What is a director's loan?

Let's start with the basics. What does a director's loan mean? There are two types of director’s loan that you ought to know about. One is where the director lends money to the company and the other is where the director borrows money from the company.

It is perfectly acceptable for a director to borrow money from their limited company. It can be viewed as a short-term and accessible source of finance. This type of director’s loan is not money that is used to pay a salary, pay out dividends or reimbursing yourself for personally paying for company related expenses. You may decide to take out a loan for a various number of personal reasons such as paying off personal expenses, paying off debt or using the company's business card to pay for non-business related expenses. There is no restriction as to what this money is used for and the amount borrowed. But it is crucial that you understand the tax implications of borrowing money from your company. These director's loan transactions are usually kept track of in a directors account.

To simply put it, the Section 455 (s455) tax charge arises if the director's loan is still owing to the company after 9 months from the end of the accounting period in which the director's loan was made and the company is a close company. So, it is best that the money is repaid in full as soon as possible. Section 455 refers to the relevant section of the Corporation Tax Act 2010. This section of the corporation tax act is only applicable to a close company.

What does a close company mean?

HMRC defines close company as a private UK company that is:

-controlled by five or fewer participators or,

-controlled by any number of participators, given they are also directors or,

- more than half of the assets can be distributed to the 5 or fewer participators or participators that are directors (conditions listed above) in the event of the company winding up.

Control of a close company can be defined by persons of the company collectively:

-owning over 50% of the company’s shares or,

-having over 50% of voting power or,

-receiving over 50% of the company’s income if distributed or,

-receiving over 50% of the company's assets if the company were wound up.

Also, a participator is defined by a person having a share or financial interest in the capital or income of the company. Examples include shareholders, loan creditors, directors etc.

Examples:

Company Tax LTD has 7 directors, which makes the company a close company.

Company Free LTD has 2 shareholder and 3 directors. This company is a close company as there are 5 or less participators.

In terms of the section 455 the tax rate is set at 33.75% for loans made following 6 April 2022. Directors loans made prior to this; section 455 Tax is payable at 32.5%. If the loan is greater than £10,000, you will need to pay interest at the official rate of interest on the section S455 tax liability. Interest is also charged until the loan is repaid or the tax is paid. The section 455 tax is calculated in the corporation tax return for the period that the loan was made, the tax is payable when the corporation tax is normally due for the period i.e 9 months after the end of the period.

How can I reclaim Corporation Tax paid on the director’s loan?

Whether the director’s loan has been repaid, written off or released, your company can reclaim the Corporation Tax paid on the loan. Essentially, the Section 455 tax is known as a temporary tax. However, any interest charged on the Corporation Tax cannot be reclaimed.

If you are reclaiming within 2 years of the end of the accounting period when the loan was taken out, you can use the CT600A form to do this. You can submit an amended CT600 for that period to reflect this. You can use the L2P form alongside the CT600 if either you are posting the CT600 Return or if the tax return is for a different accounting period than when the loan was taken out.

If you are reclaiming after 2 years or more after the end of the accounting period when the loan was taken out, please complete the L2P form alongside the latest CT600 Return.

You will be repaid either by the bank details provided in your latest CT600 Return or HMRC will send a cheque to the company’s registered address.

Please note that you cannot claim until 9 months and 1 day after the end of the CT600 Return’s accounting period in which the loan has been repaid, written off or released. Repayment will follow after this period has passed.

Example:

Your company’s accounting period ends on 30 June 2023. During this period, you, the director, borrows £9,000. This director's loan has not been repaid within 9 months, and so the section 455 Corporation Tax amounting to £3,037.5 arises. Let’s say the directors loan was repaid fully by the director in 30 Sep 2024. As this repayment, was made in the accounting period ending on 30 June 2025, the company cannot claim the tax paid until 31 March 2026.

HMRC do impose a deadline with reclaiming the section 455 Tax. This must be done within 4 years of the accounting period in which the directors loan was repaid. Let’s say, the directors loan was repaid fully on 27th November 2022 and the company’s year-end falls on 31 Dec 2022, the section 455 tax can be claimed by 31 Dec 2026.

What is the L2P form?

If you have repaid your director's loan, you can complete the L2P (loan to participators) form digitally through HMRC’s website to claim relief on your section 455 tax. You will need the company’s UTR number and the bank or bank society details, so that HMRC can issue you a refund if you are entitled to the relief. You will need your Government Gateway user ID and password so that you can access the online service.

