What Are Interest Rates?

Interest rates are the cost of borrowing money, typically expressed as a percentage of the loan amount. They play a crucial role in the UK economy by influencing consumer spending, business investments, and overall economic growth. For businesses, changes in interest rates can affect operating costs all the way to expansion plans. Higher rates typically lead to higher borrowing costs, whilst lower rates can lead to lower borrowing costs. Therefore, lower rates are likely to stimulate economic growth. The Monetary Policy Committee (MPC) meets eight times a year to review economic conditions and adjust interest rates accordingly, to maintain stable economic growth and to control inflation.

*Base Rate: Rate the Bank of England (BoE) charges commercial banks. Commercial banks then pass this on to customers.

What Causes Interest Rates To Fluctuate?

Inflation:

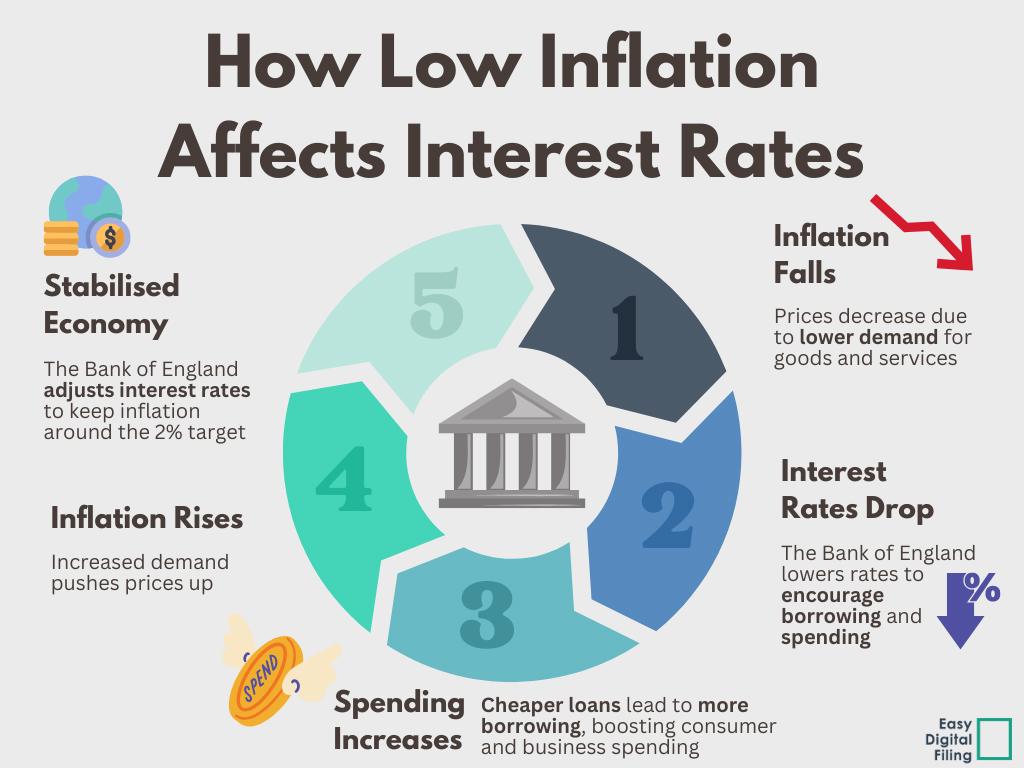

When inflation increases, the MPC may raise interest rates to counteract it. Inflation often arises from increased spending on goods and services within the economy, which can be driven by lower interest rates (cheaper borrowing). To combat this, the MPC raises interest rates, making borrowing more expensive. As a result, the demand for borrowing typically decreases, which can help reduce inflation.

On the flip side, when inflation is low, the MPC might lower interest rates to boost it. If they choose to reduce interest rates, borrowing becomes cheaper and more accessible for individuals and businesses. This usually leads to a rise in the demand for borrowing, which increases spending in the economy and drives inflation.

Economic Growth:

Economic growth is measured by calculating real gross domestic product (GDP). GDP can influence interest rates in several ways. Rising GDP indicates a strong economy, which can lead to higher demand for goods and services. To prevent the economy growing at an unsustainable rate and causing excessive inflation, the MPC may raise interest rates to slow growth and keep inflation around the government's 2% target.

Contrarily, when GDP shows signs of slow growth, it indicates a weaker economy. In response, the MPC may lower interest rates to stimulate borrowing, investment, and consumer spending, helping to boost economic activity.

