What is group relief and How does it work?

Group relief, (also known as group loss relief and consortium relief) provides a way for loss making companies to offset their losses and expenses against another profit-making company within the group. As per HMRC guidelines group relief essentially offers relief from corporation tax, reducing the tax bill for the company who claims the loss, while allowing the loss-making company to eliminate losses it would otherwise have to carry forward.

Where companies are normally treated as separate economic entities, the group relief rule allows loss making companies to transfer (or surrender) their losses to profit making companies within the group, treating the group as one economic unit for tax purposes to reduce the amount of corporation tax owed.

Although not a legal requirement it is also common practice for the profit-making company to pay tax saved through taking on the losses, back to the loss-making company. In other words, the profit-making company remains economically neutral because it pays the tax it would have paid to HMRC to the loss-making company instead.

The following losses and other amounts can be surrendered and claimed as group relief:

- Trading loss

- Capital allowances excess

- Non-trading deficit on loan relationship

- Amounts allowable as qualifying charitable donations

- UK property business loss

- Management expenses

- A non-trading loss on intangible fixed assets

What are the time limits for claiming group relief?

There is a two-year deadline from the end of the company’s accounting period for any available group relief to be claimed.

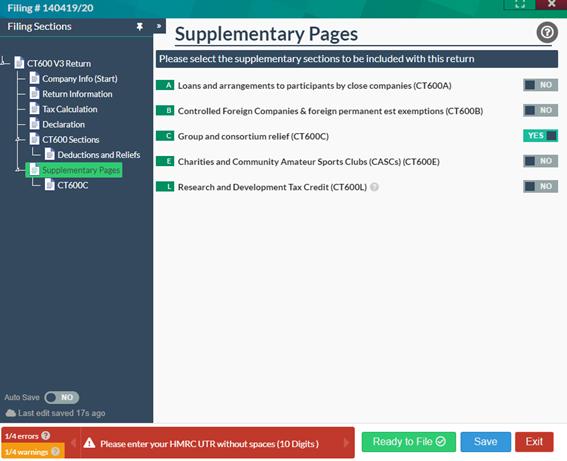

How to file group relief though the software?

To file for group relief, you can access this by opening the CT600 return, and in ‘supplementary pages’, switching box C to YES.

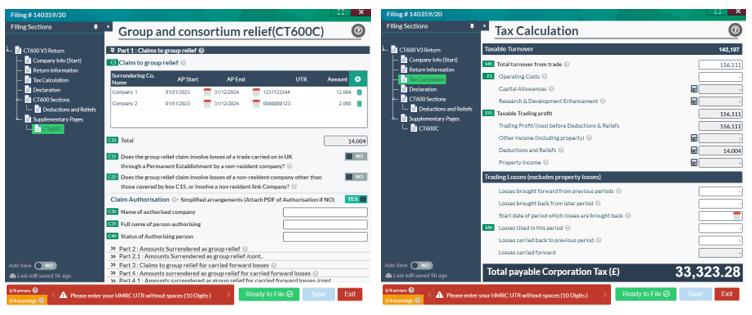

Part 1: Claims to group relief

This section is relevant if you are claiming group relief in the calculation of the Corporation Tax payable. If you are receiving a loss from another company to offset against the Corporation Tax bill, then please complete this section.

To begin, complete box C5 by entering the surrendering company name, start and end of the accounting period, company UTR, and the amount being surrendered. You can add more surrendering company details if applicable, and the total will be populated in box C10.

Unless a simplified arrangement is in place, HMRC will expect a copy of each surrendering company’s notice of consent to the claim to be attached and uploaded.

What is the simplified arrangement?

It allows for an authorised company to act on behalf of the authorising companies (all members of the same group) through a written statement of the claims and surrenders. To set this up, an application should be made in writing to HMRC. The written application must be made by the authorised company on behalf of itself and the authorising companies. Details on what should be included within the application are covered in HMRC'S manual.

What does a notice of consent cover?

This replaces the simplified arrangement. If the simplified arrangement is not in place, the following is expected to be uploaded as a supporting document:

-name of surrendering company

-name of company to which the relief is being surrendered and the amount

-accounting period to which this surrender corresponds with

-Tax Office details and references for the claiming and surrendering companies

Boxes C30-C40 should be completed if the simplified arrangement is already in place. Switch the box to YES, and enter the name of the authorised company, full name, and status of the authorising person.

As shown in this example, this company is claiming losses that amount to £14,004 from the 2 surrendering companies in the group. As the company's taxable turnover was £156,111, the losses were offset against the profits, reducing the Corporation Tax bill to £33,323.28.

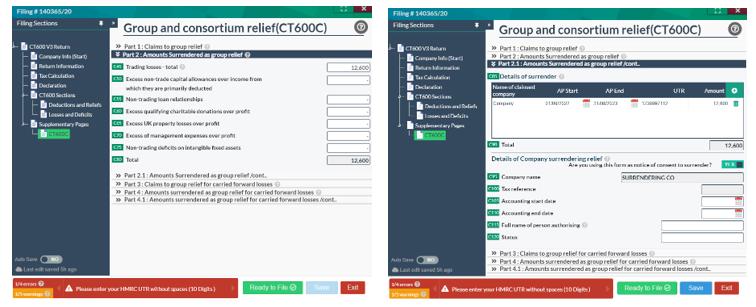

Part 2 + 2.1: Amounts surrendered as group relief

Both sections (2 + 2.1) should be completed. This should be completed if the company has made a loss and wishes to surrender its losses to another company within a group.

In boxes C45- C75, the losses should be split into the appropriate categories covered by the boxes. In this example: trading losses of £12,600 are being surrendered.

The details of the company claiming these losses from the surrendering company should be entered in box C85. Similar to part 1, the name of the claimant company, accounting period, UTR and amount surrendered should be completed. The total will be populated in box C90.

Again, if a simplified arrangement is not in place, you can use the form as a notice of surrender to surrender. Switch to YES and complete boxes C105-C120. You can also upload consent details as a supporting document.

If the company is surrendering losses as group relief, the losses and deficit and excess pages of the CT600 are also expected to be completed.

To explain the figures in the following example, let us say the surrendering company made trading losses of £24,430 and wishes to surrender £12,600 of its losses as group relief. After completing CT600C, you will find that in the tax calculation, the remaining losses that can be carried forward are £11,830 (£24,430 -£12,600). You will be able to see this on the main tax calculation page of the CT600 return.

Part 3: Claims to group relief for carried forward losses

This is similar to part 1, but this section is only to be completed if the company is receiving a carried forward loss from the surrendering within a group. You can use the losses to reduce the Corporation Tax bill.

Details of the surrendering company should be entered in box C125 (name of the surrendering company, accounting period, UTR, amount surrendered should be completed), and the claim authorisation section should be completed if required.

Part 4 + 4.1: Amounts surrendered as group relief for carried forward losses

Similar to part 2 + 2.1, this section should be completed if company has carried forward losses and wishes to surrender those losses to another company in its group.

Losses should be entered accordingly in boxes C160 -C180, and details of the claimant company will need to be completed in box C190. Again, if notice of consent to surrender is required (if the simplified arrangement is not in place), you can also complete this part of the form C210- C225.

If you would like further information on group relief, this knowledge base article on understanding group relief will help you understand the basics.