of these options require a Licensed insolvency practitioner.

You also cannot apply for a voluntary strike-off once the insolvency proceedings have begun

Compulsory liquidation

Your company might be forced into compulsory liquidation if you can’t pay your creditors. Here are some necessary steps for ALL company closures

- Pay staff or make employees redundant

- Cease trading

- Advise creditors and suppliers that business has ceased trading.

- Sell your company assets (if you have any)

- Terminate contracts (relating to business, premises and assets)

- Prepare final company accounts, tax returns and paying any amount due

- Notify HMRC in relation to payroll, VAT, if applicable and any other taxes that apply.

- Close the company bank accounts.

What do I need to file?

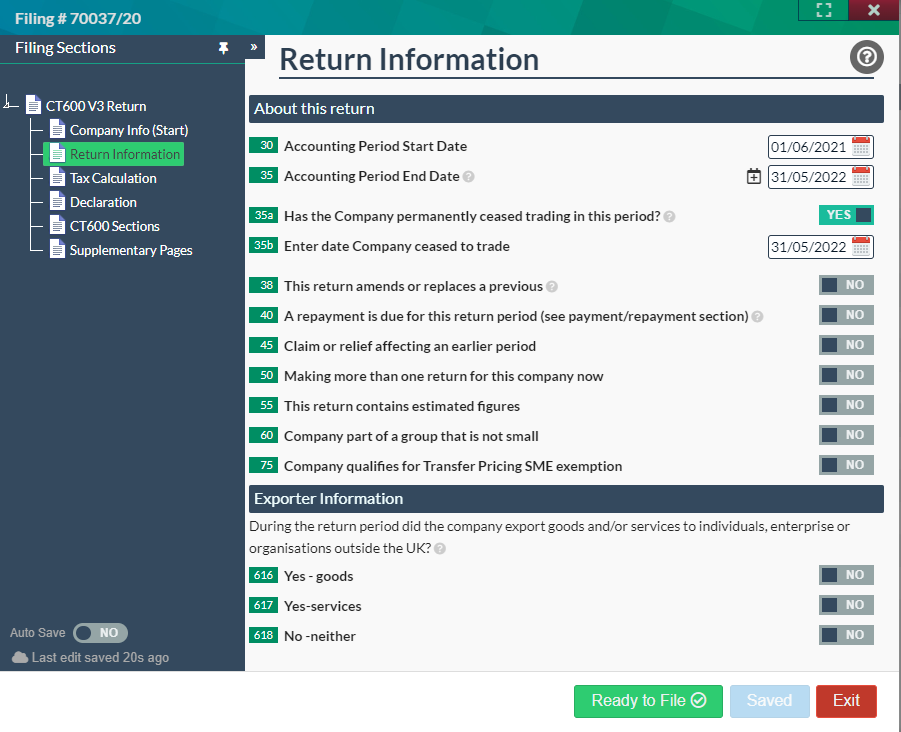

To close your Company, you will need to contact HMRC and agree a date that you last traded. You will then need to make a final return to this date, you can do this using our software at Easydigitalfiling. Once you have agreed a date with HMRC, you can file the final CT600 - in your return information page, please set box 35a to 'yes' and enter in the date you ceased trading.

Three months after this agreed date, you will need to complete a DS01 form at Companies House. This starts of the striking off procedure. Three months after this date, your company will be closed.

Let the company become dormant

You don’t have to close your company if it’s no longer trading. You can let it become ‘dormant’ for tax purpose as long as it’s not:

- Still trading

- Receiving income

Your company will still be registered on Companies House, so you will still need to send annual accounts and confirmation statement to them. A limited company can stay dormant for as long as you want. You can read more about setting your company dormant in our knowledge base article

Can I close a company and start a new one?

Yes, but there are some restrictions to this. HMRC look to prevent a process called ‘phoenixing’ which is where a liquidated company is reproduced again but with a similar or same company name. This is prohibited by Section 216 of the Insolvency Act. This act makes it illegal for any person who was a director of a company at any point in 12 months of that company going into liquidation to be involved in another company with the same or similar name for a period of five years.