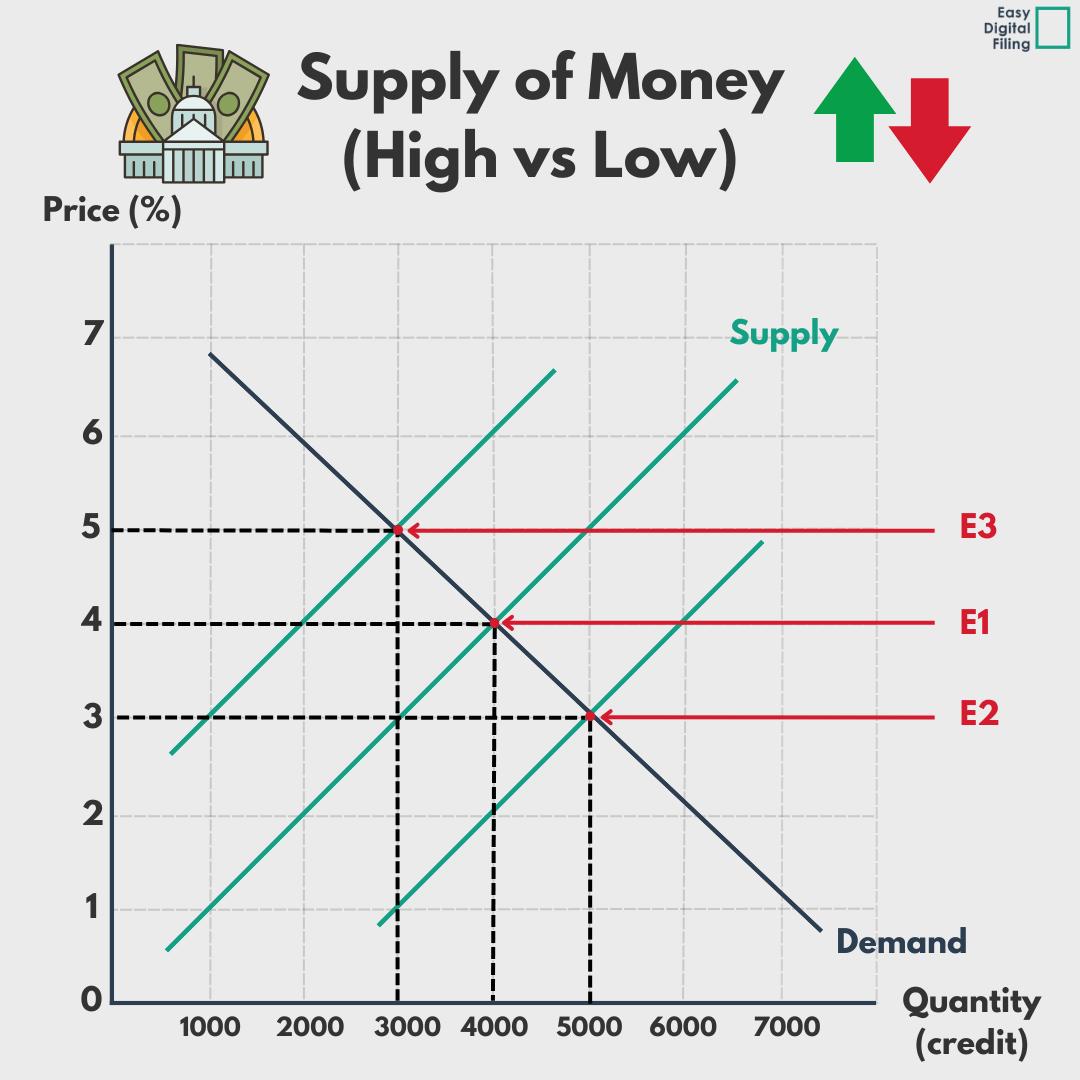

Supply & Demand For Credit (Money):

Supply of Money (High vs Low):

The supply of money can shift in two different directions, one being an increase in supply and the other being a decrease in supply. An increased supply means there is more money readily available for financial institutions to lend to businesses and individuals, therefore reducing interest rates. When the supply of money decreases, the opposite will ensue - interest rates will increase. Below, we can see how increasing and decreasing the supply of money can help determine the interest rates charged by financial institutions.

- Price = Interest Charged

- Quantity = Credit Available for Financial Institutions to Loan

E1: The equilibrium price is where the supply and demand curves intersect. In this example you can see that where the two curves intersect at E1 (Equilibrium 1), the base rate is 4%.

