Super-deductions were introduced by HMRC on 1st April 2021 as a CT600 relief to help companies investing in qualifying plant and machinery following the pandemic. Businesses investing in plant and machinery from that date can claim a 130% enhanced allowance within their Corporation Tax CT600 return for main pool assets or 50% for special pool assets.

What are Capital Allowances?

Capital Allowances are government allowances for items you purchase for use within the company. They are fixed assets such as equipment, tools, computers, furniture and vehicles. Items that you will have in your business and will generally be useful and last longer than a year. You can deduct some or all of the value of the item from your profits to reduce your corporation tax bill. Find out more about Claiming capital allowances

Super Allowances

As with the normal capital allowances there are 2 different types of super-deductions: the main 130% super-deduction, and the special pool rate which will give you a 50% deduction. These allowances are for new items only, second hand equipment should be included in your claim for annual investment allowance in your CT600 return. As a super deduction is included as first year allowances rather than annual investment allowance.

The items covered include:

- Computer equipment

- Office furniture

- Tractors, lorries, and vans

- Electric Vehicle charging points

- Machinery and equipment

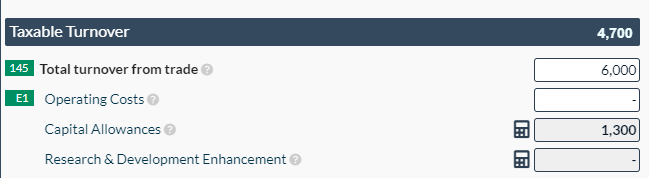

To illustrate the benefit of the super deduction, if you purchased a new computer equipment for your business at a cost of £1000, you would be able to add in the enhanced expenditure of £1,300 against your income to reduce your taxable profit.

The allowance is for any purchase made from 1st April 2021, however, looking forwards if your period ends after the 31st March 2023 then there will be a tapering of allowances available to claim.

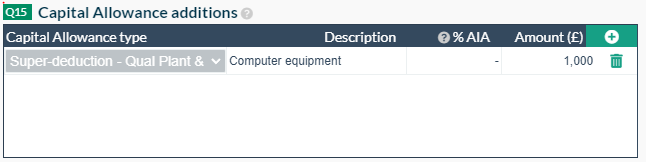

To claim this allowance in Easy Digital Filing, go to the capital allowances page under the CT sections.

Select the Super deduction allowance from the drop-down list and add in details and the cost of the item you are claiming.

The amount of the super deduction that is calculated and used in your tax calculation is shown on the CT600 tax calculation page:

50% First Year Allowance for Special Rate Items

Special rate items are items that are integral features such as long life assets or cars with a CO2 emission level over a certain threshold. Normally these items would only be allowed a writing down allowance of 6% each year.

If you purchase any of these items within the period, you can claim 50% of the cost in your tax return. The remaining 50% is then written down over the following years. This gives you an immediate advantage when calculating your corporation tax liability.

Disposals

There is one point that needs to be noted if you are claiming super deductions. This is if you dispose of the fixed asset within the chargeable period - from 1st April 21 to 1st April 23 - you must add back the sale price of the asset at 130%. For periods ending after the 1st April 23, the enhancement on the sale price is pro-rate. For periods starting after the 1st April 2023, only the actual sale price of the asset needs to be added back into the tax calculation.