What is Creative Tax Relief?

Creative Tax Relief is a range of UK corporation tax incentives designed to support businesses operating within the creative industries. If your company produces qualifying creative content, you may be able to reduce your corporation tax bill or, in some cases, receive a payable tax credit from HMRC, even if you are loss making

These reliefs recognise the unique costs, risks and long production cycles involved in creative projects and are tailored specifically to businesses within the creative sector.

Who can qualify for Creative Tax Relief?

Your company may be eligible to claim Creative Industry tax reliefs or expenditure credits if it:

- Is liable for paying Corporation Tax

- Plays an active role in planning and decision making

- Directly manages contracts, negotiations, and payments for goods, services, or rights

Is directly involved in the production and development of projects in the following sectors:

- Film production

- High-end television

- Children's television

- Animated television

- Video games

- Theatrical productions

- Orchestral concerts

- Museum or gallery exhibitions

You should take full responsibility for the production in a way that fits your specific industry. For example, for a film, TV programme, or video game, this means overseeing everything from the start of development to completion, while for a theatrical production, orchestral concert, or exhibition, it means managing the production, running it, and seeing it through to closing.

What is the Cultural Test?

The cultural test determines whether a production qualifies as British Certified, which is a core requirement for claiming Creative Tax Relief.

To qualify, a production must pass the Cultural Test and obtain a cultural test certificate from the British Film Institute (BFI). When the requirements are satisfied, the BFI grants certificates after evaluating applications and administering the Cultural Test. Although the Digital, Culture, Media and Sport (DCSMS) does not evaluate productions or issue certificates, it adopts the Cultural Test and establishes the policy framework for the Creative Tax Reliefs. Therefore, productions must obtain a Cultural Test certificate from the BFI in line with DCMS policy.

How the cultural test works? (Points-based system)

The Cultural Test operates on a points-based system. A minimum number of points must be achieved by the production to pass the Cultural Test, and the required threshold is dependent on the type of production (film, television, animation, video games).

- 16/35 points for animation (film or TV) and 16/31 for video games.

- 18/35 points for Children's Television, Film, High-End Television.

All tests broadly assess the same four areas:

1. Cultural Content

- Assesses whether the story, characters, language, or setting reflect British or EEA culture.

2. Cultural Contribution

- Considers whether the production contributes to British culture, creativity, or heritage.

3. Cultural Hubs

- Looks at where key production activities take place, such as filming, animation, or development in the UK.

4. Cultural Practitioners

- Awards points based on the nationality or residency of key cast, crew, developers, or creative leads.

Industry-Specific Requirements

Some additional conditions apply depending on the type of creative production:

Film & Animation

- You must oversee the entire production process including:

- Pre-production.

- Principal photography or animation.

- Post-production.

- Final delivery.

Video Games & Orchestra

At least 25% of your core production costs must be spent on goods and services within the EEA.

Theatre & Orchestra

Your company must manage the production from start to finish, including directly employing and engaging performers. With Orchestra Tax Relief, performances must be live and presented to a paying audience or for educational purposes.

Creative Expenditure Credit

Historically, Creative Tax Reliefs were industry-specific, with separate reliefs for:

Film Tax Relief – rate of relief of 25% has applied to all films on qualifying expenditure. Core expenditure is the spending associated with pre-production, main filming, and post-production activities.

High-End Television (HETV) Tax Relief – claimable if it qualifies as British, intended for broadcast, or drama, comedy or documentary. To qualify, at least 10% of the core expenditure must be spent in the UK, among other eligibility criteria.

Children’s TV - qualifies as British by either passing the Children’s Television Cultural Test, at least 10% of the core expenditure is spent in the UK, primary target audience is children under the age of 15, intended for broadcast.

Animation - qualifies as British by either passing the Animation Cultural Test, at least 10% of the core expenditure is spent in the UK, intended for broadcast, and at least 51% of the total core expenditure is on animation

Video games - qualifies as British by either passing the Video Games Cultural Test, at least 25% of the core expenditure is spent on goods and services provided from the UK or EEA, and intended for supply to the general public.

From 1 April 2024, the UK introduced a new system of taxable expenditure credits, replacing most previous reliefs.

There are now two main types of credits:

Audio-Visual Expenditure Credit (AVEC)

AVEC applies at the following rates:

- Films – 34%

- High-end television programmes – 34%

- Children’s television programmes – 39%

- Animated television programmes – 39%

Video games expenditure credit (VGEC):

VGEC applies to British-certified video game productions at a rate of 34%.

Both of these credits are taxable and calculated on qualifying expenditure.

How can Creative Tax Credits be used?