Other details required include:

-The starting and end dates of the accounting period that the loan was made

-The date the loan was made

-The starting and end dates of the accounting period in which the loan was repaid, released or written off.

-The date and value the loan or part of the loan was repaid, released or written off.

-The due date of the relief

How to complete the CT600A using the software:

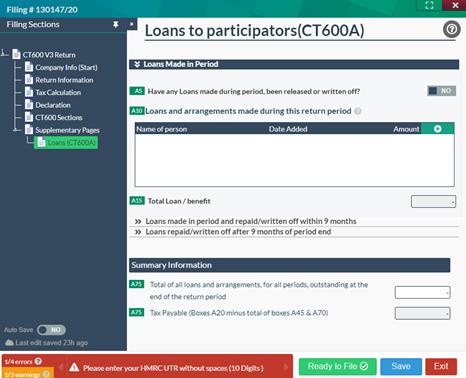

Step 1: After you have added the CT600 filing to your account, in the CT600 Return, you can access this page, by clicking on ‘supplementary pages’ and switching box A to YES . This will then include the CT600A loans and arrangements to participants by close companies.

Step 2: Then, open the CT600A and complete the director's loan to participators page as required.

If you are submitting an amended tax return, please remember to switch box 38 to YES, under the ‘return information’ page. Find out more details on submitting an amended CT600 Return

In the following example, I will demonstrate how the CT600A page is to be completed and explain how the tax is calculated.

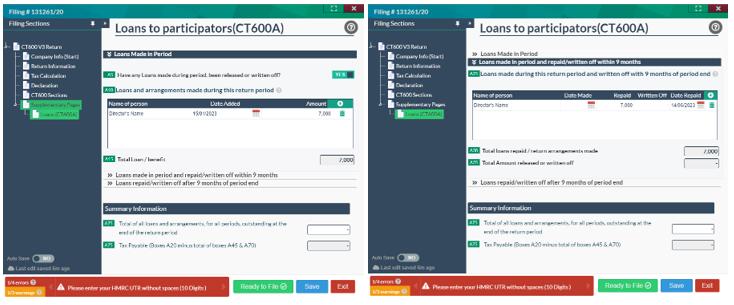

Company XY LTD is a close company and their accounting period ends on 31 December each year. We will say that the movements in the directors loan account are as follows: director borrows £7,000 on 15 Jan 2023. This money was repaid fully by the director within 9 months, and so it will not be subject to the section 455 at 33.75% tax. As shown below, the tax payable amounts to £0.

You will note that I have entered the name, date the loan was taken out and the amount in section A10. The software will automatically populate the total loan amount in A15. In this case, there was only one loan arrangement made amounting to £7,000.

As the director's loan that was made in the period, was repaid fully within the 9 months, I have completed section A25. Similarly, I have entered the name, the amount repaid and the date the loan was repaid. In box A30, the total loan repaid will be populated. You will find that the tax payable is £0, as indicated by box A75.

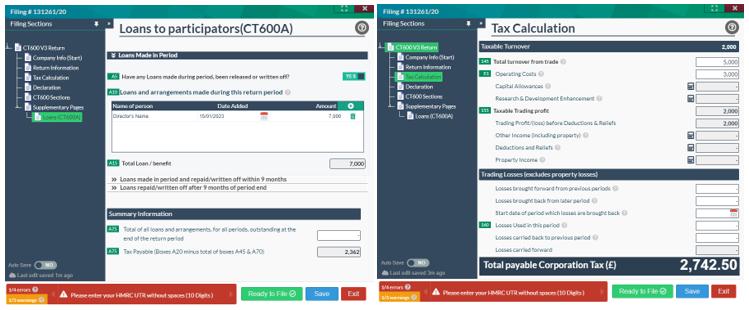

Now, let us consider a scenario where the £7,000 loan is still outstanding by the end of the accounting period (31 Dec 2023). So, the tax charged amounts to £2,362.50 (£7,000 * 33.75%). This will be reflected in the tax calculation of the CT600 Return and if the company has made a profit in the period, the total tax due will be displayed.

For example , we will say the company's turnover was £5,000 and the operating expenses was £3,000. With no capital allowances to claim and no disallowable expenses to consider, the tax payable on the net profit is £380 (£2000 * 19%). In total, the Corporation Tax due is £2,742.50.

Hopefully, this article has helped you understand the tax implications of a a director's loan and how you can reclaim the temporary tax paid on the loan. If you do have any questions about this, please do not hesitate to contact us for technical support. If you are interested in reading about articles related to Corporation Tax, take a look!