What happens if your Company makes a trading loss?

Running a business involves both opportunity and risk. While the primary objective of any company is to generate profit there may be financial years in which expenses exceed income. Experiencing a trading loss or business loss is not uncommon, particularly during periods of investment, expansion or economic uncertainty.

For many business owners, reporting a business loss can feel worrying or even discouraging. However, a loss does not automatically mean failure. Many businesses go through loss-making periods, particularly during times of growth, investment, or wider economic pressure.

The key is understanding how a business loss works, meeting your compliance obligations, and knowing how to use tools like carry forward loss to your advantage.

What does ‘making a loss’ actually mean?

When a company makes a trading loss it's total allowable expenses exceed it's total income during a financial year. In simple terms the business has spent more than it has earned.

Typical expenses that can create a business loss include:

• Operational costs

• Salaries

• Rent and utilities

• Depreciation

• Professional fees

• Overheads

When these exceed revenue the result is a net loss.

Business losses may rise for a variety of reasons including:

• Investment in equipment, tech and infrastructure

• Expansion into new markets

• Increased staffing costs

• Product development or marketing campaigns

• Unexpected operational expenses

• Economic downturns or seasonal fluctuations

Importantly, not all business losses indicate poor management. In some cases, a loss reflects strategic investment designed to generate future growth. For example, a company may invest heavily in development or marketing this year to generate stronger profits in the years ahead.

Do you still need to file your tax return?

Yes! Even if your company has made a trading loss and has no taxable income, you are still legally required to submit your annual tax return.

Filing obligations apply regardless of profitability. Tax authorities like HMRC require businesses to report their financial position every year, whether that position reflects a profit or a loss.

Typical expenses that can create a business loss include:

- Record losses correctly

- Preserve your right to carry forward loss

- Avoid penalties and interest charges

Failure to submit returns may result in:

- Administrative penalties

- Interest charges

- Compliance risks

- Reputational damage

- Difficulties in securing financing

Maintaining compliance protects the legal and financial standing of your business.

Using digital filing systems can significantly simplify this process by:

• Reducing errors

• Improving accuracy

• Maintaining organised financial records

• Minimising the risks of penalties

Compliance remains essential, even in a loss-making year.

Do you pay tax if you made a loss?

Generally, no.

If your company has no taxable profit, you will not have to pay corporation tax for that financial year because there is no taxable profit. However, businesses are allowed to carry forward losses to offset against future profits. This means that if you return to profitability next year, you may be able to reduce your taxable profit using this year’s business loss. Carry forward loss allows a company to use its current trading loss to reduce taxable profits in future accounting periods.

For example, if your company makes a loss of £50,000 this year and a profit of £80,000 next year, you can carry forward the loss of £50,000 to reduce your profit. This means your profit will be reduced to £30,000.

This mechanism helps smooth the tax burden over time and supports business recovery after difficult periods. In this way today’s business loss can reduce tomorrow's tax bill.

It is important, however, to ensure that losses are properly recorded if you intend to carry forward your loss and reported in accordance with tax regulations to preserve the right to carry them forward.

What about cash flow:

When a business makes a trading loss it can have an impact of the following:

• Cash flow

• Investor confidence

• Loan applications

• Business sustainability

That’s why it’s important to:

• Review your expenses

• Identify unnecessary costs

• Adjust pricing or strategy

• Seek professional advice if needed

Business losses can be a warning sign, but they can also be a strategic investment phase.

Why digital filing makes it easier:

Using a digital tax filing tool helps you:

• You can track performance year-on-year

• Access financial statements instantly

• Avoid missing deadlines

• Stay compliant even during difficult years

Most importantly, digital filing removes stress. When everything is stored securely and submitted correctly, you gain a peace of mind, even in a loss-making year.

How to use losses:

If your company makes a loss during a financial year, this can be a valuable benefit for the future periods.

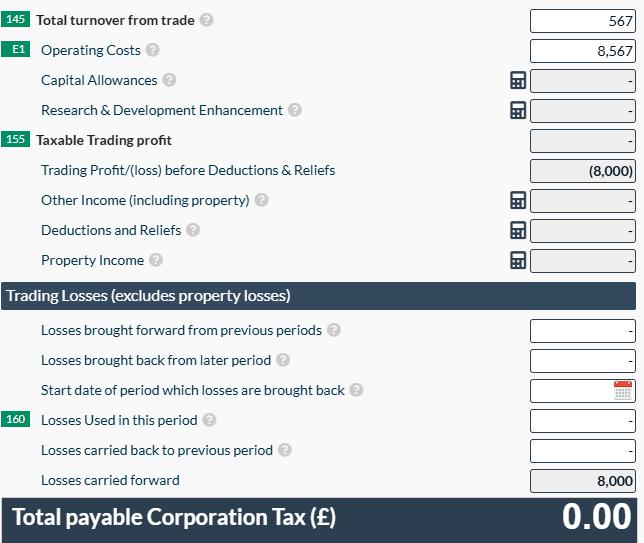

For example, if your total turnover is £567 and your expenses total £8567, your company has made a loss of £8000. Rather than losing this value, the £8000 can be carried forward and used to reduce future taxable profits.

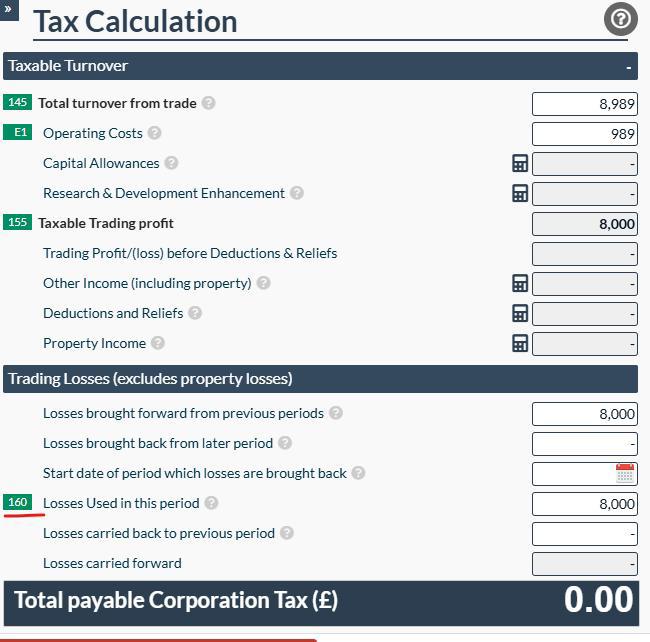

In a later financial year, if your company generates a profit of £8000, you can apply the £8000 loss brought forward to offset that profit.

This reduces your taxable profit to £0, meaning no corporation tax would be payable for that period.

How this is reflected in your CT600:

When completing your CT600, you will enter:

The amount of trading losses carried forward into the period and then the amount of that carried forward loss that is being used in the current period. This is typically entered in the relevant section of BOX 160 in the trading losses section of the CT600.

It is important to note that you only enter the amount of loss used in box 160 for that specific period, not the full amount available.

Key points to keep in mind:

- Business losses are used to reduced taxable profits, which in turn lowers your corporation tax

- An unused trading losses will continue to be carried forward to future years

- Your remaining loss balance is usually tracked within the tax software

Final thoughts

Making a business loss isn’t the end of your business career. What matters most is:

- Filing correctly

- Carrying forward your loss

- Staying compliant

- Understanding your numbers

- Planning for recovery

With the right systems in place and easy digital filing tools, you will stay in control, whether you make a profit or a loss. If your company has made a loss this year, don’t panic. File smart, review your strategy, and move forward confidently.