- Offsetting other taxable liabilities.

- Surrender to group companies.

- Pay or reduce your corporation tax.

- Be paid as a payable credit where applicable.

Closures and key dates

From 1 April 2025, new productions must claim under the new regime - AVEC or VGEC.

The existing reliefs for all productions from 1 April 2027 will cease entirely and all qualifying expenditure must be claimed through the following updated credits:

- Audio-Visual Expenditure Credit.

- Video Game Expenditure Credit.

How to Claim Creative Tax Credits through Easy Digital:

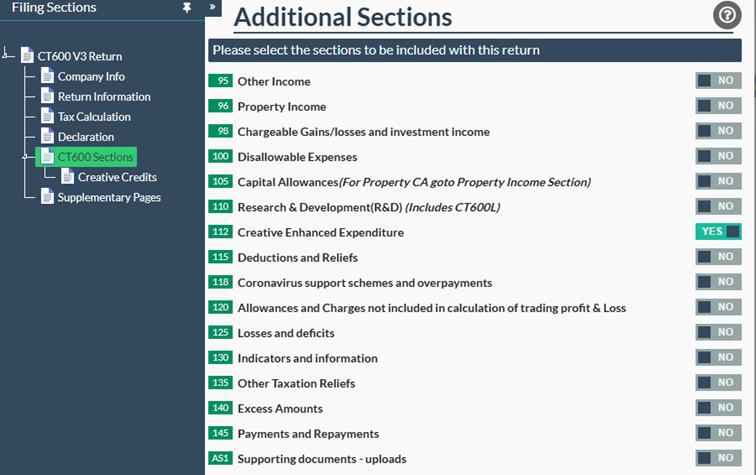

Open your CT600 return template, and click on ‘CT600 Sections’ (under the filing section column). Next, switch Box 112 ‘Creative Enhanced Expenditure’ to YES. This will open a new Creative Credits page.

Next, you will then be able to fill out the details within this page as shown below.

Get started with Easy Digital Filing

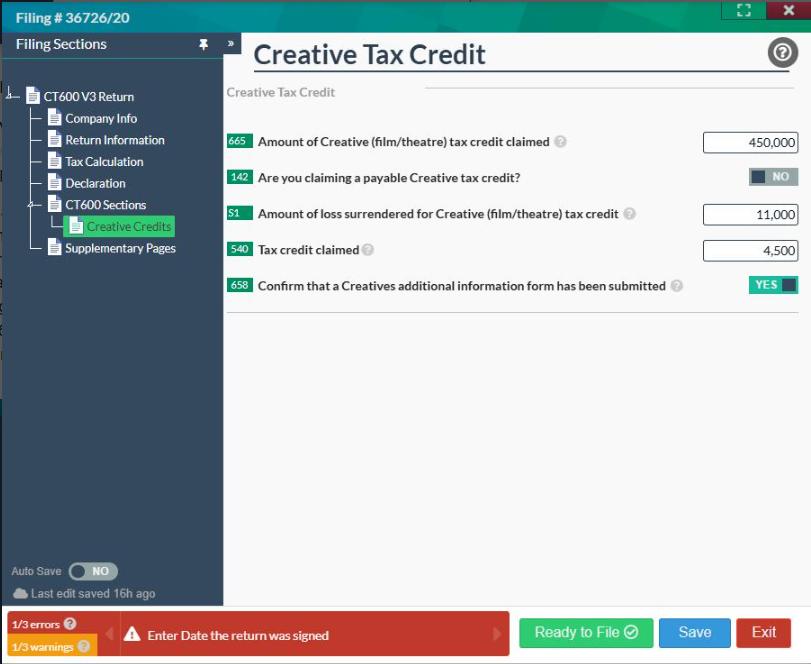

In this example we have a company that works within the film industry. In the accounting period, the company incurred qualifying creative production costs and recorded a trading loss. Rather than carrying this loss amount forward, the company chose to surrender part of it in order to claim Creative Tax Credit.

- We have an amount of £450,000 this is the amount of Creative Tax Credit claimed shown in Box 665.

- The company is not claiming any payable credit, as confirmed in Box 142.

- The loss surrendered for the Creative Tax Credit is recorded in Box S1 as £11,000, this helps to reduce future tax liabilities.

- The resulting tax credit claimed appears in BOX 540 as £4500.

- Finally, Box 658 confirms that the required creatives additional information has been successfully submitted.

Please note that:

Under the new Creative tax relief regime there is meant to be the new CT600P. This has since been delayed by HMRC, and they are looking to bring it in by April 2026. So please note that BOX 541 in the CT600 form will not be available to input a figure (until 2026).