E2: Looking at the graph above we can see that there has been an increase in the supply of money. An increase in the supply of money means that money is more readily available, therefore driving down the price of money (the interest charged). The equilibrium has shifted from E1 to E2. Looking at the price (%) axis and the quantity (credit) axis you can see that the price has fallen and the quantity of available credit has risen.

E3: This is the equilibrium for an decrease in the supply of money. So, if we were to flip everything mentioned above; this means that the price of money (% charged) has risen, making it more expensive to borrow. Looking at the price (%) axis and the quantity (credit) axis once more, we can see that the price of borrowing money (% charged) has risen sharply and the quantity (credit) has fallen.

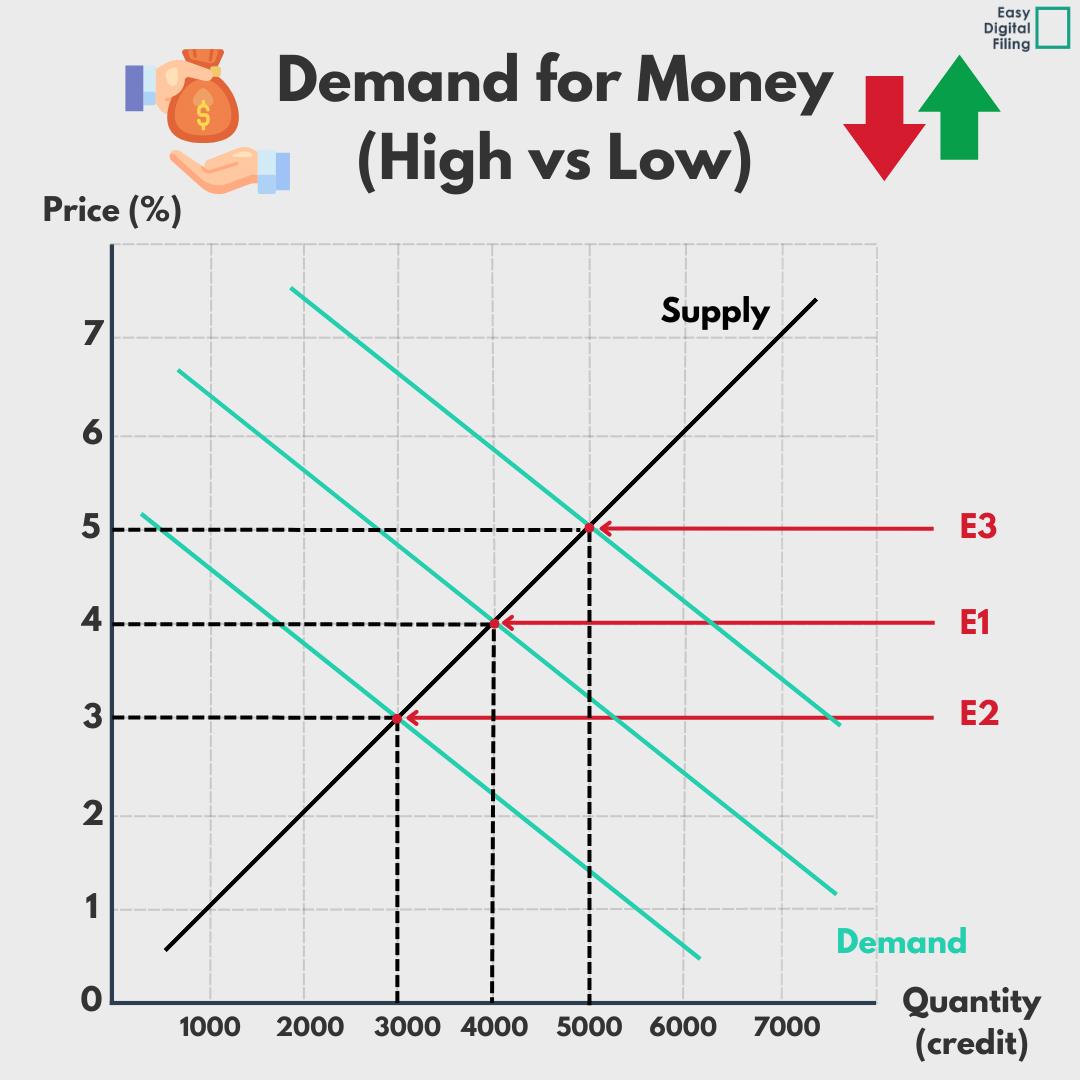

Demand for Money (High vs Low):

The demand for money can fluctuate for many different reasons. For example, during the Covid-19 pandemic, the demand for borrowing money was low, which resulted in UK interest rates reaching their lowest point ever on March 19, 2020, at just 0.1% [1]. On the contrary, on November 15, 1979, interest rates peaked at 17% [1], mainly due to rising wage demands, which led businesses to borrow more to meet these increased demands. The following section illustrates how an increase in the demand for money can influence the interest rates set by financial institutions.

