Whatever business sector you are in, you will probably have been impacted in some shape or form by the Covid 19 epidemic. As part of the Governments' response to support businesses through this period, a number of packages were made available to some businesses which included the Bounce Back Loan Scheme (BBLS) aimed at micro businesses and the Coronavirus business interruption Loan Scheme (CBILS) aimed at small and medium enterprises. If you were fortunate to be able to take advantage of any of these schemes you may be wondering how to reflect these cash movements when creating your end of year accounts and related filings. In this article we look at how grants, loans and CJRS should be treated in Accounts, Computations, and the CT600 Corporation Tax Filings.

How do I account for Coronavirus Bounce Back Loan?

The Coronavirus Bounce Back Loan(CBILS) and the Bounce Back Loan Scheme (BBLS) were offered on preferential terms where the recipient does not have to pay any interest for the first 12 months, and then after that period pays interest on the loan over the remaining term of the loan. Both of these loans are accounted for in the same way that you would treat a normal loan from e.g a bank or other financial institution.

Reporting requirements for Corporation Tax in the CT600

As with the treatment of any other loans, CBILS/BBLS is not income, so therefore it is not included as part of your income in your CT600 tax calculation.

After the first year, when you start to pay interest on the CBILS loan, the interest incurred is included as a business expense and so will be an operating cost for to the Company and subsequently reduce Corporation Tax liability.

Accounts reporting

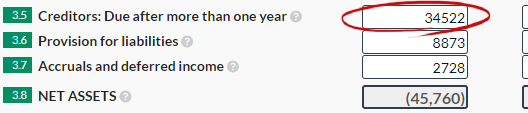

In the accounts that you submit with the Corporation Tax return, you will need to show the loan on your balance sheet, as a creditor due after one year.

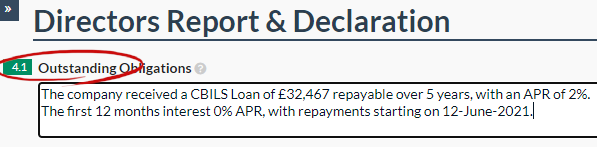

If you are a micro company, the loan should also be reported in the balance sheet notes under "Outstanding obligation."

The note should include the amount borrowed, the amount outstanding at the end of the accounting period and the interest charged.

If you are a small company, the loan should be reported in the Government grants and government assistance text area.

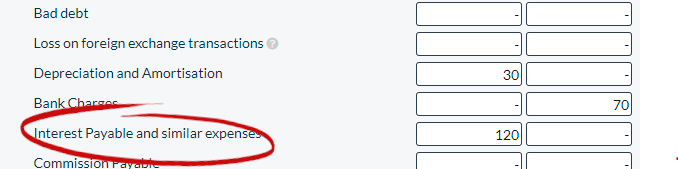

Once the company starts to pay, interest on your loan, the amount of interest paid during the period, should be included in your income statement under other expenses - interest payable and similar expense.

Coronavirus Job Retention Scheme (CJRS)

If you have had to furlough any of your employees during the corona virus pandemic and taken advantage of the CJRS then this needs to be reported in both your CT600 and accounts.

CT600 and CJRS

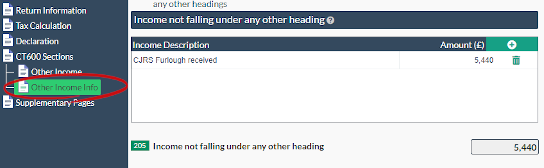

Enter in the amount of CJRS received into box 205 in the other income section and label as CJRS Furlough received

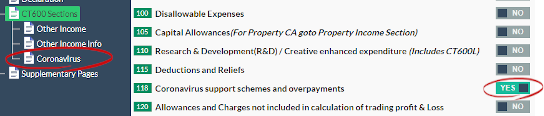

Now switch on Box 118 in the CT600 Sections sections:

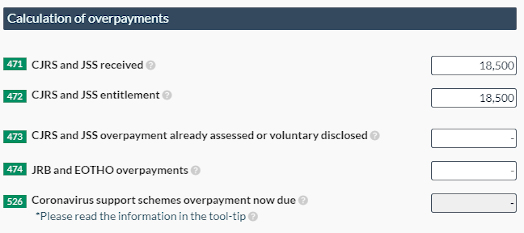

Enter in the amount of CJRS/JSS received into box 471 and your actual entitlement into box 472. If these two figures are the same, there will be no repayment calculated (box 526).

If you have received an over payment enter in the amount received in box 471 and your entitlement into box 472. Any overpayment will be populated into Box 526. If you already had an assessment made by HMRC for an overpayment, please enter into box 473.

If you have received an overpayment for CJRS, then HMRC will contact you to arrange repayment. It does not form part of your corporation tax calculation.

Accounts and CJRS

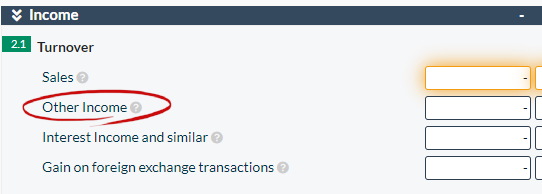

Enter any CJRS scheme in the income statement, under other income.

If you are a small company reporting under FRS102 1A, any CJRS should also be reported in the Government grants and government assistance text area.