E1: In this example equilibrium 1 (E1) is the base rate of 4%.

E2: From the graph shown above you can see that there has been a decrease in the demand for money. Let's imagine this is March 2020 and covid is at its peak. With the majority of individuals not leaving their house, this meant a huge decrease in spending and borrowing, seeing a downwards shift in the demand for credit. This has therefore driven down the demand for money and shifted the price (%) charged to equilibrium 2 (E2). Alongside the price being driven down, the quantity (credit) available has fallen sharply.

E3: E3 reflects an increase in the demand for money. This shows that the price of money (% charged) has risen, making it more expensive to borrow. Looking at the price (%) axis and the quantity (credit) axis, we can see that the price of borrowing money (% charged) has risen sharply and the quantity (credit) has fallen.

How Will Lower Interest Rates Affect My Business?

On the 6th Feb 2025 interest rates were cut once again to 4.5%. This is following a downwards trend which is great news for small businesses. Interest rates are predicted to be cut a further 3 times in 2025, closing the calendar year with a base rate of 4% [2]. As a business owner it is essential that you understand these rates and how they may impact your business.

Borrowing:

Low interest rates typically reduce the cost of borrowing money and repaying variable rate business loans. The decrease in borrowing costs can improve cash flow, allowing businesses to use the funds for more productive purposes or to support other investments. It could provide the opportunity to develop new products or invest into new equipment.

Overheads:

Overheads can be defined as any expense incurred to support the business, that aren't directly related to the cost of the product or service. For example, rent, insurance, legal fees, marketing, postage etc. Low interest rates can lower business rents by increasing property supply as landlords borrow more to invest in real estate. Furthermore, interest rate cuts should see commercial mortgages getting cheaper. Lower interest rates are especially beneficial for property companies, this will be explored in further detail later on in the article.

Consumer Spending:

Lower rates on mortgages, credit cards, and personal loans can increase consumers disposable income, providing them with more money to purchase goods and services. Additionally, they may feel more confident about taking out low interest loans for bigger purchases (e.g. a new car). This is positive news for small businesses, as they are likely to see a boost in revenue from the rise in consumer spending.

Good News For Property Businesses

Increased demand for property:

Lower Mortgage Payments: If your business owns properties with mortgages, low interest rates can reduce your monthly mortgage payments, which will improve cash flow. This can be especially beneficial if your business relies on rental income.

Lower Borrowing Costs: When interest rates are low, it becomes cheaper to borrow money. This makes it likely that more buyers can afford to apply for mortgages, which increases demand for both residential and commercial properties. This could lead to more sales or rentals for your company.

Better cash flow for leasing/renting

Lower Mortgage Payments: As mentioned above, if your company owns properties with mortgages, low interest rates can reduce your monthly payments, therefore improving cash flow.

Strong Tenant Demand: Since mortgages are likely to be more affordable and easier to obtain, more people may opt to rent rather than buy, resulting in increased demand for rental properties. This is likely to result in your property business attracting more tenants, increasing cash flow, and potentially enabling you to expand your property portfolio.

Rising property prices:

Property Value Appreciation: With more people able to afford mortgages, demand for property increases, which often leads to rising property values.

Flipping Opportunities: Property development companies will also benefit from lower interest rates. They have the potential to acquire properties at a lower cost, therefore improving profit margins.

The 2025 Outlook For Interest Rates

There is no shortage of expert opinions when it comes to interest rate forecasts. According to KPMG, due to persistent inflation, experts anticipate the Bank of England will adopt a more careful approach on reducing interest rates. This could involve three cuts in 2025, lowering the Bank of England base rate to 4%. On the other hand, analysts at Goldman Sachs have adopted a more bullish approach, predicting more aggressive cuts next year, and forecasting the Bank of England base rate to fall to 3.25% by the end of 2025 [3].

References:

[1] https://www.bankofengland.co.uk/boeapps/database/Bank-Rate.asp

[3] https://www.goldmansachs.com/insights/articles/uk-economic-growth-may-lag-expectations-in-2025